American Journal of Business and Society, Vol. 1, No. 4, November 2016 Publish Date: Aug. 16, 2016 Pages: 183-188

The Evaluation of the Relationship between Market Capitalization and Macroeconomic Variables in Emerging Market

Alayemi Sunday Adebayo*

The Federal Polytechnic, School of Business and Management Studies, Department of Accountancy, Nigeria

Abstract

The study evaluated the relationship between market capitalization and macroeconomic variables, in emerging market. In the study all the entire companies whose shares were traded on the Nigerian Stock Exchange were studied from 1988 -2012 spanning a period of 25 years. Data were collected from the stock exchange market and Federal office of statistics. The main objective of the study is to evaluate the relationship between market capitalization and macroeconomic variables. The specific objectives from the main objective is to evaluate the relationship between market capitalization and each of the components of macroeconomic variables, that is, interest rate, inflation rate, lending rate, gross domestic product and unemployment rate. The overall result revealed that macroeconomic variables are the drivers of market capitalization. Multiple regressions were employed to investigate the relationship between market capitalization and components of macroeconomic variables. The results showed that there was negative effect of interest rate, inflation rate, lending rate and unemployment on market capitalization at varying degree. In the final analysis, the result showed that there was relationship but not significant between market capitalization and components of microeconomic variables.

Keywords

Market Capitalization, Nigerian Stock Exchange, Macroeconomic Variables, Interest Rate, Inflation Rate

Received: May 28, 2016

Accepted: June 6, 2016

Published online: August 16, 2016

@ 2016 The Authors. Published by American Institute of Science. This Open Access article is under the CC BY license. http://creativecommons.org/licenses/by/4.0/

Contents

1. Introduction 2. The Conceptual Framework 2.1. Interest Rate 2.2. Inflation 2.3. Other Macroeconomic Variables 3. Literature Review 4. Gap in the Literature 5. Methodology 5.1. Dependent Variable 5.2. Explanatory Variables (Independent Variables) 5.3. Model Specification 6. Analysis of Data 7. Conclusion Appendix

1. Introduction

Businesses are impacted by economic factors with varying degree effects in accordance with the types of business. For instance, general price level would have fewer effects or impact to a utility company as opposed to other companies in another industry for example, products and services. Therefore, stock market indices are often used because of its value as a parameter to gauge how healthy the economy of a country is. Stock market index consist of prices and capitalization of selected shares in the market. Therefore, market value is commonly used to refer to the market capitalization of a publicly-traded company, and is obtained by multiplying the number of its outstanding shares by the current share price. Hence, macroeconomic variables determine to a larger extent the financial performance as reflected in the operation of the stock exchange market. The main thrust of this paper is to evaluate the impact of macroeconomic variables on market value/capitalisation of companies quoted on the Nigerian Stock Exchange. The secondary objective would concentrate on the relationship between market value/capitalisation of each of the macroeconomic variable (interest rate, lending rate, inflation rate, gross domestic product and unemployment rate).

2. The Conceptual Framework

In order to fully understand what drives market value/ capitalization, it is important to first understand the macroeconomic factors that bring about the changes.

2.1. Interest Rate

Interest rates as set by the central bank have a direct relationship on the economy as a whole and hence the stock market. When the economy is stagnating and not growing as desired by the central bank and government, the central bank has option other than to use expansionary monetary policy. It implies that the central bank increases the supply of money and hence lowering the interest rates in order to, for instance, raise inflation. The expected outcome is then that money will become cheaper and thus create demand for consumers goods and others to start investing and spending, thereby stimulating the economy. If the central bank on the other hand wants to slow down the economic activity, it can reduce the money supply in the economy and increase the bank rate [1]. Basic macroeconomic theory implies that interest rates should therefore affect the stock returns. When interest rates are low it also entails that investors cannot get a considerably high return, for instance bank deposits and therefore seek to other investments, usually stocks.

2.2. Inflation

Inflation is usually something that especially economics take very seriously and is often the primarily goal to attain. A rising inflation usually has a negative impact on stock returns. When inflation increases, prices get higher which implies that consumers no longer can afford to buy goods and services to the same extent as before? This will in turn lower revenues and profits and eventually result in a decline in the stock market. Rising inflation should hence have an insidious effect on the stock market where it could take time for consumers and producers to be acclimated [2].

2.3. Other Macroeconomic Variables

The following are other macroeconomic instruments that are important for a country's economy. One commonly used gauge is gross domestic product (GDP) which is used to measure the economic wealth of a country. Gross domestic product per capita is often a more genuine measure since it takes the population into consideration. Whether this measurement corresponds to the well-being of a country is disputable but it is still employed to a great extent to compare different countries. It could also indicate the wealth of the companies and accordingly be reflected on the stock market. As there are different schools of thoughts, to what extent this holds is arguable since some studies show no real correlation between gross domestic product growth and equity returns [3].

Nor this is \all; unemployment rate is also something well-measured and could be used to signify a country's well-being. There is, according to basic macroeconomic theory, a direct link between short-term unemployment rate and inflation through the Phillips curve. To therefore have a stable unemployment rate is a prerequisite for a stable inflation and vice versa [4]

3. Literature Review

In the work of [5] investigation was carried out on the long-run relationship and the short-run dynamics among macroeconomic fundamentals and the stock returns of Germany and the United Kingdom. Each case was examined individually, by applying Johansen co-integration, error correction model, variance decomposition and impulse response functions, in a system incorporating the variables such as consumer price index (CPI), interest rates, exchange rates, money supply and industrial productions between the periods of February 1999 to January 2011. The Johansen cointegration tests showed that the UK and German stock returns and chosen five macroeconomic variables are cointegrated. The findings also indicated that there are both short and long run causal relationships between stock prices and macroeconomic variables.

Furthermore, [6] attempted to present several classifications of macroeconomic variables, with the objective of selecting macroeconomic variables for seeking their relationship with stock market prices, and, subsequently, to define what macroeconomic variables have positive and what macroeconomic variables have negative effects on stock market prices in Lithuania in the short run. Augmented Dickey Fuller test has been employed to check the stationarity of the selected time series since a spurious regression may occur if a time series is not stationary. The results of the paper clearly indicated that macroeconomic variables are significant determinants for stock market prices in Lithuania. Gross domestic product and money supply have a positive effect on stock market prices while most of the time unemployment rate, exchange rate, and short-term interest rates negatively influence stock market prices. The findings of the paper are similar to the results of some other empirical studies.

Another study by [7] was undertaken to evaluation of the effect of macroeconomic variables on stock market prices using annual time series datasets for Nigeria for the period 1980-2013. The data were analyzed with the application of OLS regression technique. The study employs Johansen cointegration and VECM based on arbitrage pricing theory (APT) of [8]. The macroeconomic variables utilized were gross domestic product (GDP) and broad money supply (M2). The results of the findings indicated that Nigerian stock market prices had long-run relationship with macroeconomic variables. However, GDP had significant long-run negative effect on stock prices contrary to a priori expectation that GDP has significant positive effect on stock prices. But M2 has significant long-run positive effect on stock prices, the result being consistent with a priori expectation. Again, there is unidirectional causal effect between GDP and stock prices with direction running from stock prices to GDP. Whereas there is no causal effect between stock prices and broad money supply. However, in the short-run both GDP and M2 have positive but insignificant effect on stock prices in Nigeria. This result suggests that stock market in Nigeria is informational inefficient. It shows that predicting stock prices based on macroeconomic factors is difficult.

A dynamic study by [9] was on the relationship between share prices and a macroeconomic variable is well documented for the United States and other major economies. However, what is the relationship between share prices and economic activity in emerging economies? The goal of the study is to investigate the time-series relationship between stock market index prices and the macroeconomic variables of exchange rate and oil price for Brazil, Russia, India, and China (BRIC) using the Box-Jenkins ARIMA model. Although no significant relationship was found between respective exchange rate and oil price on the stock market index prices of either BRIC country, this may be due to the influence other domestic and international macroeconomic factors on stock market returns, warranting further research. Also, there was no significant relationship found between present and past stock market returns, suggesting the markets of Brazil, Russia, India, and China exhibit the weak-form of market efficiency.

Additionally,[10 and11] indicated that stock market prices and money supply are positively related in Nigeria. However, contrary to these results, [12 and 13] showed that stock prices relate negatively with money supply in Nigeria. [14] tested the Granger-causality between stock prices and money supply. The results indicate that money supply does not Granger-cause stock prices.

In the same vein, [15], in his study examined the relationship between the stock market and selected macroeconomic variables in Nigeria. The all share index was used as a proxy for the stock market while inflation, interest and exchange rates were the macroeconomic variables selected. Employing error correction model, it was found that a significant negative short run relationship exists between the stock market and the minimum rediscounting rate (MRR) implying that, a decrease in the MRR, would improve the performance of the Nigerian stock market. It was also found that exchange rate stability in the long run, improves the performance of the stock market. Though the results for Treasury bill and inflation rates were not significant, the results suggests that they were negatively related to the stock market in the short run thus, achieving low inflation rate and keeping the TBR low could improve the performance of the Nigerian stock market. Specifically, the study concludes that, by achieving stable exchange rates and altering the MRR, monetary policy would be effective in improving the performance of the Nigerian stock market.

4. Gap in the Literature

From the available literature, most of the researchers carried out researches on the influence of macroeconomic variables on market value on individual company quoted on the Nigerian Stock Exchange. The author has not known any research carried out on this topic that was made up of all the companies quoted on the Nigerian Stock Exchange Market.

5. Methodology

The nature of the study is quantitative from 1988-2012 which was done by gathering information from the secondary source. Data on macroeconomic variables were collected from the Federal Office of Statistics while that of market capitalization was collected from the Nigerian Stock Exchange (NSE). The choice of this method was informed by the fact that the events have already taken place which would be very difficult if not impossible to manipulate. Furthermore, it could be replicated by other researchers arriving at the same conclusion [16, 17 and 18].

5.1. Dependent Variable

In this study, dependent variable is market capitalisation of all the companies quoted on the Nigerian Stock Exchange

5.2. Explanatory Variables (Independent Variables)

Macroeconomic variables such as interest rate, lending rate, inflation rate, gross domestic product and unemployment rate. These variables were regressed against market capitalisation to show whether or not it has significant relationship with macroeconomic variables.

5.3. Model Specification

MAC = β0 + β1(INT) + β2(INF) + β3(LER) +β4(GDP)

+ β5(UMP) +ε

Where:

MAC = Market capitalization

INF = Inflation rate

LER = Lending rate

GDP = Gross domestic product

UMP = Unemployment rate

β0 is the intercept of the model. This is the level of market capitalisation the stock exchange market can sustain when macroeconomic variables would be considered irrelevant. β1(1=1,2,3,4,5) symbolized the coefficients (effects) of the respective components of macroeconomic variables on market capitalization. ε are the stochastic variables introduced in the model to cater for the influence of other variables that may shape market capitalization but which are not explicit included in the model.

6. Analysis of Data

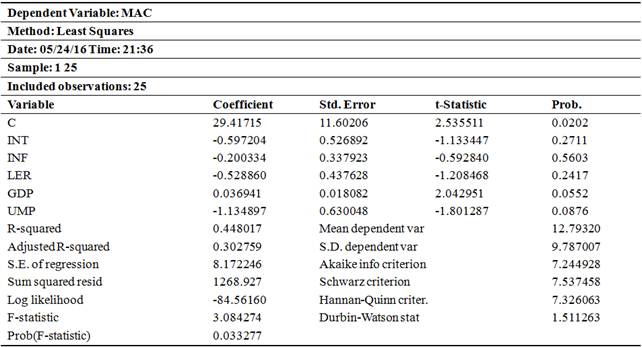

From the appendix, the value of DW is near 2. Hence there is no autocorrelation as far as the data are concerned [19].

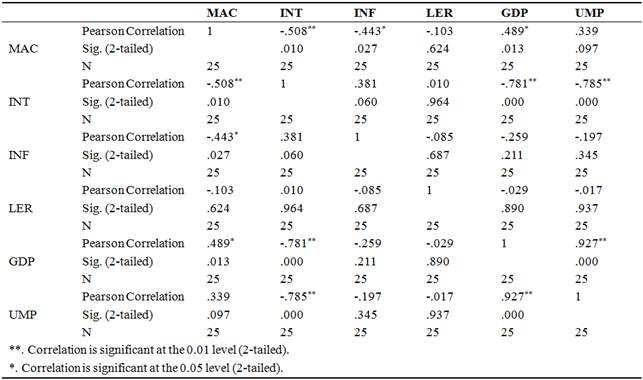

Table 1 showed correlation of the dependent variable (MAC) with each of the independent variables (INT, INF, LER, GDP and UMP). From the table, INT, INF and LER are negatively correlated with MAC at varying degree. While the correlation of MAC with INT and INF are significant (0.01 and 0.03) respectively, that of LER is not significant (0.62). on the other hand, GDP and UMP are positively correlated with MAC at varying degree. While the correlation between MAC and GDP is significant (.01) that of UMP is not significant (.10).

Table 1. Correlations.

Table 2 is the model summary. R-squared (R2) measured the proportion of the variation in the in the dependent variable (MAC) that was explained by variations in the independent variables (INT, INF, LER, GDP and UMP). The result as shown in this study was 45% of the variation (not the variance) was explained leaving 55% unexplained. Adjusted R-squared is a measurement of the proportion of the variance in the dependent variable (MAC) that was accounted for by variation in the independent variables (INT, INF, LER, GDP and UMP). In this study, 32% of the variance was accounted for while 68% was not accounted for.

Table 2. Model Summary.

Table 3. ANOVA.

The overall significance of the model was tested by the ANOVA as shown in Table 3. The result revealed that that the model is significant as shown by the value of F-statistic as 3.08 and Prob (F-statistic) that is p-value of 0.03 which is less than 0.05. The result is an indication that the data fit the model. Equally of importance from the ANOVA was that macroeconomic variables (INT, INF, LER, GDP and UMP) are drivers of market value/ capitalization. This means that there is significant relationship between market capitalization and micro economic variables.

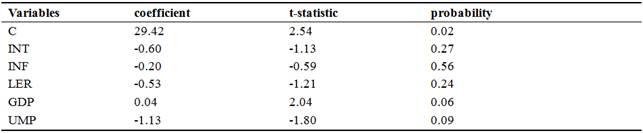

Table 4. Coefficients, T-statistic and probability.

Table 4 showed the multiple regressions to investigate the relationship between market capitalization and components of macroeconomic variables (INT, INF, LER, GDP and UMP). For the sake of emphasis the model is:

MAC = β0 + β1(INT) + β2(INF) + β3(LER) +β4(GDP) + β5(UMP) +ε

The coefficients of the variables are an indication that the predictor/explanatory variables made contribution to the variation in the dependent variable at varying degree as shown below:

MAC = 29.42 – 0.60INT – 0.20INF – 0.53LER + 0.04GDP – 1.13UMP + ε

p-value 0.27 0.56 0.24 0. 06 0.09

From the model, there is negative effect of INT, INF, LER and UMP. This showed, however, that as market capitalization (MAC) increases, there will be corresponding decrease in INT, INF, LER and UMP at varying degree. The degree of the significance was in the following order: -0.20(INF), -0.53(LER), -0.60(INT) and – 1.13(UMP). The associated p-value indicated that though INT, INF LER and UMP have relationship with the market capitalization, it is not significant. On the other hand there is positive but insignificant relationship between MAC and GDP. As GDP increases there will be corresponding decrease in MAC. This was confirmed by the p-value as indicated above.

7. Conclusion

The study evaluated the relationship between market value/capitalization and macroeconomic variables in emerging market. The main objective the research is to evaluate if any relationship between macroeconomic variables and market capitalization. Data spanning twenty five (25) years were collected from the Federal office of statistics and Stock Exchange in Nigeria. Multiple regressions with the aid of EViews software was used using Ordinary Least Square (OLS) method. Consideration of economic factors is very concomitant to the development of business organization as well as the capital market. The study showed relationship between market capitalization components of the macroeconomic variables (interest rate, inflation rate, lending rate, gross domestic product and unemployment rate) at varying degree. The overall result revealed that the drivers of market capitalization are the macroeconomic variables. Therefore, the happening in the economy must be considered by both the captains of the industry as well as the operators of the capital market.

Appendix

OUTPUT OF DATA ANALYSIS

References

- Jahan, S. (2012). Inflation targeting: Holding the line. IMF:Finance Development.

- Zucchi,K.(2013).Inflation'sImpactonStockReturns. http://www.investopedia.com/articles/investing/052913/inflations-impact-stock-returns.asp. [Online; accessed 2015-04-15].

- Wade, K. and May, A. (2013). GDP growth and equity market returns. http://www.schroders.com/en/SysGlobalAssets/staticfiles/schroders/sites/americas/us-institutional-2011/pdfs/equity-returns-and-gdp.pdf/. [Online; accessed 2015-04-15].

- Phelan, J. (2012). Milton Friedman and the rise and fall of the Phillips Curve. http://www.thecommentator.com/article/1895/milton_friedman_and_the_rise_and_fall_of_the_phillips_curve. [Online; accessed 2015-04-15].

- Mahedi Masuduzzaman(2012). Impact of the Macroeconomic Variables on the Stock Market Returns: The Case of Germany and the United Kingdom. Global Journal of Management and Business Research,Volume 12 Issue 16 Version 1.0. 23-34.

- Donatas Pilinkus, Vytautas Boguslauskas (2009). The Short-Run Relationship between Stock Market Prices and Macroeconomic Variables in Lithuania: An Application of the Impulse Response Function.Economics of Engineering Decisions,ISSN 1392–2785.

- Gabriel Nkechukwu, Justus Onyeagba and Johnson Okoh(2015).Macroeconomic Variables and Stock Market Prices in Nigeria: A Cointegration and Vector Error Correction Model Tests. International Journal of Science and Research, Volume 4, Issue 6, 717-724.

- Ross, S.A. (1976) The Arbitrage Theory of Capital Assets Pricing. Journal of Economic Theory 13: 340-362.

- Robert D. Gay, Jr.(2008). Effect Of Macroeconomic Variables On Stock Market Returns For Four Emerging Economies: Brazil, Russia, India, and China. International Business & Economics Research Journal,Volume 7, Number 3, 1-8.

- Maku, O. E. and Atanda, A. A (2011). Determinants of stock market performance in Nigeria: Long-run analysis. Journal of Management and Organizational Behaviour, 1(3).

- Adaramola, A. O. (2011).The impact of macroeconomic indicators on stock prices in Nigeria\Developing Countries Studies,1(2). Retrieved July 23, 2012, from www.iiste.org.

- Amadi, S. N., Onyema, J. I. and Odubo, T. D. (2002). Macroeconomic variables and stock prices: A multivariate analysis. African Journal of Development Studies, 2(1), 159-164.

- Isenmila, P. A. and Erah, D. O (2012). Share prices and macroeconomic factors: A test of arbitrage pricing theory (APT) in Nigerian stock market. European Journal of Business and Management, 4(15).

- Asaolu, T.O. and Ogunmuyiwa, M.S. (2011). An Econometric Analysis of the Impact of Macroeconomic Variables on Stock Market Movement in Nigeria. Asian Journal of Business Management, 3(1), 72-78.

- Terfa Williams Abraham (2008). Stock Market Reaction to Selected Macroeconomic Variables in the Nigerian Economy.CBN Journal of Applied Statistics Vol. 2 No.1, 61-70.

- Alayemi, Sunday Adebayo(2015). The impact of macroeconomic variables on all share index on the Nigerian stock exchange. Current Journal of Commerce and Management 01, 47-50.

- Alayemi, Sunday Adebayo and R. Ogunniyi Olajumoke(2015). Does debt impact equity returns? Journal of Global Economics, Management and Business Research, 6(2), 76-82.

- Alayemi Sunday Adebayo, Owolabi, Sunday Ajao and Sokefun Adeyinka Olawanle(2015). Going concern assessment through cash flow statements (A case study of Nigerian Breweries PLC). International Journal of Economics and Business Administration, Vol. 1, No. 2, 113-119.

- Kohler, R. (1994). Statistics for business and economics(3rd ed.). Harper Collins College Publishers.