American Journal of Business and Society, Vol. 1, No. 4, November 2016 Publish Date: Aug. 19, 2016 Pages: 195-199

Financial Development, Financial Integration and Economic Growth

Arash Ketabforoush Badri1, *, Aidin Poorabdollahi Sheshgelani2

1Department of Economics, College of Management and Accounting, Qazvin Branch, Islamic Azad University, Qazvin, Iran

2Master of Executive Management, Department of Management, Tabriz Branch, Islamic Azad University, Tabriz, Iran

Abstract

The effects of financial development and economic growth is one of the importance chanals included the economic issues and have followed a lot of debates. Some economists believe that financial development by increasing savings and increased levels of investment can provide an appropriate basis for economic growth and some others are emphasized, to transfer the effect of financial development on economic growth through its effects on resource allocation and investment efficiency. For this purpose this study is trying to deal with the relationship between financial development, financial integration and economic growth in 24 OIC selected countries using panel data method in period 2005 to 2013. The results of the study show that financial development, human education and government spending have positive effect and financial integration has negative effect on growth in studied countries.

Keywords

Financial Development, Financial Integration, Economic Growth, Panel Data

Received:July 21, 2016

Accepted: August 3, 2016

Published online: August 19, 2016

@ 2016 The Authors. Published by American Institute of Science. This Open Access article is under the CC BY license. http://creativecommons.org/licenses/by/4.0/

Contents

1. Introduction

Financial globalization, a process that refers to the rise and expansion of the current global financial communications (Torki et al, 2010). In this regard, the formation of a monetary union and the choice of a monetary anchor to expand world trade and financial relations and also establish the convergence of member state economies, help to deepen the process of financial globalization (Tayebi et al, 2007). Regional integration goes along with the globalization of the world trade system. Among these, the Islamic countries, also, due to having good potential and potential capacities, in order to expand trade and economic cooperation have attempted to integration of diverse forms such as the Persian Gulf Cooperation Council, the Organization of the Islamic Conference, the Organization for Economic Cooperation and so on.

The Organisation of Islamic Cooperation (OIC) is an international organisation founded in 1969 consisting of 57 member states. The organisation states that it is the collective voice of the Muslim world and works to safeguard and protect the interests of the Muslim world in the spirit of promoting international peace and harmony.

Islamic countries are economically developing and underdeveloped, religiously Muslim and will become culturally close. These countries have little trade and domestic trade is still very low among members. Except from oil-exporting countries (Algeria, Iran, Brunei, Gabon, Indonesia, Iraq, Kuwait, Libya, Nigeria, Oman, Qatar, Saudi Arabia and United Arabic Emirates), other Muslim countries are the most important export raw materials and consumables such as food, linen, leather and wood. A high percentage of Muslim population, live below the poverty line, the proportion reaches 70/2 percent in some countries such as Sierra Leone.

Therefore, this study tries to examine the relationship between financial integration and economic growth in 24 OIC selected countries in the period 2005 to 2013 using panel data method.

2. Theoretical and Empirical Literature Review

Theoretical models have identified a number of channels through which international financial integration can help to promote economic growth in the developing world. However, it has proven difficult to empirically identify a strong and robust causal relationship between financial integration and growth. In theory, there are a number of direct and indirect channels through which embracing financial globalization can help enhance growth in developing countries (Prasad et al, 2003, 23). Financial integration can raise economic growth by direct channels like Augmentation of domestic savings, Lower cost of capital due to better risk allocation, Transfer of technology and Development of financial sector and indirect channels like Promotion of specialization, Inducement for better policies and Enhancement of capital inflows by signaling better policies. These items make higher economic growth. About the Augmentation of domestic savings we can say North-South capital flows in principle benefit both groups. They allow for increased investment in capital-poor countries while they provide a higher return on capital than is available in capital-rich countries. This effectively reduces the risk-free rate in the developing countries. Reduction in the cost of capital through better global allocation of risk causes effects on economic growth. International asset pricing models predict that stock market liberalization improves the allocation of risk (Henry (2000), and Stulz (1999)). First, increased risk sharing opportunities between foreign and domestic investors might help to diversify risks. This ability to diversify in turn encourages firms to take on more total investment, thereby enhancing growth. Third, as capital flows increase, the domestic stock market becomes more liquid, which could further reduce the equity risk premium, thereby lowering the cost of raising capital for investment.

Mahajan and Verma (2015) studied relationship between international financial integration and economic growth in India during 1981-2011. Apart from direct impact of international financial integration on growth, indirect impact (via financial development) has also been studied empirically. Models of co-integration and Vector Error Correction Model (VECM) have been applied to examine the relationships. The study observes that international financial integration affects the growth of the economy positively; and change in economic growth due to it through financial development is approximately 8.63 percent. The study also suggests that the structural reforms that took place in India in early nineties did not affect the existing relationship of global financial integration and economic growth significantly.

Miron and Alexe (2014) studied empirical analysis regarding the impact of current account imbalances, as counterparts to net capital flows, on the income convergence in the European Union during 1995 – 2007. Results show that the current account deficits had an income convergence effect in the area, more specifically they contributed to a higher economic growth in the countries with lower levels of initial GDP per capita.

Song et al (2013) have investigated empirical panel data analysis to detect the catching- up effect in growth and the possibility to form different convergence clubs in selected Europe and Asian economies during 1960-2009. The results reveal that all economies except Turkey and India are able to catch- up with U.K. economy. The economies in both regions of Europe and Asia are able to form their convergence clubs.

Dvorokova et al (2011) have studied impact of the financial crisis on the convergence of the Czech economy with the Euro area economy in the period 1990-2009. The results of the model suggest a rather low dependence of the average economic level of the euro area on the independent variables (PLI and OPENK).

Rasmidatta (2011) examined the relationship between domestic saving and economic growth and convergence hypothesis in Thailand by using time series annual data from 1960 to 2010 with Granger causality test. The test results shows that domestic saving growth rate does not help narrowing the range of different of income of Thailand and Singapore which mean that domestic saving growth rate does not support the convergence hypothesis in Thailand.

Faruk et al (2011) studied effects of convergence in governance on investment decisions among a sample of 43 developing countries, using dynamic system GMM estimations during 1992-2005. Various dimensions of the quality of the administration (control over corruption, quality of bureaucracy, law and order), of political stability (government stability, internal conflict, ethnic tensions), and of democratic accountability (civil liberties, political rights, democratic accountability) show a positive and significant impact on investment. This result is all the more important for the BSCE countries, because of the scope of improvement in governance that still exist in the region.

Haiss et al (2011) investigated the impact of financial crises on the finance-growth relationship in the European perspective. The results showed that the development of European financial markets seems to have not only decoupled from the real sector but also to exert an inverted impact on growth.

Bower and Turrini (2010) have investigates the accession-related economic boom in the countries which recently entered the European Union (EU). The analysis tests whether, on top of the standard growth determinants, the period of EU accession made a significant difference to the growth performance of the new member states (NMS). They find that the period of EU accession is characterised by significantly larger growth rates of per-capita GDP, even after controlling for a wide range of economic and institutional factors.

Fung (2009) tries to tests for convergence in financial development and economic growth by incorporating the interaction between the real and financial sectors into an otherwise traditional test for convergence. The results show strong evidence for conditional convergence. Middle- and high-income countries conditionally converge to parallel growth paths not only in per-capita GDP, but also in financial development.

Furceri (2009) analyzes the effects of fiscal convergence on business cycle volatility and growth. Using a panel 21 OECD countries (including 11 EMU countries) and 40 years of data. He finds that countries with similar government budget positions tend to have smoother business cycles and that is, fiscal convergence (in the form of persistently similar ratios of government surplus/deficit to GDP) is systematically associated with smoother business cycles.

Kakilli et al (2009) review the literature on the finance-growth nexus and investigate the causality between financial development and economic growth in sub-Saharan Africa for the period 1975-2005. Using panel co-integration and panel GMM estimation for causality, the results of the panel co-integration analysis provide evidence of no long-run relationship between financial development and economic growth. The empirical findings in the paper show a bi-directional causal relationship between the growth of real GDP per capita and the domestic credit provided by the banking sector for the panels of 24 sub-Saharan African countries. The findings imply that African countries can accelerate their economic growth by improving their financial systems and vice versa.

3. Econometric Methodology and Variables

3.1. Panel Data

Panel data is data from a (usually small) number of observations over time on a (usually large) number of cross-sectional units like individuals, households, firms, or governments. In other words panel data analysis is a method of studying a particular subject within multiple sites, periodically observed over a defined time frame. With repeated observations of enough cross-sections, panel analysis permits the researcher to study the dynamics of change with short time series. The combination of time series with crosssections can enhance the quality and quantity of data in ways that would be impossible using only one of these two dimensions (Gujarati, 2004). Some more advantages of panel data as given in ‘Basic Econometrics’ by Gujrati are:

Ÿ Since panel data relate to individuals, firms, states, countries, etc over time, there is bound to be heterogeneity in these units. The techniques of panel data estimation can take such heterogeneity explicitly into account by allowing for individual-specific variables.

Ÿ By studying the repeated cross section of observations, panel data are better suited to study the dynamics of change.

Ÿ Panel data can better detect and measure effects that simply cannot be observed in pure cross-section or pure time series data.

Ÿ By making data available for several thousand units, panel data can minimize the bias that might result if we aggregate individuals or firms into broad aggregates.

3.2. Data and Variables

The study population consisted of 24 selected OIC countries Iran, Malaysia, Turkey, Bahrain, Kuwait, Oman, Saudi Arabia, Bangladesh, Pakistan, Algeria, Cameroon, Egypt, Morocco, Tunisia, Benin, Burkina Faso, Chad, Mali, Mauritania, Mozambique, Niger, Senegal, Sierra Leone and Togo. Period is used 2005-2013. Time series data from these countries have been collected from WDI 2015. The model presented in this research paper inspired by Sarkar and Amor (2009) is as follows:

LnGDPPit = β0 + β1LnFDit + β2LnFIit + β3LnGit + β4Ln HEit + εit (1)

LnGDPPit = Logarithm of GDP per capita constant 2000 dollars

LnFDit = Logarithm of financial development (the share of domestic credit allocated to the private sector of GDP)

LnFIit = Logarithm of financial integration index (ratio of net foreign assets to GDP)

LnHEit = Logarithm of public spending for education of GDP

LnGit = Logarithm of size of government (share of government spending of GDP)

εit = random error

4. Empirical Analysis

4.1. Results of F-lymr and Houseman Test

Table 1 shows that the value of F test statistic using fixed effects would be more appropriate. Houseman also test statistic indicates the suitability of the method for estimating the fixed effects model.

Table 1. Results of F- Lymr and Houseman test of the estimated model.

Sources: research findings

4.2. The Estimation Results

Accordingly, the results of model estimation is introduced to determine the relationship between financial development and economic growth using a fixed effects panel data are presented in Table 2.

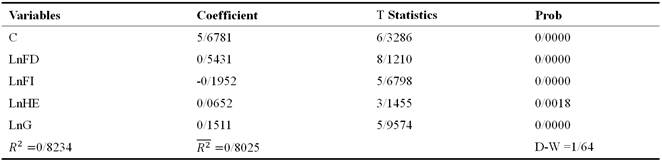

Table 2. Results of estimating the relationship between financial development and economic growth.

Sources: research findings

The table 2 showed that all coefficients have signs consistent with the theoretical basis and all coefficients are significant. According to the results, one percent increase in the share of domestic credit allocated to the private sector, GDP per capita increased 0/54. Financial integration coefficient is -0/19. This means that a one percent increase in financial integration, GDP per capita, 0/19 percent decreased. As mentioned earlier, the ability of a country to achieve convergence depends on four key factors: Behavior and structure of bank and non-bank financial services providers, the development of money and capital markets, country's degree of openness to international financial flows, finally, financial markets and has developed a good relationship with the international financial institutions. After considering the above factors can be argued that in the studied countries due to non-fulfillment of this condition, capital flows and foreign investment persistence, no positive effect on economic growth. In this group of countries with existing conditions, financial integration has a negative effect on economic growth. Human education coefficient is 0/06. This indicates that with improved human education, we can see an growth of countires is increased. So that the improvement of mental and physical condition will improve labor and thus increase the rate of labor productivity should be that this resulting in increased production and the increase in exports of the country and it can raised the growth of the countires. Government spending coefficient is 0/15. This shows that a one percent increase in government spending, growth in these countries will increase 0/15 percent. Also, as can be seen in the R2 estimated model is 0/82, which this shows that the explanatory power of the independent variable.

5. Conclusions

The importance of financial markets and the development of these markets to raise capital needed for economic growth, were considered the financial integration between Islamic countries, which could be conducive to the provision of capital needed for economic growth in these countries. The purpose of this study was obtain the effects of financial development, financial integration on economic growth of 24 selected OIC countries using panel data method for the period 2005 to 2013. Based on the results of the estimation was found financial development, human education and government spending have positive effect and financial integration has negative effect on growth in studied countries. Financial markets provide resources through small and big savings in the economy and optimize the flow of financial resources to use their guidance and needs investment in the productive sectors of the economy. So the factor that limits the gains from financial integration due to the economic structure of this group of countries which are generally lacks advanced and efficient financial markets. Government spending and human education coefficient is positive, this means that increase in public spending and investment in human capital to increase the economic growth of studied countries.

References

- Bower, U., Turrini, A.(2010), EU Accession: A Road to Fast-track Convergence? Comparative Economic Studies 52,June, 181-205.

- Dvorokova, K., Kovarova, J., Sulganova, M.(2011), Impact of the Financial Crisis on the Convergence of the Czech Economywith the Euro Area Economy, 136-149, www.opf.slu.cz/kfi/icfb/proc2011.

- Faruk Aysan, A., Faruk Baykal, O.(2011), The Effects of Convergence in Governance on CapitalAccumulationin the Black Sea Economic Cooperation Countries, Etudes et Documents, 1-37.

- Fung, M.K.(2009), Financial development and economic growth:Convergence or divergence, Journal of International Money and Finance 28, 56–67.

- Furceri, D.(2009), Fiscal Convergence, Business Cycle Volatility and Growth, OECD Economics Department Working Papers, No. 674, OECD Publishing, 1-28.

- Greene, W. H. (2003), Econometric Analysis, Prentice Hall.

- Gujarati, D. (2003), Basic Econometrics, the McGraw-Hill.

- Haiss, P., Juvan, H., Mahlberg, B.(2011), The Impact of Financial Crises on The Finance-Growth Relationship: a European Perspective, Journal of Banking and Finance, July,1-20.

- Henry, P.B.(2000), Stock Market Liberalization, Economic Reform, and Emerging MarketEquity Prices, Journal of Finance, Vol. 55, April, 529–564.

- Kakilli Acaravci, S., Ozturk, I., Acaravci, A.(2009), Financial development and economic growth:literature survey and empirical evidence Fromsub-saharan aFrican countries, SAJEMS NS 12 (2009) No 1, 11-27.

- Mahajan, N., Verma, S.(2015), International Financial Integration and Economic Growth in India: An Empirical Investigation, Eurasian Journal of Business and Economics 2015, 8(16), 121-137.

- Miron, D., Alexe, I.(2014), Capital flows and income convergence in the European Union. Afresh perspective in view of the macroeconomic imbalanceprocedure, Procedia Economics and Finance, 8, 25-34.

- Rasmidatta, P.(2011), The Relationship Between Domestic Saving and Economic Growth and Convergence Hypothesis: Case Study of Thailand, Sodertorns Hogskola, Department of Economics, Master Thesis, Economics, Spring, 2011.

- Song, P.C., Sek, S.K., Har, W.M.(2013), Detecting the Convergence Clubs and Catch-up in Growth, Asian Economic and Financial Review, 2013, 3(1), 1-15

- Stulz, R. (1999), International Portfolio Flows and Security Markets, InternationalCapital Flows, NBER Conference Report Series, University of Chicago Press, 257–293.

- Tayebi, K., Sameti, M., Abbaslu, Y., Esgragi Samani, F.(2009), Effects of and Financial Development on Economic Growth of Iran, Value Quarterly Journal of Economics, Vol. 6, No. 3, Fall, 55-78.

- Torki, L., Tayebi, K., Sharifi, S.(2010), The impact of financial reform on economic growth and the creation of convergence between Selected Islamic countries, Journal of Economic Modeling No. 2, Winter, 65-86.