American Journal of Business and Society, Vol. 1, No. 4, November 2016 Publish Date: Aug. 16, 2016 Pages: 189-194

The Implications of Money Supply on Interest Rate in Nigeria

The Implications of Money Supply on Interest Rate in Nigeria

Yunana Titus Wuyah1, *, Amba Daniel Amwe2

1Department of Economics and Management Science, Faculty of Social and Management Sciences, Nigeria Police Academy, Wudil, Kano, Nigeria

2Department of Demographic and Social Statistics, National Bureau of Statistics, National Headquarters, Abuja, Nigeria

Abstract

The paper examined the implication of money supply on interest rate in Nigeria for the period of sixteen years (2000-2016) using multiple regression model. Ordinary least squared was used in estimating the regression model. We first test for the presence or non-presence of unit root on the variables. The unit root result showed that that all the variables were stationary after the first difference. The OLS result showed that money supply and exchange rate have negative implication on interest rate while inflation rate has positive implication. The regression model is a good fit as the coefficient of determination showed that 76% of the variation in interest rate is explained by all the explanatory variables (money supply, inflation rate and exchange rate). The t-value also indicated that both money supply and exchange rate has significant influence on interest rate. We therefore recommend increase in money supply into the economy which will consequently reduce interest rate, increase investment and boost economic growth in the Country. The monetary authorities (Central Bank of Nigeria) should pay special attention on broad money supply (M2) by manipulating instruments like the liquidity ratio, reserve ratio, among others which directly affects the monetary aggregate M2 for managing the economy.

Keywords

Money Supply, Interest Rate, Inflation Rate, Exchange Rate, Central Bank

Received: June 6, 2016

Accepted: June 16, 2016

Published online: August 16, 2016

@ 2016 The Authors. Published by American Institute of Science. This Open Access article is under the CC BY license. http://creativecommons.org/licenses/by/4.0/

Contents

1. Introduction 2. Literature Review and Theoretical Framework 2.1. Literature Review 2.2. Theoretical Framework 3. Research Methodology 3.1. Sources of Data and Techniques of Analysis 3.2. Model Specification 3.3. Research Hypotheses 3.4. Presentation and Analysis of Results 4. Conclusion and Recommendations

1. Introduction

The ultimate effect of money on the real economy has always been of great concern to economists and monetary policymakers[1]. The Classical and New Classical Economics, namely the traditional approach proposes that money supply has no any significant implication on interest rates. This approach completely relies on The Quantity Theory of Money and assumes a dichotomy between monetary and real sectors, known as classical dichotomy. Its main hypothesis is that the real money demand of people is fixed, so that there is a direct relation between money supply (Ms) and price level (P) [2]. A change in money supply induces price level to change through the same direction and by the same proportion. The traditional approach hypothesizes that the interest rate is determined in the real sector by investment demands and loanable funds. The causality is from quantity of investment demands and loanable funds to interest rates [3]. Thus, this framework excludes interest rates from monetary analysis. But the Liquidity Preference framework refuses the classical dichotomy and implicates an inverse relation between money supply and interest rates. The Keynesian economics implicates an indirect relation between money supply and price level. This indirect relation is determined by interest rates and unemployment. However, Monetarists argue that the liquidity effect is not the ‘whole story’ [2]: Money supply will have other effects on the economy that may make interest rates rise, such as income effect, price level effect and expected inflation effect. Whether monetary authorities could or not affect interest rates by determining money supply variables depends on these factors.

The central bank defines money supply in two ways: narrow and broad money. Narrow money (M1) is defined to include currency in circulation plus current account deposits with commercial banks. Broad money measures the total volume of money supply in the economy and is defined as narrow money plus savings and time deposits with banks including foreign denominated deposits. There is excess money supply when the amount of money in circulation is higher than the level of total output of the economy. When money supply exceeds the level the economy can efficiently absorb, it dislodges the stability of the price system, leading to inflation or higher prices of goods. In this brief, we shall examine how a change in money supply by the CBN affects people and the economy. In subsequent series, we shall look at the effects of an increase/decrease in interest rate and the effects of depreciating/ appreciating the exchange rate on the people and the economy [4].

The interest rate is a key tool of monetary policy. In October 2001, the European Central Bank stated that it had not changed interest rates because it considered current rates "consistent with the maintenance of price stability over the medium term [5]. In May 2001, Brazil’s central bank "increased interest rates" because it was "worried about mounting inflationary pressure," [6]. And in the first half of 2000, the U.S. Federal Open Market Committee increased the federal funds rate target three times in order to head off "inflationary imbalances" [7]. The central bank of Nigeria recently increases the MPR by 25 basis points from 6.0 to 6.25 per cent; in other to curb inflation in the country, [8].

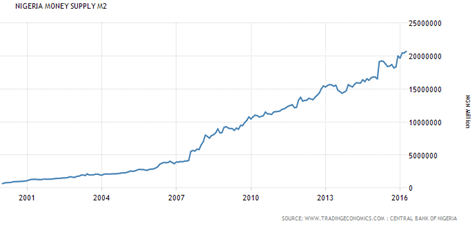

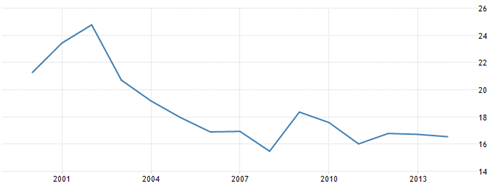

Money Supply M2 in Nigeria increased to 20727909.47 NGN Million in April from 20470436 NGN Million in March of 2016. Money Supply M2 in Nigeria averaged 7939691.37 NGN Million from 2000 until 2016, reaching an all-time high of 20727909.47 NGN Million in April of 2016 and a record low of 648506.60 NGN Million in January of 2000. Money Supply M2 in Nigeria is reported by the Central Bank of Nigeria. Nigeria Money Supply M2 includes M1 plus short-term time deposits in banks. There is a significant growth of money supply over the period under review while interest rate continues falling as indicated in figure 1 and 2 respectively.

Figure 1. Growth of broad money supply (January, 2000 – June 2016).

Figure 2. Trend of Interest rate in Nigeria (January, 2000 – June, 2016).

Source: Tradfingeconomic.com/Central Banks of Nigeria, 2016

The central bank of Nigeria kept its benchmark interest rate unchanged at 12 percent at its May 2016 meeting, despite surging inflation, contracting economy and rising unemployment while market expected a hike of 100 bps. Policymakers also voted for a greater-flexibility in exchange rate after it has been pegged for 15 months. Interest Rate in Nigeria averaged 10.10 percent from 2007 until 2016, reaching an all-time high of 13 percent in November of 2014 and a record low of 6 percent in July of 2009. Interest Rate in Nigeria is reported by the Central Bank of Nigeria. In Nigeria, interest rate decisions are taken by The Central Bank of Nigeria. The official interest rate is the Monetary Policy Rate (MPR).

Therefore, this study aims at analyzing the economic implication of money supply on interest rate in Nigeria for the period of sixteen years from January, 2000 to June, 2016. The research work is structure into five sections: the introduction, literature review and theoretical framework, research methodology, presentation and analysis of results and finally conclusion and recommendations.

2. Literature Review and Theoretical Framework

2.1. Literature Review

The empirical works of this study were carried out in determining the economic implications of money supply on interest rate in Nigeria. The Central Bank of Nigeria (CBN) takes a number of monetary policy decisions, including a change in the level of money supply (M2), the Minimum Rediscount Rate (MRR), or a change in the exchange rate. The central bank defines money supply in two ways: narrow and broad money. Money supply has economic implication on macroeconomic variables such as interest rate, inflation rate, and exchange rate among others.

Omiete and Onyemachi [9] examined the impact of Broad Money supply (M2) on Asset prices in Nigeria. Monthly data, in logarithmic form, was used for the period 2008M1-2013M12. The Unit root test show that the variables were stationary after being first differenced; at the 5% significance level. The Johansen Co-integration test gave evidence of one co-integrating equation which explains that a long-run equilibrium relationship exist between LogSMC and LogBMS. The Vector Error Correction Model was used to analyze short-run adjustment dynamics and showed -0.08% speed of adjustment of prior deviations from equilibrium. Thus, about 8% of disequilibrium is corrected monthly. The Granger Causality test demonstrates a Unit-directional causality from LogBMS→LogSMC. Furthermore, the Impulse Response and Variance Decomposition test indicate both positive and negative shocks which are in consistent with our findings from the VECM and Granger causality analysis. Overall, all the results obtained are in line with a priori expectation.

Tariq, Muhammad and Tariq [10] investigate the impact of inflation, interest rate and money-supply on volatility of exchange rate in Pakistan. To estimate short and long run relationship among variables, monthly data for the period ranging from July-2000 to June-2009 have been analyzed by applying Johansen Co-integration (trace test & eigenvalue) Tests) and Vector Error Correction Model (VECM). Granger Causality Test and Impulse Response Function (IRF) have also been applied to determine effect and response to shock of variables on each other. The results reveal that the short run as well as long run relationships exist between inflation and exchange rate volatility. High money supply and increase in interest rate raises the price level (inflation) which leads to increase in exchange rate volatility.

Muhammad & Mubarak [11] examined the relationship between money supply, interest rate, income growth and inflation rate in Nigeria for the period 1980-2010 by employed a co-integration method, VAR, and Granger causality test to examine the relationship among the variables. Based on this approach, the paper found that there is no long run relationship among the variables and granger causality test shows a bidirectional relationship between money supply and inflation, income growth and inflation and interest rate and inflation. The granger causality test also revealed that money supply, interest rate, and income growth all granger cause inflation.

Abbas and Husian [12] examines the casual relationship between money and income and money and prices in Pakistan. The co-integration analysis indicates, in general, the long run relationship among money, income and prices. The error correction and Granger causality framework suggest a one-way causation from income to money in the long run implying that probably real factors rather than money supply have played a major role in increasing Pakistan’s national income, regarding the causal relationship between money and prices, the causality frame work provides the evidence of bi-variate causality indicating that monetary expansion increases and is also increased by inflation in Pakistan. However, money supply seems to be the leader in this case.

Marcus Hagedorn [13] studies the joint business cycle dynamics of inflation, money growth, nominal and real interest rates and real money demand. He extends and estimates a standard cash and credit monetary model by adding two features: idiosyncratic preference shocks to cash consumption, and a banking sector. The estimated model accounts very well for the business cycle data, a result that standard monetary models have not been able to generate. He find-out that the quantitative performance of the model is explained through substantial liquidity effects.

Holod [14] investigates the identified vector auto-regression to model the relationship between CPI, money supply and exchange rate in Ukraine. The results show that exchange rate shocks significantly influence price level behaviour. Further, the study also found that money supply responds to positive shocks in price level.

Asogun [15] examined the influence of money supply and government expenditure on gross domestic product. He adopted the Saint Louis model on annual and quarterly time series data from 1960-1995. He finds money supply and export as being significant on the determinant of economic growth in the Nigerian economy. The result indicated that unanticipated growth in money supply would have positive effect on output.

Ganley and Salmon [16] demonstrate that monetary policy has an asymmetrical effect on real output if prices are less flexible downwards than upwards. It has been suggested that negative money-supply shocks and/or increases in interest rates reduce output more than monetary expansions raise it. Monetary policy may cause asymmetric output responses if asymmetric information the banking sector produces binding credit constraints.

2.2. Theoretical Framework

Quantity theory of Money: The basic premise or idea that forms the basis for this reasonable line of argument is to seek to answer the question ‘what determines the demand for money?’ as a result; there are different theories of demand for money by different schools of thought.

(a) The Fisher’s version of the quantity theory of money is formally expressed as:

MV = ∑PQ (1)

Fisher’s simplified the version of the equation as:

MV = PT (2)

Each variable denotes the following:

M → represents the quantity of money in circulation

V→ is the transaction velocity of money

P→ is weighted average of all individual prices and P = MV/T

T→ is the sum of all the transactions of goods and services per unit of time.

The Fishers theory assumes that; V (velocity of money) and T (volume of transactions are constant in the short term) that the quantity of money, which is determined by outsides forces, is the main influence of economic activities in a society. The theory also assumes that the economy is in equilibrium and at full employment. Essentially, the theory’s assumptions imply that the value of money is determined by the amount of money available in an economy.

From equation (2), when V and T are constant, changes in M will lead to proportionate change in P.

(b) The classical modification of the model called income version of quantity theory of money was expressed as:

MV = PY (3)

Where Y is the physical output which include all exchanges which is the same as real income in social accounting sense.

The assumption of this theory is that, Y is constant. Therefore, equation… (3) Implies that a rise in money (Y remaining constant) results in a proportional rise in price. When money supply increases, it increase the cash balance at the disposal of the people. People do not prefer to hold idle cash balance. They spend it on goods and services. An increase in money expenditure, while Y is held constant, means aggregate demand increases while aggregate supply is fixed. The ultimate result is rise in price; Price rise because production cannot be increased in the short run.

(c) Cambridge reformation of the model came under the leadership of Marshal and Pigou. They expressed their equation as:

Md = KPQ (4)

Where Md is demand for money, P is the price, Q is the real income and K is the proportion of money held as currency and bank deposits. Equation … (4) means that the demand for money (Md) equal K proportion of the total money income. They claimed that, K is fairly stable and that, at equilibrium level, stock of money (M) equals demand for money (Md) that is

M = Md = KPQ (5)

At equilibrium,

M = KPQ (6)

or

M (1/k) = PQ (7)

According to this version, price level is affected only by that part of money which people hold in the form of cash for transaction purpose, not by the total MV as suggested by the classical theory.

3. Research Methodology

3.1. Sources of Data and Techniques of Analysis

The method used for this study is the ordinary least square (OLS) method because it has the Best, linear, Unbiased Estimator (BLUE). Another reason being that its computational procedure is fairly simple compared with other econometric techniques with data requirements not excessive.

We used the OLS methods and estimated the implications of money supply, inflation rate and exchange rate (independent variable) on interest rate (dependent variables). The study sourced it data from central Bank of Nigeria and National Bureau of statistics. Then, the computer software package used and obtained the results was the econometric-view version 4.0.

3.2. Model Specification

The specification of econometric model is based on econometric theory and on any valuable information relating to the phenomenon being studied. The study build a multiple regression model to estimated and analyze the implications of the explanatory variables on the dependent variable in Nigeria. The functional relationship of the model is expressed as:

ITR = F (MS, INF, EXR) (8)

Equation (8) is explicitly transformed into the following:

ITRt = β0 + β1 MSt + β2 INFt + β3 EXRt + Ut (9)

Where: MS = Broad money supply

ITR = Real Interest rate

INF = Inflation rate

EXR = Real Exchange Rate

β0, β1, β2, and β3 = Parameter

Ut = Error term

3.3. Research Hypotheses

Based on the available data, this work is interested in testing out the hypothesis below;

H0: The implications of money supply on interest rate, inflation rate and exchange rate in Nigeria over the years is not significant.

H1: The implications of money supply on interest rate, inflation rate and exchange rate in Nigeria over the years is significant.

3.4. Presentation and Analysis of Results

In other to estimate the equation, we performed stationary test on all the variables using the Philip Perro Test and all the variables were stationary after first difference. We therefore proceed and the regression model and the results presented and evaluated below:

ITR = -2.941 – 0.84MS + 0.65INF – 0.035EXR

t = (-1.94) (-3.871) (-0.27)(24.10)

R2 = 0.85 R-2 = 0.76, F = 111.214 Dw = 2.00

The coefficient of the variable of real interest rate (ITR) is – 0.84, signifying that a unit change in real interest rate will bring about 84% change (decrease) in money supply in the country. The t-value which measure the significant contribution of the variable to the dependent variable is (-3.871). Since the value of above 2 in absolute term (rule of thumb), we conclude that money supply is significant in influencing interest rate in Nigeria.

The coefficient of inflation rate (INF) is 0.65 with t-value of -0.27 depicting that a unit change in inflation rate will bring about 27% increase in interest rate but the variable is not significant as the t-value is below 2 in absolute term.

Exchange rate coefficient is – 0.035. This shows that a unit change in real exchange rate will bring about a 3% decrease in interest rate. The variable is significant in influencing interest rate as indicated by the t-statistics.

The coefficient of multiple determinations (R2) is used to check the goodness – of- fit of the regression model. From the regression result, the value of R-2 is 0.76 which implies that in the Long run, 76% of the variation in real interest rate (ITR) is explained by the explanatory variables (broad money supply, inflation rate and exchange rate). F statistics is carried out to determine if the explanatory variables in the model are simultaneously significant or not. Hence, the analysis shall be carried out under the hypothesis below,

HO:β1, β2 & β3 =0 (all slope coefficients are equal to [0])

H1:β1, β2 & β3 ¹ 0 (all slope coefficients are not equal to zero [0])

Decision Rule: Reject H0 if F – cal > F – tab at 5% level of significance. Our F-value is 111.214 which is far above the tabulated. We therefore, conclude that all the explanatory variables are significant in influencing the dependent variable.

Finally, the test for autocorrelation (DW) is aimed at ascertaining if autocorrelation occurred in the model. The DW value of 2.00 means that, there is no presence of autocorrelation in the model as the value is 2.

4. Conclusion and Recommendations

The study examined the implications of money supply on interest rate in Nigeria for the period of sixteen years (2000 – June, 2016). Money supply has been a powerful macroeconomic variable influencing the economy. The study adopted ordinary least square technique to estimate the regression model after subjecting the variables to unit root test. The results showed that, all the variables were stationary after the first difference. The regression result indicated that, money supply and exchange rate have negative implication on interest rate while inflation rate has positive implication but both money supply and exchange rate has significant influence on interest rate. We therefore recommend increase in money supply into the economy which will consequently reduce interest rate, increase investment and boost economic growth in the Country. The monetary authorities (Central Bank of Nigeria) should pay special attention on broad money supply (M2) by manipulating instruments like the liquidity ratio, reserve ratio, among others which directly affects the monetary aggregate M2 for managing the economy.

References

- Anyanwu, J.C. (1993) "Monetary Economics, Theory and Institution" Onitsha: Hybrid Publisher Limited.

- Mishkin, Frederic S. (1989) "The Economics of Money, Banking and Financial Markets." Second Edition, Scot, Foresman and Company, Boston.

- Anyanwu, J.C., Oyefusi, A, Oaikhenan, H. and Dimowo, F.A. (1997) "The Structure of The Nigeria Economy (1960 – 1997)." Awka: Joanne Educational Publishers Ltd.

- Central Bank of Nigeria, (2006) "Annual Report and Statement of Account. (December 2006).

- European Central Bank (2001) monetary policy decision.

- New York Time, Rich 2001.

- Afolabi, O.L. (1999) "Monetary Economics" Nigeria" Heineman Educational Book PLC.

- Central Bank of Nigeria Communiqué No. 69 of the Monetary Policy Committee Meeting, April 15, 2010.

- Omiete Victoria Olulu-Briggs and Onyemachi Maxwell Ogbulu (2015)"Money Supply and Asset Prices in Nigeria (2008-2013): An Empirical Review"Research Journal of Finance and Accounting,ISSN 2222-1697 (Paper) ISSN 2222-2847 (Online).

- Tariq Mahmood Ali, Muhammad Tariq Mahmood and Tariq Bashir (2015) "Impact of Interest Rate, Inflation and Money Supply on Exchange Rate Volatility in Pakistan" World Applied Sciences Journal 33 (4): 620-630, 2015, ISSN 1818-4952.

- Muhammad Zayyanu Bello & Mubarak Abdullahi Saulawa (2013) "Relationship between Inflation, Money Supply, Interest Rate and Income Growth (Rgdp) in Nigeria 1980-2010. An Empirical Investigation."Journal of Economics and Sustainable Development, Vol.4, No.8, 2013.

- Fazal Husain & Kalbe Abbas (2006) "Money, Income, Prices, and Causality in Pakistan: A Trivariate Analysis." The Pakistan Development Review.

- Marcus Hagedorn (2009) ‘Money, Interest Rates and Strong Liquidity Effects’ university of Zurichy.

- Holod, D. (2000) "The Relationship between Price Level, Money Supply and Exchange Rate inUkraine".

- Asogu, J.O., (1998) "An Econometric Analysis of relative potency of monetary policy in Nigeria." Economic model on economic growth; the findings albeit support Fin. Rev, pp: 30-63.

- Ganley, J. and Salmon, C. (1997) "The industrial impact of monetary policy shocks: some stylized facts," Bank of England, Working Paper no. 68.