American Journal of Business and Society, Vol. 1, No. 3, September 2016 Publish Date: Aug. 5, 2016 Pages: 166-175

Impact of Demographics Variables on the Level of Financial Literacy Among the University Students of Punjab Pakistan

Sidra Akram, Amna Abbas, Umar Draz*

Hailey College of Commerce, University of the Punjab, Lahore, Pakistan

Abstract

Financial literacy is an important feature that permits people to attain a successful financial state. Past studies were only limited to Gender. Therefore, the purpose of this paper is to measure the level of financial literacy among university students by considering the various demographics of students. In this sense, a survey was conducted with 137 students who live in Pakistan for an analysis of the collected data. t-independent sample test and k- independent test was used for binary categorical demographics while One-way ANOVA was used to check the difference in financial literacy level on the basis of multiple categorical variables All these measures showed a highly significant difference in area of study except financial behavior.

Keywords

Financial Literacy, University Students, K Independent Sample Test, T-independent Sample Test, One –Way ANOVA

Received:June 18, 2016

Accepted: July 20, 2016

Published online: August 5, 2016

@ 2016 The Authors. Published by American Institute of Science. This Open Access article is under the CC BY license. http://creativecommons.org/licenses/by/4.0/

Contents

1. Introduction 2. Financial Literacy (Literature Review) 3. Relationship Between Gender and Financial Literacy 4. Credit Card Use 5. AGE 6. Research Design 6.1. Need of the Study 6.2. Objectives of the Study 6.3. Data Base and Research Methodology 6.4. Hypothesis 7. Sample Characteristics 8. Analysis and Discussion 9. Results and Discussion of Descriptive Statistics 10. Results and Discussion of T-test and K Independent Sample Test 11. Results and Discussion of One-Way ANOVA 12. Conclusion and Findings of Study Limitations

1. Introduction

Financial literacy is outlined as ones’ "knowledge of facts, concepts, principles, and technological tools that helps in being good in managing money." (Garman & J. Gappinger, Delivering Financial Literacy Instruction to Adults, 2008) or it may be defined as Financial literacy has been referred to as an important ability for the people who need to operate in an advanced financial state of affairs. Governments on all sides of the world are interested in finding economical approaches to increase the population’s level of financial literacy through the formation or development of national strategies for financial literacy with the goal of providing learning opportunities at different levels of education (A. & Messy., 2012).

The importance of financial literacy has been arising with the liberation of money markets and also the easier access to credit as financial institutions compete with one another for market share, the ascent in development and selling of economic merchandise, and also the government’s encouragement for folks to require a lot of responsibility for his or her retirement incomes (Potrich, Vieira, & Coronel, 2015) (Beal & Delpachitra, 2003; Ibrahim & Marcelin, 2006). Additionally, financial literacy can forestall the university students to engage in depth debt particularly in master card debt.

In current years, developed and rising countries have become preoccupied with the level of financial literacy of their people, mainly attributable to the tough economic and financial contexts and also the proven fact that the lack of financial literacy is one of the factors that have contributed to poor informed financial choices with immense negative repercussions in financial situation (Potrich, Vieira, & Coronel, 2015) (Girardi et al., 2010). As a result, financial literacy involves be notable around the world as a vital component to economic stability and development, and it reflects the approval of the High Principals Level concerning National strategies for financial literacy from the Organization for Economic Co-operation and Development(OECD) supported for the G20 meeting (Potrich, Vieira, & Coronel, 2015) (G20, 2012).

In addition to governments, international organizations and researchers United Nations agency dedicate themselves to the present theme, OECD (2012) is associate example of a company that conceptualizes financial literacy as a method during which people improve their understanding of financial product and their ideas and risks in such how that through data and clear recommendations, skills and necessary confidence is developed to create basic and safe financial decision to enhance their well-being.

From this view, (Potrich, Vieira, & Coronel, 2015) Anderson and Van done (2010) outline financial literacy as a strengthen measure that enables individuals to have enough conditions within which to grab financial issues and manage their personal finances in a satisfactory means, avoiding financial obligation.

Another facet associated with financial education is financial literacy. in step with, (C. A, P., & A., 2012) financial literacy involves the ability to know financial info and build economical decision using identicalinformation, whereas financial education merely involves remembering a group of facts. In this context, financial education can be thought-about a capability to develop a method of making correct choices and thriving management of personal financial and financial literacy is that the ability to use the information and skills needed. Simply, the main focal point of financial literacy involves not solely information however also individuals’ financial behaviors and attitudes.

However, there remains an absence of a unity within the academic field regarding the instruments for measure financial literacy. In recent years several studies are conducted within the USA, like those by subgenus (Chen & Volpe, An analysis of personal financial literacy among college students, 1998), and (A, A & P, E, 2010). Studies with families from the UK have additionally been conducted by (Potrich, Vieira, & Coronel, 2015) Lusardi and Tufano (2009) and Gather well (2011). In addition, the same studies were held with university students from Japan by (Sekita, 2011) and from African nation by (A, 2011) and with retired persons in Holland by (Potrich, Vieira, & Coronel, 2015) Among rising countries, it remains common to find works that debate the themes approached in this paper. Within the Brazilian situation, this subject has been the center of studies conducted by (Mendes-Da-Silva, Nakamura, & de Moraes, 2012) and (Norvilitis, J. M & Mendes-Da-Silva, W, 2013) in student sample. A distinction in our paper is that the study of the university students population.

Whatever measure is used, several studies have proved the relations and influences of socioeconomic and demographic variables on the degree of individuals’ financial literacy (Chen & Volpe, An analysis of personal financial literacy among college students, 1998) (Potrich, Vieira, & Coronel, 2015) Lusardi and Tufano,2009; Hastings and Mitchell, 2011; (LUSARDI &MITCHELL, Financial literacy and retirement planning in the United States, 2011);(Atkinson, A. & F. Messy, 2012);(Martin Brown & Roman Graf, 2013); (Mottola G., 2013). Gender is one in every of the most variables researched, and therefore the majority of the proof indicates that women usually show lower level of financial literacy than men (Chen & Volpe, An analysis of personal financial literacy among college students, 1998) (LUSARDI & MITCHELL, Financial literacy and retirement planning in the United States, 2011) (Atkinson, A. & F. Messy, 2012) (Lusardi, Financial Literacy and Quantitative Reasoning in, 2013); (Brown, Financial Literacy and Retirement Planning in, 2013); (Mottola G., 2013) (Sekita, 2011) broadens the proof that girls face greater difficulties than men in creating financial calculations, which, additionally to not having the essential financial concepts and lower level of knowledge, create accountable financial decision harder to attain. this will be considered a worrying issue as a result of girls are gaining space within the marketplace and taking part a lot of in consumer decisions, financial management and indebtedness; furthermore, girls typically have the role of being responsible for the family. within the period between 2000 and 2010, Brazilian girls that were accountable for the family grew from twenty two 22% to 37.3% in keeping with the Brazilian Institute of earth science and Statistics (IBGE, 2010). The existing literature has argued that financial literacy is a three-dimensional construct which a singular construct would not be comfortable to cover all dimensions involved. Though some studies have been conducted, there is still ambiguity concerning the constructs and best proxies to evaluate financial literacy and additionally whether or not a model maybe used for various genders. All of those facts recommend the necessity of building and validate models that are able to consider measures and their sub-relations at the same time.

In order to increase the financial literacy, Bank Negara Asian country has initiated the subsequent three-pronged approaches that embrace developing and diffusive instructional materials on monetary merchandise and services through booklets and websites, promoting monetary education to students united with the Ministry of Education and monetary establishments and conducting financial educational outreach program to various target groups, as well as university students, through strategic partnerships with different organizations. (Swee Lian, 2008) Since they have expanded buying power, this had created the university or faculty students one among the necessary client market segments.

Many students are not able to manage their income. Once they have a lot of money they simply spend it on necessary and unnecessary things. This spending behavior clearly shows the lacking of financial literacy among students that need to be modified. We must improve the financial knowledge and abilities of our students. There should be training programs from high schools and comprehensively in colleges and universities (Potrich, Vieira, & Coronel, 2015) (Davidson, 2006, p. 22).

Pakistan is a developing country; financial literacy is all the more important in Pakistan students have to take loans for their higher education level so they must have accurate knowledge about finance that’s why we are exploring financial literacy level among university students.

2. Financial Literacy (Literature Review)

The term financial literacy has been oftentimes used as equivalent word for financial education or financial knowledge, but actually, these constructs are conceptually totally different, and using them as synonyms will cause issues because financial literacy is deeper than financial education. (J. HUSTON, 2010) Says that financial literacy has 2 dimensions:

Understanding, that represents the personal financial knowledge of financial education, and use, which means the appliance of the management of personal financial knowledge. (Hung, Parker, & Yoong, 2009) Outline financial education as a method by which individuals improve their comprehension regarding financial merchandise and services, and financial literacy is outlined as the ability to use the knowledge and abilities attain to handle resources efficiently, providing financial well being.

One of the dilemmas in financial literacy study is that the understanding of the variations between this construct, financial knowledge and monetary (financial) education. In this sense (Robb, Babiarz, P, & Woodyard, A, 2012), build a distinction among these terms, indicating that financial knowledge involves the power to grasp financial knowledge and build economical decision using this information, whereas monetary (financial) education is only the power to recall a gaggle of facts or just financial knowledge. (Xiao, 2011) Argue that financial knowledge isn't adequate for proficient financial management, and the influence of financial knowledge on behavior is a measure of the student’s monetary (financial) attitudes. According to (Criddle, E, 2006) having financial literacy includes learning when selecting form several alternatives to determine monetary objectives. All in all, financial literacy goes more than the concept of basic financial education (J. HUSTON, 2010) (Robb, Babiarz, P, & Woodyard, A, 2012)

Another difficulty within the study of financial literacy is that the lack of models that show the various dimensions concerned. In a comprehensive review of the literature, (J. HUSTON, 2010)has found that out of the seventy-one works revised, over fifty couldn’t outline financial literacy, and within the twenty works that gave a definition, eight totally different definitions may well be found; two definitions centered on ability, and three definitions centered on knowledge solely.

Although there are several definitions and dimensions used to describe financial literacy, most of them seek advice frogman individual’s ability to get, understand and assess financial into that’s necessary to form an economical decision aiming at the individual’s financial wellbeing. In this means, a wide definition is given by the OECD, measuring financial literacy as a mixture of the awareness, knowledge, skill, perspective(attitude) and behavior necessary to make solid financial choices, and eventually, reach financial wellbeing (Atkinson & Messy, 2012) The OECD describes financial literacy in terms of three dimensions: financial knowledge, monetary (financial) behavior and financial attitude. Financial knowledge has been projected by as a specific type of human capital attain within the life cycle through learning aspects that have an effect on the power to manage income, expenditures and savings in an efficient approach. it's been developed through interactions once transmission and receiving info in teams (Danes, S. M. & Haberman, H.R, 2007)financial attitude is interpret by (Potrich, Vieira, & Coronel, 2015) as a combination of ideas, info and emotions regarding the process of learning and ends up in a tendency to act favorably. Hence, the development of attitudes is a result of the direct experiences of people due to the exposure or acquisition of the content (Winkielman, Halberstadt, Fazendeiro, & Catty, 2006). Additionally, financial behavior is describe as a vital element of financial literacy (Potrich, Vieira, & Coronel, 2015) (OECD, 2013), whereas recent studies have associated financial behavior as a part of financial literacy (Lusardi and Mitchell, 2013) (Potrich, Vieira, & Coronel, 2015)

Therefore, it looks that there's not a ‘‘common’’ or ‘‘usual’’ manner within which investigators and professionals measure financial literacy. However, this doesn't mean that financial literacy has not been measured during a consistent manner within the literature and much. Annemarie Lusardi and Olivia Mitchell developed a gaggle of three questions that are ordinarily used in several studies (KNOLL & HOUTS, 2012) the queries comprehend three basic concepts of finance: the tax rate, inflation and risk aversion.

The utility of those queries lies within the indisputable fact that they have been the themes of the many studies, building a helpful base to compare among countries with relation to monetary (financial) literacy. Among these studies, it's necessary to see those by (Potrich, Vieira, & Coronel, 2015) Hastings and Mitchell (2011) in Mexico; Lusardi and Mitchell (2011) within the USA, (Sekita, 2011) in Japan; and recently, those in Sweden (Brown & Graf, Financial Literacy and Retirement Planning in, 2013), (Arronde, Debbich, & Savignac, 2013) France and Romania (Beckmann, 2013)

The lack of measures and international information still as the request from several countries asking for a strong measure of financial literacy on a national level have led the OECD and its International Network for financial Education (INFE) to develop search instrument that maybe accustomed appraise the financial literacy of individuals in several countries, centralized in aspects like the knowledge, attitudes and behavior related to international ideas of financial literacy. Apart from these instruments, some authors have evaluated the dimensions of financial literacy separately. (Rooij, Lusardi, & J. M. Alessie, 2011) Examined the relationship between financial knowledge and retirement designing in Holland Studies by (Chen & P. Volpe, 1998) (Alena C, 2001), and developed appraising instruments for financial behavior. Another instrument employed in some analysis is that the FLABK (financial literacy—attitude, behavior and knowledge) elaborated by Susan Sminth Shockey (2002), World Health Organization analyzes the attitudes and behavior of respondents.

Despite the variations within the ideas, analysis and dimensions inherent to financial literacy, there's associate agreement that its importance brings advantages to people well as families in several aspects (Blalock, Tiller, & Monroe, 2004, Vol 53, No 2) and (Grable, & Joo, S.H, 2006). an increase in financial literacy promotes an improvement in self confidence, management and independence(Allen, Edwards, Hayhoe, & Leach, 2007) and an improvement in the marriage relationship (OGGINS, 2003) in step with (Schmeiser & Seligman, 2013) and (LUSARDI & MITCHELL, 2011), an increase in the financial literacy level contributes to changes in national prosperity over time, and for (FONSECA, MULLEN, ZAMARRO, & ZISSIMOPOULOS, 2012), financial decision are sensitive to developing men’s and women’s levels of education and positively impact this development.

This question is even additional necessary in developing countries like Brazil, wherever the academic level is often less smaller, have an oversized population with budget restrictions, the economy is unstable with periods of nice fluctuation in interest rates, availability of credits and changes of risk and return on financial products. It needs from the population increased application of monetary (financial) literacy that becomes even additional essential.

3. Relationship Between Gender and Financial Literacy

The relationship between gender and monetary(financial) management has been gaining space as a result of knowing individuals’ profiles and levels of financial literacy is extraordinarily related because of the rise in their financial tasks.

Therefore, low levels of financial literacy will cut back the ability to manage and accumulate assets and in terms of ultimate analysis, guarantee a hopeful financial future (Mottola, 2013). Specifically, in terms of variations between genders, several authors found that ladies typically show lower levels of financial literacy than men (Chen & Volpe, An analysis of personal financial literacy among college students, 1998) (LUSARDI & MITCHELL, Financial literacy and retirement planning in the United States*, 2011) (Atkinson & Messy, 2012) (Lusardi & Wallace, Financial Literacy and Quantitative Reasoning in the High School and College Classroom, 2013) (Brown & Graf, 2013) (Mottola G. R., 2013). In the USA, (LUSARDI & MITCHELL, Financial literacy and retirement planning in the United States, 2011) found that ladies are less susceptible to answer properly and are a lot of susceptible to say that they not understand the answers to questions associated with financial literacy. Similar results have been found in different countries like Australia, France and Romania (Lusardi & Wallace, Financial Literacy and Quantitative Reasoning in the High School and College Classroom, 2013).

However, in a very study conducted in Sweden (2013), this distinction within the level of financial literacyis not influenced by a scarcity of women’s interest in financial queries, however actually, the distinction in genderis slightly lower once comparison the participation of individuals who answered all of the queries throughout the interviews to people who have an interest in finance. Furthermore, (Shambare & Rugimbana, 2012) examined the money acquisition in South Africa and found that 20% of men answered the compound interest queries properly compared to 10% percent for ladies, besides the association between gender and financial illiteracy.

4. Credit Card Use

Students like to use credit cards and those students who have credit cards have more favorable behavioral attitudes toward credit card usage than students who did not have credit cards (Xiao et al., 1995 as cited in Borden et al., 2007, p.25). Finally, more frequent use of credit cards was helped by further favorable and affective attitude toward credit card use.

5. AGE

Based on the previous researches, there's a positive relationship between the age and also the university students’ financial literacy. From eighteen to twenty four years young adults typically are having a better degree of demographic diversity and instability, with several living removed from home for the1st time. Moreover, several of those individuals gain a new independence, selflessness and a larger sense of financial responsibility. The acquisition of knowledge appears to extend with age and knowledge. The results usually show that the younger the age can tend to possess the lower financial literacy. (Volpe & Chen, 1998), (Micomonaco, 2003) and (Ronald, Haiyang, & Joseph, 1996) observed lack of financial literacy between those who aged 18-24 and this can be not a solely a results of depleted financial-based education at the college level. the explanation for the low level of information are often attributed to the young ages of eighteen to twenty two years recent of the participants or below thirty as majority of them square measure during a very early stage of their money life cycle. (Chen & Volpe, 1998).

6. Research Design

6.1. Need of the Study

As previously explained financial literacy involves providing awareness about the risk and return linked with financial products to the users and providers of financial products.

It is the information about the financial market that enables the players to manage the risk and regulate the high amount of returns.

University students with a commerce and business management surroundings are mainly expected to go into professions correlated with banking, finance and economics.

Examining the intensity of financial literacy of the students and measuring the impact of different demographic variables on their level of financial literacy will help the strategy makers to make a policy setting favorable to achievement of financial literacy. This in turn would make sure that the physical and financial resources are put to their best use in order to produce high levels of financial growth.

6.2. Objectives of the Study

Following are the objectives of our study;

Ÿ To examine the level of financial literacy among university students with the help of different measures (general awareness, financial attitude, financial behavior, and financial knowledge).

Ÿ To examine the impact of demographics on the level of financial literacy of students.

6.3. Data Base and Research Methodology

This study investigates the students population in Pakistan with a random sample of 150 students with a valid response of 137. The instrument has been formed by five blocks related to their questions to collect data. In beginning, we attempted to recognize the respondents’ profiles with eight questions correlated with demographic variables: gender, age, economic class, area of residence, job status, parent’s monthly income, contribution in home financial matters and area of study.

To estimate the level of financial knowledge, multiple choice questions have been chosen from (Rooij, Lusardi, & Alessie, 2011). For each question from the basic knowledge block, 1 to 5point has been assigned to each correct answer.

The scales option has taken into concern the best modification for the Pakistani’s context, which is translated and the content validation of which is analyzed. These scales have been chosen for this study because they represent to Pakistan reality best.

The accurate responses of the students to the financial literacy questions were used for the purpose of analysis. We applied descriptive statistics to measure general awareness by displaying charts and providing results in percentages and frequencies. To measure financial attitude on the base of binary categorical demographics we used 2 independent sample t-tests and on the basis of multiple categorical demographics we used k-independent sample test. Independent sample t test has been used to measure financial behavior on the basis of binary categorical demographics. A One Way analysis of variance (ANOVA) has been used to find out the differences in the financial behavior on the basis of age, Parents monthly income and area of study. Financial knowledge has been measured by using 2 independent sample tests on the basis of gender, job status and contribution in home financial matters, on the other hand, k independent test was used to evaluate financial knowledge on the basis of age, parent’s monthly income and area of study.

The students of commerce and management background formed the universe of the study as these students were more likely to be familiar with the financial and economic concepts as compared to students from other disciplines.

6.4. Hypothesis

The null hypothesis for this study is as follows;

H01: There is no difference in financial general awareness of male and female.

H02: There is no difference in financial general awareness of student’s regarding their job status.

H03: There is no difference in financial general awareness of students regarding their contribution in home financial matters.

H04: There is no difference in financial general awareness of students at different Level of age.

H05: There is no difference in financial general awareness of students regarding their parent’s monthly income.

H06: There is no difference of financial general awareness of students of different area of study.

H07: There is no difference in financial attitude of male and female.

H08: There is no difference in financial attitude of students regarding their job Status.

H09: There is no difference in financial attitude of students regarding their Contribution in home financial matters.

H010: There is no difference in financial attitude of students at different level of age.

H011: There is no difference in financial attitude of students regarding their parent’s monthly income.

H012: There is no difference of financial attitude of students of different area of study.

H013: There is no difference in financial behavior of male and female.

H014: There is no difference in financial behavior of students regarding their job Status.

H015: There is no difference in financial behavior of students regarding their contribution in home financial matters.

H016: There is no difference in financial behavior of students at different level of age.

H017: There is no difference in financial behavior of students regarding their parent’s monthly income.

H018: There is no difference of financial behavior of students of different area of study.

H019: There is no difference in financial knowledge of male and female.

H020: There is no difference in financial knowledge of students regarding their Job Status.

H021: There is no difference in financial knowledge of students regarding their contribution in home financial matters.

H022: There is no difference in financial knowledge of students at different level of age.

H023: There is no difference in financial knowledge of students regarding their parent’s monthly income.

H024: There is no difference of financial knowledge of students of different area of study.

7. Sample Characteristics

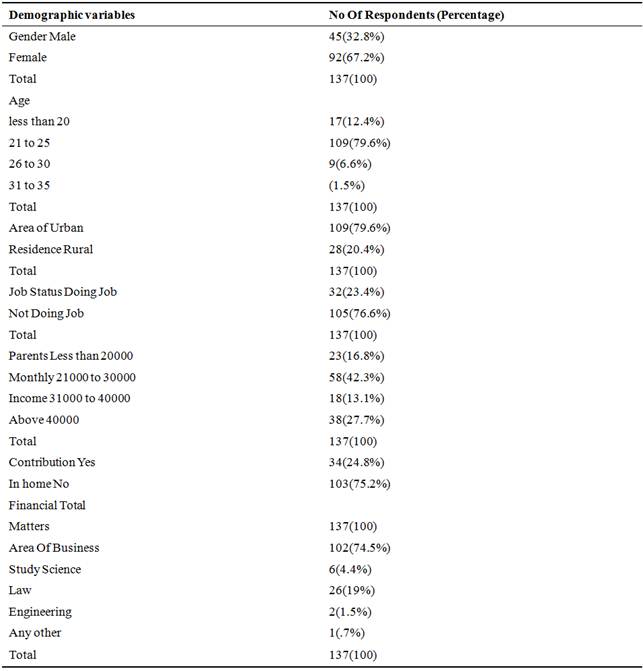

As far as the demographics profile of the students is concerned, sample consisted of a diversity of students related to different area of study and financial background. Demographic surroundings of the students represented in table 1.

Table 1. Demographic profile of the students.

Source: Author’s own, based on collected data.

Table 1 shows that out of 137 respondents most of the respondents that is, 92 respondents (67.2%) were female and 45 respondents (32.8%) were male. The age of the most of the respondents was in the range of 21 to 25, that is 109 respondents (79.6%), while 17 respondents (12.4%), 9 respondents (6.6%) and 2 respondents (1.5%) were in the range of less than 20, 26 to 30 and 31 to 35 respectively. Most of the respondents that is 127 (92.7%) belonged to middle class while 7 respondents (5.1%) and 3 respondents (2.2%) belonged to lower and top class respectively, as far as the area of residence of respondents is concerned 79.6% of the respondents reported that they live in urban cities while 20.4% respondents specified that they live in rural cities. With regard to their job status, out of 137 respondents 105(76.6%) are not the job holders while only 32 (23.4%) having a job. Most of the respondent’s families (42.3%) having a monthly income that is 21000 to 30000. 102 respondents are such, who don’t have any contribution in home financial matters. The area of study of most of respondents was from business that is 102 respondents (74.5%).

8. Analysis and Discussion

The questionnaire was divided into four parts that is the first part was related to general financial awareness second part was related to financial attitude; third part was related to financial behavior while the last part was related to financial knowledge. In order to examine the level of financial literacy among university students having different demographic profile firstly, we analyze the general financial awareness through cross tabulation calculated on SPSS to show descriptive statistics results.

The first general financial awareness question was related to some basic financial products such as pension funds, investment account, mortgage, credit card, saving account, unsecured bank loan, stock, shares and microfinance loan and bonds.

9. Results and Discussion of Descriptive Statistics

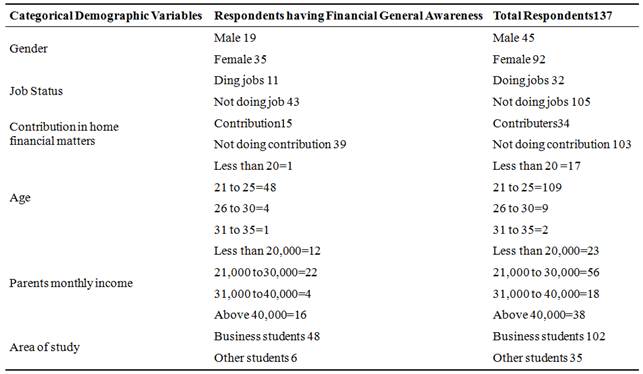

General awareness about finance is first measure of Financial Literacy in this study upon which we have applied Descriptive statistics. Through cross tab we derived following results. In our data variances among groups are un-equal. And according to unequal variances we found that 35 females and 19 males have general awareness. so we reject H01.11 job holders and 43 not having any job have Financial General Awareness so we reject H02.11Students who contribute in Home financial matters have financial awareness. 39 students who do not contribute in home financial matters have general awareness about finance so we reject H03. Students of 21 to 25 age group have more financial awareness than others so we reject H04. Students their parents have average salaries like 21,000 to 30,000 have more general awareness. So we reject H05. Business students have more Financial general awareness as compare to others so we reject H06.

Table 2. Descriptive Statistics.

10. Results and Discussion of T-test and K Independent Sample Test

In order to examine whether the significant differences exist in the financial attitude of the students on the basis of (binary categorical variables) such as gender, job status and regarding their contribution in home financial matters 2 independent sample test was used. As shown in table 2 the value of level of significance for 2 independent sample tests based on gender is .170. These values are greater than 0.05 so we accept the null hypothesis that’s mean there is no significant different lies in the financial attitude of the university students based on gender. The value of level of significance for 2 independent sample test based on their job status is .016 less than 0.05 so we reject our null hypothesis that’s mean there is a difference in the financial attitude of university students with respect to their job status. In order to determine the financial attitude based on the students contribution in home financial matters 2 independent sample test showed the value of level of significance .000 which is less than 0.05 so we reject our null hypothesis.

Table 3. Results of 2 independent sample tests to determine financial attitude.

K-Independent sample test was used to evaluate the financial attitude of multiple categorical variables like age, parent’s monthly income and area of study of students. K test showed the significance value of .255 > 0.05 based on age of respondents so we accept null hypothesis that’s mean there is no difference in financial attitude of students having different age. The significance 2 tailed value based on parents monthly income is .291 > 0.05 so we accept our null hypothesis. Based on area of study of students financial attitude shows significant value of .000 < 0.05 so we reject our null hypothesis that’s mean significant difference lies in financial attitude of students based on area of study.

Independent sample t test has been used to measure financial behavior on the basis of binary categorical demographics. Before applying t-test, Levene’s test for equality of variances was used in order to determine whether the differences between the groups are equal or not. As shown in table 3 the value of level of significance for Levene’s test is .197 in respect of gender. Since these values are greater than 0.05 so variances between the groups are equal. The value of level of significance for t test is .996 greater than 0.05 so we accept or fail to reject the null hypothesis. Value of level of significance for Levene’s test is .495 in respect of respondents job status as these values are greater than 0.05 so the variances are equal. The value of level of significance for t-test is .854 greater than 0.05 so we accept our null hypothesis that’s mean there is no significant differences in financial behavior of students regarding their job status. Levene’s test of equality of variances value is .443 greater than 0.05 shows equal variances in respect of respondents contribution in home financial matters as the level of significance value is .138 >0.05 so we accept or fail to reject our null hypothesis.

Table 4. Results of Independent Sample t-test to examine financial behavior.

To evaluate the financial knowledge on the basis of gender 2 independent sample test was used. The value of level of significance.003 < 0.05 so reject the null hypothesis. Significance value based on job status calculated by 2 independent samples is.004 < 0.05 so reject our null hypothesis that’s mean there is significant difference in financial knowledge of students with respect to their job status. Value of significance is.001 < 0.05 based on students contribution in home financial matters so we reject our null hypothesis, that is there is a significant difference in financial knowledge regarding their contribution in home financial matters.

K-Independent sample test was used to evaluate the financial knowledge of multiple categorical variables like age, parent’s monthly income and area of study of students. K test showed the significance value of .088 > 0.05 based on age of respondents so we accept null hypothesis that’s mean there is no difference in financial knowledge of students having different age. The significance 2 tailed value based on parents monthly income is .253 > 0.05 so we reject our null hypothesis. Based on area of study of students financial knowledge shows significant value of.003 < 0.05 so we reject our null hypothesis that’s mean significant difference lies in financial knowledge of students based on area of study.

11. Results and Discussion of One-Way ANOVA

In order to determine whether the significant differences exist in financial behavior based on multiple categorical variables such as age, parents monthly income and area of study of respondents one-way ANOVA was applied. The value of level of significance of one-way ANOVA is.385,.894 and.480 in respect of age, parent’s monthly income and area of study. Since all these values are greater than 0.05 so we accept our null hypothesis and there lies no significant difference in financial behavior with respect to age, parents income and area of study of respondents.

12. Conclusion and Findings of Study

Financial literacy is defined as the skill to use knowledge and capability to manage financial resources efficiently for a life span of financial comfort. Financial literacy involves imparting knowledge concerning the risk and return of financial products to the users and providers of these products. The present study tried to examine the level of financial literacy of university students and to find out the effect of different demographic variables on their financial literacy levels.

We measured financial literacy through general financial awareness, financial attitude, financial behavior and financial knowledge. The study concluded that basic difference in financial literacy lies in area of study of students. Students of business and commerce show high level of financial general awareness, attitude, behavior and knowledge as compared to other students.

On the basis of unequal variance among groups, there is a difference in general financial awareness regarding gender, job status, contribution in home financial matters, parent’s monthly income but highly significant difference lies in area of study and age factor. Students of business and commerce within the age of 21 to 25 have higher general awareness.

The level of financial attitude is different on the basis of job status, contribution in home financial matters and area of study. Study concluded that there is no difference in financial behavior of students regarding any demographics variables.

On the basis of financial knowledge there is a difference in financial literacy level with respect to gender, job status, contribution in home financial matters and area of study. Now it’s obvious that basic difference in financial literacy lies in the area of study. In fact, it is the curriculum that is offered to them that would be helpful in addressing the issue of financial literacy among students. So the basic financial concepts in courses in other various disciplines will enable the students to deal with financial products in order to make effective financial decision.

Limitations

Ÿ The data for the study was collected from PUNJAB UNIVERSITY; however a more extended geographical sample may produce different results.

Ÿ Our study showed the results on the basis of unequal variances between male and female so the results can be more valid with equal variances of male and female in sample.

References

- Arronde, L., Debbich, M., & Savignac, F. (2013). Financial Literacy and Financial Planning in France. Advancing Education in Quantitative Literacy, 1936-4660.

- J. HUSTON, S. (2010). Measuring Financial Literacy. Journal of Consumer Affairs, 296–316.

- Winkielman, P., Halberstadt, J., Fazendeiro, T., & Catty, S. (2006). Prototypes Are Attractive Because They Are Easy on the Mind. A journal of the Association of pshycological research, 799-806.

- SERVON, L., & KAESTNER. (2008). Consumer Financial Literacy and the Impact of Online Banking on the Financial Behavior of Lower-Income Bank Customers. The journal of consumer affairs, 271–30.

- A, A. (2011). Level of knowledge in personal finance by university freshmen business students. African J. Bus. Manag, 8933-8940.

- A,A, N., & P,E, N. (2010). The missing curriculum link: Personal financial planning. Amer. J. Business Edu, 79-82.

- Beckmann, E. (2013). Financial Literacy and Household Savings in. Advancing Education in Quantitative Literacy, 1963-4660.

- C.A, R., P., B., & A., W. (2012). The demand for proffesionals advice:The role of financial knowledge, satisfaction and confidence. Financial Services Review, 291-305.

- Criddle, E. (2006). Financial literacy: Goals and values, not just numbers. Alliance, 4.

- Danes, S.M., & Haberman, H.R. (2007). Teen financial knowledge, self-efficacy, and behavior: A gendered view. Journal of Financial Counseling and Planning, 48-60.

- Hung, A., Parker, A., & Yoong, J. (2009). Defining and Measuring Financial Literacy. Social science resrarch network, 28.

- KNOLL, M., & HOUTS, C. (2012). The Financial Knowledge Scale: An Application of Item Response Theory to the Assessment of Financial Literacy. Journal of Consumer Affairs, 381–410.

- Mandell, L. (2008). Financial literacy of high school students. Handbook of consumer financeresearch, 14620-4000.

- Robb, C., Babiarz, P, & Woodyard, A. (2012). The demand for financial professionals' advice: The role of financial knowledge, satisfaction, and confidence. Financial Services Review, 291-305.

- Sekita, S. (2011). Financial literacy and retirement planning in Japan. Journal of Pension.Economics and Finance, 637 - 656.

- Swee Lian, M. (2008). Youth Financial literacy:Development, delivery and execution.International conference of education.

- Xiao, J. (2011). Antecedents and Consequences of Risky Credit Behavior Among College Students: Application and Extension of the Theory of Planned Behavior. American Marketing Association, 239-245.

- Garman, E., & J.Gappinger, A. (2008). Delivering Financial Literacy Instruction to Adults. Association for Financial Counseling and Planning Education, 324-3147.

- Rooij, M. C., Lusardi, A., & J.M.Alessie, R. (2011). Financial literacy and retirement planning in the Netherlands. Journal of Economic Psychology, 593-608.

- Alena C, J. (2001). Evaulating a financial assessment tool: The Financial Checkup. Retrieved from http://digitalcommons.usu.edu/etd/2539/.

- Blalock, L. L., Tiller, V. R., & Monroe, P. A. (2004, Vol 53, No 2). ‘‘They Get You Out of Courage:’’ Persistent Deep Poverty AmongFormer Welfare-Reliant Women. Family Relations, 127-137.

- G. J., & Joo,S.H. (2006). Student racial differences in credit card debt and financial behaviors and stress. College Student Journal, 400-408.

- Allen, M. W., Edwards, R., Hayhoe, C. R., & Leach, L. (2007). Imagined interactions, family money management patterns and coalitions, and attitudes toward money and credit. Journal of Family and Economic Issues, 3-22.

- OGGINS, J. (2003). TOPICS OF MARITAL DISAGREEMENT AMONG AFRICAN-AMERICAN AND EURO-AMERICAN NEWLYWEDS. Psychological Reports, Vol92, issue 2, 419-425.

- Schmeiser, M. D., & Seligman, J. S. (2013). Using the Right Yardstick: Assessing Financial Literacy Measures by Way of Financial Well-Being. Journal of Consumer Affairs, 243-262.

- LUSARDI, A., & MITCHELL, O. S. (2011). Financial literacy and retirement planning in the United States. Journal of Pension Economics and Finance, 509-525.

- FONSECA, R., MULLEN, K. J., ZAMARRO, G., & ZISSIMOPOULOS, J. (2012). What Explains the Gender Gap in Financial Literacy? The Role of Household Decision Making. Journal of Consumer Affairs, 90-106.

- Lusardi, A., & Tufano, P. (2009). Debt Literacy, Financial Experiences, and Overindebtedness. Retrieved from National Bureau of Economic Research, Inc working paper: http://www.nber.org/papers/w14808

- PERRY, V. G., & MORRIS, M. D. (2005). Who Is in Control? The Role of Self-Perception, Knowledge, and Income in Explaining Consumer Financial Behavior. Journal of Consumer Affairs, Volume 39, Issue 2, pages 299-313.

- Rooij, M. C., Lusardi, A., & Alessie, R. J. (2011). Financial literacy and retirement planning in the Netherlands. Journal of Economic Psychology, Volume 32, Issue 4, Pages 593–608.

- STANGO, V., & ZINMAN, J. (2009). Exponential Growth Bias and Household Finance. The Journal of Finance,Volume 64, Issue 6, 2807–2849.

- Mottola, G. R. (2013). In our best interest: Women, financial literacy, and credit card behaviour. Numeracy, Vol. 6: Iss. 2, Article 4..

- Atkinson, A., & Messy, F.-A. M. (2012). Measuring Financial Literacy: Results of the OECD / International Network on Financial Education (INFE) Pilot Study. Retrieved from http://dx.doi.org/10.1787/5k9csfs90fr4-en

- Brown, M., & Graf, R. (2013). Financial Literacy and Retirement Planning in Switzerland. Numeracy: Vol. 6: Iss. 2, Article 6.

- Lusardi, A., & Wallace, D. (2013). Financial Literacy and Quantitative Reasoning in the High School and College Classroom. Numeracy: Vol. 6: Iss. 2, Article 1.

- Shambare, R., & Rugimbana, R. (2012). Financial literacy among the educated: An exploratory study of selected university students in South Africa. Thunderbird International Business Review, Volume 54, Issue 4, 581–590.

- Chen, H., Volpe, R. P., Mandell, L., & Klein, L. S. (1998,2009). An analysis of personal financial literacy among college students,The Impact of Financial Literacy Education. Financial Services Review,Journal of Financial Counseling and Planning Volume 20, Issue 1, Volume 7, Issue 2, Pages 107–128.

- Manton,. E., English,. D., Avard,. S., & Walker,. J. (2006). What college freshmen admit to not knowing about personal finance. Journal of College Teaching and Learning, 3(1), 12.

- Comeau.T, M. M., & Rhine,. S. (2000). Delivery of financial literacy programs. Consumer and Community Affairs Division 7,12.

- Pillai,. R., Carlo,. R., & D'souza,. R. (2010). Financial prudence among youth. Munich Personal RePEc Archive.

- Cummins,. M., Haskell,. J., & Jenkins,. S. (2009). Financial attitudes and spending habits of university. Journal of Economics and Economic Education Research, 10(1), 136, page 11.

- Danes,. S., Huddleston-Casas,. C., & Boyce,. L. (1999). Financial planning curriculum for teens. impact evalutaion Financial Counseling and Planning, 10(1), 14.

- Danes,. S. (1994). Parental perceptions of children's financial socialization. Financial Counseling and Planning 5, 23.

- Henry,. R., Weber,. J., & Yarbrough,. D. (2001). Money management practices of college students. College Student Journal 35(1), 6.

- Micomonaco,. J. (2003). Borrowing against the future: practices, attitudes and knowledge of financial management among college students.

- Ronald, P. V., Haiyang, C., & Joseph, J. P. (1996). Personal Investment Literacy Among College Students: A survey. Financial Practice and Education, 6(2), 10.

- Greenberger,. E., & Steinberg,. L. (1986). When teenagers work: the psychological and social costs of adolescent employment,(Vol. 9, pp. 10). New York.

- Pillai,. R., Carlo,. R., & D'souza,. R. (2010). Financial prudence among youth. Munich Personal RePEc Archive.

- Roy, M. (2003). ANZ survey of adult financial literacy in Australia - final report (pp. 81). Retrieved from ANZ: http://www.anz.com/aus/aboutanz/Community/Programs/FinLitResearch.asp

- Potrich, A., Vieira, K., & Coronel, D. (2015). Financial literacy in Southern Brazil: Modeling and. Journal of Behavioral and Experimental Finance, 1-12.

- REMUND, D. L. (2010). Financial Literacy Explicated: The Case for a Clearer Definition in an Increasingly Complex Economy. Journal of Consumer Affairs, Volume 44, Issue 2, pages 276–295.

- S, S., BL, B., NA, C., JJ, X., & J, S. (2010). Financial socialization of first-year college students: the roles of parents, work, and education. journal of youth Adolesc, 39(12):pages 1457-70.

- S., S., Xiao, X., J.J, Barber, B.L., B., & Lyons,. A. (2009). Pathways to life success: A conceptual model of financial well-being for young adults. Journal of Applied Developmental Psychology, 30 (6). pp. 708-723.