International Journal of Economics and Business Administration, Vol. 2, No. 5, September 2016 Publish Date: Jul. 27, 2016 Pages: 45-52

Correlation Between Company’s Returns, Market and Book Value per Share in the Jordanian Shareholding Companies

Maswadeh Sana'a. N.*

Accounting Department, Jadara University, Jordan, Irbid

Abstract

Companies are interested in promoting and improving the value of its trading shares as higher book and market value of its shares reinforces the company's position and improves its credit reputation. Hence, the purpose of this study is to look at the nature of the correlation between company returns (return on assets and earnings per share), book value and market value per share. Also to analyze the nature of the correlation between market value and book value per share in different sectors belonging to the industrial, services, and financial segments in Jordanian shareholding companies during the period between (2008-2014). One of the highlights of the results of the study is the higher correlation to earnings per share and market value and book value per share compared with the return on assets and market value and book value per share in all sectors of the Jordanian shareholding companies. The results show that nearly all the correlation coefficients in the industrial and service sectors were closer to each other while the ones for the financial sector differed. Additionally, the study showed that there is high correlation between book value and market value per share in all sectors of the Jordanian shareholding companies, indicating that the change in book value per share leads to change in market value, and vice versa. Thus, the change in such value can be relied upon as an indicator of the change in the other values.

Keywords

Market Value of Share, Book Value of Share, Earnings Per Share, Return on Asset

Received: June 19, 2016

Accepted: July 11, 2016

Published online: July 27, 2016

@ 2016 The Authors. Published by American Institute of Science. This Open Access article is under the CC BY license. http://creativecommons.org/licenses/by/4.0/

Contents

1. Introduction 1.1. Statement of the Research Problem 1.2. Objective of the Study 1.3. Research Hypotheses 1.4. Significance of the Study 2. Theoretical Framework & Literature Review 3. Research Methodology 3.1. Population and Study Sample 3.2. Statistical Method 3.3. Measurement & Descriptive Statistics of Study Variables 4. Statistical Results 5. Conclusion and Recommendations

1. Introduction

Shareholding companies are dramatically and tangibly spreading at the moment and have become the basis of the underlying economies of most countries in the world. These companies are interested to promote and improve the market value of their trading shares, that consider as indicator of strengthens the company's position and improves their credit reputation, enabling them to finance from different sources and develop their resource funding and achieve earnings and the ability to continue and survive under the current severe economic situation and competition.

Earnings realized by the shareholding companies are considered as basic information that is relied upon by investors in making their investment decisions and stimulate financial markets and increase their efficiency. Therefore, this amplified the interest of financial markets to call attention to public shareholding companies to publish relevant and reliable accounting information that reflects the real performance of the public shareholding companies. Furthermore, investors try to ink stock prices such as market and book value to company returns to make their expectations and decisions; in addition investors build their expectations and decisions most often on many factors. These factors include the degree of company risk and number of shares traded on the market and the tradition of big investors, as well as traded rumors in the financial market and other factors [6]. Hence, this study aimed to look at the correlation between the return on assets and earnings per share with book and market value of the traded shares in the financial market. In addition, it also sought to analyze the nature of the correlation between book and market values of the shares and compare these values with each other and determine the differences between them in order to ascertain the interrelation between market and book value of shares.

1.1. Statement of the Research Problem

The problem of the study lies in investigating a correlation between earnings realized by the shareholding companies and market and book value of their shares, especially it suppose there is a positive relation between company’s returns and book and market value per share, and this, will attract investors and motivate them to keep and buy the company's shares. Ultimately, all these will reflect positively on the market value of the shares. So, in the case of absence these correlations it means there are different reasons and justifications must catch. In addition to studying these correlations in different sectors of public shareholding companies (industrial, services, financial sectors), in order to determine the difference between them, which help different interested parties (such as investors, analysts. Managements, creditors.), take their rational decisions.

1.2. Objective of the Study

The objective of this study is to look at the nature of the correlation between company returns (return on assets and earnings per share), book value and market value per share. Also to analyze the nature of the correlation between market value and book value per share in different sectors belonging to the industrial, services, and financial segments in Jordanian shareholding companies during the period between (2008-2014).

1.3. Research Hypotheses

The construction of the study’s hypotheses is based on intellect and accounting logic which stipulates that the increase in a company's ability to exploit its assets and achieve high rate of return on its investment will lead to an increase in the company's ability to capture profits. This will reflect positively on book value per share as well as increase the company's ability to achieve profit which will increase earnings per share, and this in turn will attract investors and motivate them to keep and buy the company's shares. Ultimately, all these will reflect positively on the market value of the stock. In general, the increase in book value per share is an indication of the strength and durability of the financial position of the company, and this is supposed to reflect positively on the market value of the company’s shares. Thus, this study aimed to test the following assumptions:

(i). There is no significant correlation between return on assets and the market value per share.

(ii). There is no significant correlation between return on assets and the book value per share.

(iii). There is no significant correlation between earnings per share and the market value per share.

(iv). There is no significant correlation between earnings per share and book value per share.

(v). There is no significant correlation between the book value and market value per share.

1.4. Significance of the Study

The importance of this study is related to the extent and nature of the relationship between the earnings realized by the shareholding companies such as return on assets, which is one of the important indicators for measuring a company's performance, and the earnings per share, which is one of the principal interests of investors in order to judge the returns stocks and make decisions whether to keep these stocks or otherwise, and between market and book value and the response of these value returns to the earnings generated by the shareholding companies. In addition, analyzing and ascertaining the relationship between market and book value of the shares, in which it is assumed that there is a direct and positive relationship between them is also important. Thus, the contribution of this study relies on reflecting the ability of Jordanian companies to show financial status and the efficiency of their information and their earnings in enhancing the value of their shares, and providing conclusions and recommendations that will help in enhancing the market and book value of shares, and therefore the companies’ overall value, which would help them to survive and compete at the local and global level.

2. Theoretical Framework & Literature Review

There are many factors that affect the turnout of the shareholders in retaining their shares of companies such as dividends so that the investors will obtain income from these dividend distributions periodically and continuously, especially if the company is pursuing a fairly stable dividend policy. In addition, the investors may seek to obtain capital gains from these shares through speculative operations or they try to significantly affect the company's decisions and thus influence the decision and direction of the company's management and vote of the board members [1].

This research focuses on share valuations which are linked to corporate performance and its ability to achieve income, especially since the evaluation of the shares is an important investment tool that affects the investors' decisions. There are several values of shares, including the par value of shares, the issued price of the company’s shares at the beginning of the foundation of the company, defined on the face of a share certificate and is the basis of the company’s recorded capital in its books. [13], determines the par value of the shares of Jordanian companies to be JD 1 only.

Book value per share varies depending on the company's earnings and its ability to construct retained earnings, it is the value that the stockholder is expected to obtain in the event that the company is liquidated. It is calculated by dividing the shareholders' equity over the number of shares issued and traded [2].

A reliable way of assessing the value of a company is through the present value of its shares, while the discounted generated cash flows from the operations of the company based on an appropriate discount rate reflect the degree of risk faced by the company, and the rate of return required by the administration of the company. Nevertheless, many difficulties are associated with determining the expected cash flows, the appropriate discount rate and the period for the discount, especially in the case of shares, which has infinite life within going concern assumption [19].

In the view of [11], the market value of shares is the fair value or focal value per share and the value that investors want to pay to own the stock, which depends on what information the investors have. In the case of non-availability of information to all investors at the same time, it will lead to a disparity and lack of agreement among the investors on the share price, and the new information coming in the market leads to obvious changes in this price.

[14], mentioned that the market value of a share is affected by the book value of the shares, as rising book value is an indication of the company's ability to achieve income and maintain them as returned earnings; thus, having a positive impact on the stock price in the market. In addition, the dividends resulting from the incomes generated by the company as a result of activity and success in their work is expected to positively affect the market value of the shares as well as investors' expectations about the strength and durability of the financial position of the company which would lead to positive effect on the market value of the shares, especially in the case of optimistic expectations.

[19], explained that the market value is affected by environmental, logistical and political circumstances surrounding the company. The growth of recovery and economic prosperity in the economy has a positive effect on the market value of the shares, in addition to what is published in terms of domestic or international political news, and as expected from conditions of war or peace which would suggest trouble or stability and thus significantly and clearly affecting stock prices in the financial market.

The market value is assumed to affect by returns generated by the companies; a study by [4], showed that there is no significant correlation between return on equity and the ratio of market value to book value per share. Additionally, the study also indicated lack of significant correlation between return on equity and market value per share of Jordanian companies. [21], in his study revealed that there is a direct correlation between the dividends per share and retained earnings per share with the market value of the Jordanian commercial banks’ shares, and that the dividends per share have more effect in influencing the market value of the Jordanian commercial banks’ shares, compared with retained earnings per share. Results from a study by [18], showed that the announcement of earnings per share and dividends affect the determination of the market value and the amounts of stocks traded on the Palestinian stock exchange market. Additionally, the earnings per share have more effect on the market value of the shares, compared with the effect of the dividends.

In another study which was carried out by [16], the results obtained showed that there is a positive effect of retained earnings on the book value of Jordanian commercial banks’ shares, and there is a positive effect of the book value on the market value of shares and thus on the capital gains realized by investors from trading these shares.

Results from a study by [5], showed there is a positive and strong correlation between the market value per share and companies' income and dividends in the stock exchange market of the United Kingdom. [5], found that the correlation of dividends is stronger than the companies' income, where the change in the dividends is substantially affected by the change in the companies' income.

[3], in his study examined the effect of different financial ratios on the market value per share of the Palestinian stock exchange market for various segments of companies. The study found that it can rely on a set of financial ratios for each of the companies’ sectors to predict the market value per share, and the relationship between these financial ratios varied depending on the sector in which the company belongs. The study found that insurance companies showed strong correlation between the market value per share and market value to book value ratio, and earnings per share and book value per share. As for investment companies, there is strong correlation between the market value per share and return on equity, and book value per share and current ratio.

The study by [22], examined the correlation between the accounting disclosures, earnings per share, book value per share and the market value per share on the Taiwan stock exchange market. The study found significantly strong correlation between the accounting disclosure, earnings per share, book value per share and market value per share.

[8], in their study aimed to test the effect of the announcement of the income and the dividend on the market value per share and the volume of shares trading in Greece’s stock exchange market. The study reached the conclusion that the positive correlation between the market value per share and volume of shares trading was due to the announcement of income and dividend. [6], carried out a study on a sample of companies in Ghana's stock exchange market and concluded that the announcements of the dividend significantly affect the market value per share, especially if the stock exchange market is effective.

In their study [17], aimed to examine the correlation between the market ratios and the market value per share in Tehran’s Stock Exchange market. They found that there is statistically significant correlation between earnings per share, and dividends per share and the market value per share.

[20], in their study looked at the key factors that determine the market value per share in the Emirates’ stock exchange market. Their study revealed strong correlation between earnings per share and the market value per share.

[12], in their study tested the correlation between dividends and earnings per share and the change in market value per share in the British stock exchange market. Their study revealed that there is positive correlation between earnings per share and dividends and the change in the market value per share. They concluded that earnings per share and dividends are considered to be the main factors in determining the market value per share in the British stock exchange market.

[23], in their study tested the effect of the announcement of dividends before and after the 10 days of the loss of the right to receive dividends on the market value per share in Taiwan’s stock exchange market. The study found a significant increase in the market value per share during the 10 days preceding the date of the loss of the right to receive dividends, compared with the 10 days following the date of the loss of the right to receive dividends.

3. Research Methodology

This section presents an analytical description of the methodology of the study and reviews the stages and steps followed to test the study’s hypotheses. This section begins with the description of the study population and sample, resources for collecting data, and the statistical methods used in analyzing the data.

3.1. Population and Study Sample

The study was carried on a population consisting of companies included in the Amman Stock Exchange securities. The researcher collected the necessary data from the Jordanian guide of public shareholding companies issued by securities commission board Commission Securities Exchange [7]. The Jordanian companies were chosen randomly from different sectors using unrestricted or simple random sampling method, where the companies’ financial reporting fulfilled the conditions for selection of the sample, and have all the required data for the period from 2008 to 2014. Information on companies in the study population and sampling are showed in Table (1).

Table 1. Study population and sample.

Source: prepared by researcher.

3.2. Statistical Method

To test the study's data and hypotheses, the Statistical Program for Social Sciences (SPSS) IBM version 19 was used. Pearson correlation was used to test the hypotheses of the study, where it is a measure of the most prevalent mechanism for measuring a linear correlation between two variables and the correlation coefficient ranges between (-1, +1). The value of the correlation coefficient indicates the strength of the correlation, while the sign clarifies the direction of the correlation. Therefore, as the correlation coefficient gets closer to (+1), the correlation is considered strong and positive. However, if the correlation is strong and negative, then the Pearson correlation coefficient gets closer to (-1), while a correlation coefficient that is closer to (0) is an indicator that the correlation is weak. In this study, the researcher considered (50%) as the mid-point of the correlation; thus, if the correlation coefficient is more than (50%) at the significance level of (a ≤ 0.05) at 95% confidence level, this indicator shows that the correlation is higher than the mid-point, and vice versa if the correlation coefficient is lower than 50%. The researcher would then accept the affirmative hypothesis if the significance value of the Pearson correlation coefficient is ≤ 5% at 95% confidence level, which means there is correlation between the variables of the study. In contrast, a null hypothesis is accepted if the significance value of the Pearson correlation coefficient is > 5%. Next, the researcher would examine the linear correlation between the variables of the study by testing the dissemination schedule of the data (scatter plot) which would show if the correlation between the study variables has linear correlation. This would allow the researcher to rely on Pearson correlation coefficient to test the hypotheses of the study. To test the normality distribution of the data, the study depends on the central limit theorem which states that cases of normal distribution of the data, the sample should be more than 30 items [9]. Since the study samples involved 1162 items, this indicated that the data distribution followed the normal distribution.

3.3. Measurement & Descriptive Statistics of Study Variables

The variables measured in this study are shown in Table (2) below.

Table 2. Summary of study variables and its measurement.

* There isn't any preferred stocks issued by Jordanian insurance companies

Source: prepared by researcher

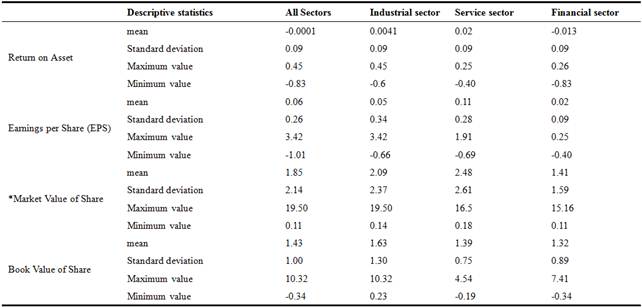

The descriptive statistics of the study’s variables are shown below:

Table 3. Descriptive statistics for the study’s variables.

* Par value to common stock issued by Jordanian companies 1 JD.

Source: prepared by researcher (Statistical tests)

4. Statistical Results

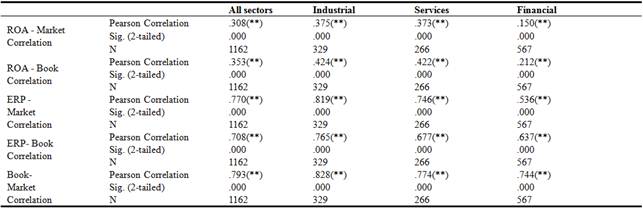

This section represents the statistical results related to Pearson correlation tests of the study’s hypotheses. It begins with the summary of the analytical results of the correlation tests between the study variables of the Jordanian companies for the year 2008 to 2014 as shown in Table (4).

Table 4. Pearson Correlation for All Sectors and the Industrial, Service, and Financial Sectors Individually.

** Correlation is significant at the 0.01 level (2-tailed).

* Correlation is significant at the 0.05 level (2-tailed).

prepared by researcher (Statistical tests)

Table (4) shows a statistically significant correlation amounting to 30.8% between return on assets and market value per share at the significance level of (a≤0.05), indicating a positive correlation less than the mid-point in all sectors of the Jordanian companies. Table (3) shows the convergence value of the coefficient correlation between return on assets and market value per share in the industrial and service sectors, where the correlation coefficient for both sectors was 37.5% and 42.4% respectively, at the significance level of (a≤0.05). Meanwhile, the correlation coefficient between the return on assets and market value per share in the financial sector was 15% at the significance level of (a≤0.05), which is an indication that the market value of shares is linked to a variety of factors and variables; some of them are linked to market factors, while others are linked to economic factors and other different factors.

Thus, the null hypothesis is rejected and the affirmative hypothesis accepted; there is significant correlation between return on assets and the market value per share at the significance level (a≤0.05).

Referring to Table (4), it shows that the Pearson correlation coefficient between return on assets and book value per share amounted to 35.5%. This indicates that there is a positive correlation less than the mid-point at the significance level of (a≤0.05) for the Jordanian companies, and reference to Table (3) shows that the correlation in the industrial and service sectors was 42.4% and 42.2% respectively, while the correlation coefficient in the financial sector, reaching 21.2% at the significance level of (a ≤ 0.05).

Based on the above result, the null hypothesis is rejected and the affirmative hypothesis accepted; there is a significant correlation between return on assets and book value per share at the significance level of (a≤0.05).

Table (4) shows that there is a positive and higher than the mid-point correlation between earnings per share and market value per share, as the correlation coefficient was 77% at the significance level of (a≤0.05) for all the sectors of the Jordanian companies. Additionally, the correlation coefficient between earnings per share and market value per share was 81.9% for the industrial sector and 74.6% for the service sector, while the positive correlation coefficient for the financial sector was 53.6% at the significance level of (a≤0.05). These results confirm that correlation between earnings per share and market value per share was higher than the correlation between return on assets and market value per share, an indication that the earnings per share is closer to market value per share than return on assets in all sectors of the Jordanian companies.

Thus, the null hypothesis is rejected and the affirmative hypothesis accepted; there is a significant correlation between earnings per share and market value per share at the significance level of (a≤0.05).

Table (4) shows that there is a positive and higher than the mid-point correlation between earnings per share and book value per share for all sectors of the Jordanian companies as the value of the correlation coefficient was 70.8% at the significance level of (a≤0.05). In addition, the industrial sector showed higher and positive correlation than the mid-point, where the correlation coefficient reached 76.5%, whiles the correlation coefficient was 67.7% and 63.7% for both the service sector and financial sector, respectively. This result confirms the higher correlation between earnings per share and book values per share for all sectors of the Jordanian companies.

Thus, the null hypothesis is rejected and the affirmative hypothesis accepted; there is a significant correlation between earnings per share and book value per share at the significance level (a≤0.05).

Referring to Table (4), a clear and more than the mid-point correlation can be seen between book and market value per share for the Jordanian companies, reaching a correlation coefficient of 79.3% at the significance level of (a≤0.05). A correlation coefficient of 82.8% at the significance level of (a≤ 0.05) was found in the industrial sector, while the correlation coefficient between the book value and market value in the service sector and financial sector reached 77.4% and 74.4% respectively, at the significance level of (a≤ 0.05). This result confirms the high correlation between book value and market value for all the sectors of the Jordanian companies.

Therefore, the null hypothesis is rejected and the affirmative hypothesis accepted; there is a significant correlation between book value per share and market value per share at the significance level of (a≤0.05).

5. Conclusion and Recommendations

The study found several results, and these are highlighted below.

(i). Higher correlation between earnings per share and market value and book value per share, compared with the correlation between return on assets and market value and book value per share.

(ii). Higher correlation between returns (return on asset and earnings per share) and market and book value per share in the industrial and service sector compared with the financial sector.

(iii). Converged correlation between returns (return on asset and earnings per share) and market and book value per share in both the industrial and service sector, while the correlation for the financial sector differed. This may be due to the high volume of assets in the financial sector compared with the industrial and service sector, especially intangible assets among the total assets.

(iiii). There is positive and high correlation above the mid-point between book value and market value in all sectors of Jordanian companies. This indicates that the change in book value per share leads to a change in market value per share, and vice versa. Thus, the change in such value can be relied upon as an indicator of the change in other values.

The researcher would therefore recommend that investors increase their interest in the changes of book value per share, which in turn is expected to lead to a change in market value and thus on their ability to obtain capital earnings from trading shares. This would reflect the efficiency and affluence of the stock exchange market which plays a critical role in the development and evolution of the economy at the local and international level.

All parties in stock exchange market such as investors, researchers and official bodies must increase their attention to the factors that affect the market value per share of the financial sector, as it was found that the correlation between market value per share with earnings (return on assets and earnings per share) in this sector was less than the other sectors.

Finally, the researcher would like to recommend future researchers to carry out studies that look into building or developing a model that would allow prediction of market value per share by relying on book value and return on asset and earnings per share in all sectors as the results of the present study showed correlation between these variables.

References

- Abu-alrub, N., &Thaher, M. (2006). The impact of the dividend on share price and trading volume of listed companies in the Palestine stock exchange securities, Journal of Al-Quds Open University for Research and Studies, 1(8), 251-272.

- Abu-Nassar, M. (2014).Accounting companies scientific and practical issues. (4th ed), Dar Wael for Publishing, Jordan, Amman.

- Algergawi, K. (2008). The role of financial analysis of published financial information in financial statements to predict stock prices. unpublished Master Thesis, Islamic University of Gaza.

- Al-Rai, Z. (2001). The impact of the accounting rates of return on equity and market valuation of common stocks of Jordanian Companies. Journal of Business and Management, 5(3), 464-477.

- Anupam, M. (2012).An empirical analysis of determinants of dividend policy -evidence from the UAE companies.Global Review of Accounting and Finance, 3(1), 18-31.

- Asamoah, G., &Nkurmah, K.(2010). The impact of dividend announcement on share price behavior in Ghana.Journal of Business & Economics Research, 8(4), 47-58.

- Commission Securities Exchange. Available online at: http://www.jsc.gov.jo.

- Dasilas, A., Lyroudi, K., &Ginoglou, D. (2008).Joint effects of interim dividend and earnings announcements in Greece. Studies in Economics and Finance, 25(4), 212-232.

- Gujrati, D.N.(2004). Basic Econometrics. (4th ed), New York: McGraw Hill.

- Hamdan, M. (2012).The effect of the accounting conservatism in improving earnings quality of financial reporting: A Case Study of Jordanian industrial companies. Al Drasat Administrative Sciences, 38(2),33-55.

- Hinawi, M. (2000).Analysis and assessment of stocks and bonds. Al Dar Algamaih Publishing, Jordan, Amman,

- Hussainey, K., Mgbame, C. O., &Chijoke-Mgbame, A. M. (2011). Dividend policy and share price volatility: UK evidence. The Journal of Risk Finance, 12, (2), 57-68.

- Jordanian Companies Law No. (22). 1997. As amended. Available online at: http://www.ccd.gov.jo.

- Khalaf, F. H. (2006). The financial and cash markets. The Modern World of Books for Publication Distribution, Irbid, Jordan.

- Kieso, D. W., & Warfield, T. (2014). Intermediate accounting.15th edition, Wiley & Sons, New Jersey.

- Kilani, Q., &Kaddoumi, T. (2006). The impact of the returns earnings on the book and market value and capital gains for shares listed on the Amman Stock Exchange Securities. Jordan Journal of Applied Sciences, 9 (1), 20-41.

- Saeidi, P., & Khandoozi, B. (2011).The investigation of relation between market ratios and market price per share of accepted companies in Tehran stock exchange. Global Business and Management Research: An International Journal, 3(2), 136-140.

- Sharb, O. (2006). The effect of the announcement of the dividend on the shares price of listed companies in Palestine Stock Exchange Securities: an empirical study. Unpublished Master Thesis, Islamic University of Gaza.

- Subramanyam., K.R., (2015), Financial Statement Analysis, 11th edition, McGraw-Hill Inc, New York.

- Tamimi, H. A., Alwan, A. A., & Abdel Rahman, A. A. (2011).Factors affecting stock prices in the UAE financial markets. Journal of Transnational Management, 16(1), 3-19.

- Thaher, M. (2003). Dividend policy and its impact on the market price of the stock traded on the Amman Stock Exchange Securities. The Journal of Bethlehem University, 1(22), 28-61.

- Wang, H. C., & Chang, H. (2008). The association between accounting information disclosure and stock price. Global Journal of Business Research, 2(2), 1-10.

- Yang, J. J., & Wu, T. H. (2015). Announcement effect of cash dividend changes around Ex-dividend days: evidence from Taiwan. The International Journal of Business and Finance Research, 9(2), 77.