International Journal of Economics and Business Administration, Vol. 1, No. 1, July 2015 Publish Date: Jun. 17, 2015 Pages: 25-38

Defining Balanced Scorecard Aspects in Banking Industry Using FAHP Approach

Malihe Rostami*, Ahmad Goudarzi, Mahdi Madanchi Zaj

Department of finance and accounting, Electronic Branch, Islamic Azad University, Tehran, Iran

Abstract

This study has been conducted to define Balanced Scorecard model as one of evaluation system in bank. Financial institutions and banks are trying to increase their competitive advantage, so find a comprehensive evaluation model for the performance that is a main key to survive and get competitive position. There are several theories and methods of assessment that can be employed depending on the size and type of organization. Balanced Scorecard (BSC) is one of the measurement systems that cover short and long term plans and strategies and also, internal as well as external control. BSC consider aspects of the financial, customer, internal processes and learning and growth. In this article, aspects of Balanced Scorecard and the importance of each aspect and related indicators are examined. To achieve the research objective Fuzzy Analytical Hierarchy Process (FAHP) is used. At the first step of study, 56 indicators were found based on prior studies and literature which were scrutinized by expert opinions through administering a questionnaire. Ultimately 9 indicators were extracted. In the second step of study, the weight of each indicator is investigated using pair comparison questionnaire based on FAHP approach. According to research, the first priority is customer aspect, the second priority is the financial aspect, third priority is internal processes aspect and the end, learning and growth aspect are the fourth priority. Meanwhile, the "Market rate" and the "Growth rate of customer complaints" and "Customer attract rate" are the most important indicators of customer aspect. "Revenues", "P/E ratio" and "leverage" are the most important indicators in the financial aspects, the "Electronic transactions share", "Performance management" and "Research and development costs" are the most important indicators in internal processes aspect and "Employee stability", "Loan per capita" and "Present reduction in disciplinary matters" are the most important indicators in growing and learning aspect.

Keywords

Received:April 25, 2015

Accepted: May 18, 2015

Published online: June 18, 2015

@ 2015 The Authors. Published by American Institute of Science. This Open Access article is under the CC BY-NC license. http://creativecommons.org/licenses/by-nc/4.0/

Contents

1. Introduction 2. Problem Statement 3. Performance Evaluation 4. Balance Score Card (BSC) 5. BSC Background 6. BSC Perspectives 6.1. Financial Perspective 6.2. Customer Perspective 6.3. Internal Business Perspective 6.4. Learning and Growth Perspective 7. BSC Advantages 8. BSC Literature 9. Fuzzy Analytic Hierarchy Process (FAHP) 10. Chang Triangular Method 11. The Triangular Fuzzy Numbers 12. Fuzzy Delphi Method 13. Consistency Rate (CR) 14. Research Methodology 15. The Research Model 16. Discussion and Results 16.1. Priority Determination of Indicators 16.2. The Final Priority Determination with AHP Technique 17. Summary and Conclusions

1. Introduction

In today's competitive world, only organizations can compete and to make the profit those can attend to the needs of our customers and try to provide customer satisfaction and loyalty [1]. Banks are also included in this rule. In other words, banks, like other organizations, to evaluate the performance of their activities and to assess the achievement of strategic objectives [2]

Since the competitive distance is reduced in organizations, they are looking to increase their competitive advantage and one of the ways to gain a competitive advantage, is to evaluate the performance of the organization and find the appropriate ways [3]

Performance analysis and evaluation of banks and financial institutions require a specific framework. Meanwhile, we can design and build a system or set it as a tool to analyze the performance of the Bank's strategy is one of the fundamental requirements [4].

There are different methods to analyze organization performance such as "Ratio Analysis", "Delphi Analysis", Balanced Score Card" ,"Data Envelopment Analysis", "Analytic Hierarchical Process", "Total Production Analysis" and " Regression Analysis" that an organization can chose according to its type and size [5]. It means, an organization needs to find an effective way to join performance to goals [4].

Since the banks are as an intermediary between the owners and users of financial resources, they can create money, so any mistakes or failures in performance result impacts on the economic situation negatively. Hence, focus on finding the right method and system performance evaluation improve banking system and economic [2].

Existence of accurate, comprehensive and reliable performance management is one of the indicators of development agencies and banks that require relevant infrastructure and requirements.

Balanced Scorecard is a tool that can cover this need. In this article, the aspects of the balanced scorecard with fuzzy analytic hierarchy process method (FAHP) are examined.

2. Problem Statement

The financial institutions are a tool to make growth on country’s economic development. In developing countries, due to the lack of development of financial markets, the institutions are not efficient. So, in competitive environment, economic institutions need to improve themselves continuously [6].

In the current financial environment, the processes of integration and rapid technological changes that have taken place, ensuring the accuracy of the organization’s performance is important that it’s necessary to be considered many aspects and environmental conditions [2].

Performance evaluation points to an organization's goals in a special period and it is one of the most important activity of control management that checks whether resources are being used correctly and efficiently and whether it is achieving its objectives in the short term, the organization will help achieve long-term plans and strategies [5], [7].

Due to the financial aspects and non-financial organizations can help to achieve the goal in competitive environment because according to traditional view and calculation of financial ratios are not sufficient to explain internal and external environment of an organization, the ratio of ROA and ROE and the others cannot be shown shareholders' welfare [4], [8].

Balanced Scorecard is a tool for evaluating the performance that also, points to non-financial aspects, aspects of the customer, internal processes and learning and growth and this tool has attracted banks and financial organization’s attention [6].

This study aimed to find the most effective aspects of the balanced scorecard and indicators for banks and certainly, the results of this research will help banks to revise map strategies and plans to make more successfulness.

3. Performance Evaluation

Performance evaluation is usually synonym with effectiveness of the organization's activity [9]. Overall, performance evaluation refers to specified assessment process in unique term that all expectations and indicators are clear before. It is one of effective way to improve one organization. So, managers try to find suitable route to evaluate performance [10].

These days, the issues raised in the most recent scientific field are directly or indirectly related to performance evaluation. The reason is that each of the concepts, techniques, and practices of organizations in order to achieve better performance. So, the main focus of the evaluation is to evaluate the utility of these functions and all managerial issues will be directly or indirectly related to performance evaluation.

4. Balance Score Card (BSC)

One of the most famous and best-known models in performance evaluation system model is "Balanced scorecard" that is developed by Kaplan and Norton in 1992 and then expanded and improved. In addition, BSC consider the non-financial indicators plus financial as a prerequisite for future financial performance and drive them completed and assist organizations in implementing strategies.

Balanced Scorecard is a strategic management system that helps organizations to identify strategies and make it executable [11], [12].

Balanced Scorecard is a tool used by many organizations used to evaluate the performance of different aspects. The model is not only to consider the organization performance internally, but many investors and shareholders, are able to monitor the results of this organization, assess and ensure [8].

This model suggests to evaluate the performance of each organization must use the set of indicators. So that managers can monitor four major aspects of the organization:

So these four aspects are:

• Financial aspects

• Customer aspects

• Internal business aspects

• Learning and growth aspects [13].

• Each of these aspects into one of the following four basic questions answered:

• How do we look to shareholders? (Financial aspect

• How do customers see us? (Customer aspect)

• What must we excel at? (Internal business aspect)

• Can we continue to improve and create value? (Learning and growth aspect) [14].

Kaplan and Norton believe that knowing about these aspects, disappears problems increase and accumulation of information by restricting the use of the indicator. The managers will be forced to focus only on a limited number of indicators are crucial and critical. In addition, the use of several different aspects of performance prevents from focus on one subject only [15].

Balanced Scorecard objectives come from organization's vision and strategy. With the old view, which was the only financial perspective, there are many differences and the difference in the balanced scorecard after some changes is focus on the learning and growth of the business and its customers and environment. It also contains to recognize the strengths and weaknesses of your competitors and focus on improving the quality of these [10]. Balanced scorecard as a tool to help manage and evaluate organizational performance effectively [11], [16].

Balanced Scorecard can take several forms, including options and various operational parameters to be useful in decision-making and also, ways and forms of implementation and use of the balanced scorecard can have different effects on performance [11].

5. BSC Background

BSC was devised and designed by Robert Kaplan of Harvard University and David Norton David Norton, who was working as a consultant in the Boston area in 1992, [15]. Kaplan and Norton were as a consultant for12 companies in 1990. They seek new ways to measure the performance of their companies. They believed that they could not calculate only financial items to evaluate the performance of businesses. These companies were convinced that reliable measure of financial performance is not enough and affected by their ability to create value. Management believes these companies focus on issues relating to customers, internal processes, and commercial matters relating to staff and stakeholders can effectively contribute to the assessment of organizational performance. Kaplan and Norton's called this tool to "Balanced Scorecard" [1], [13].

After four years, a number of organizations with the implementation of the Balanced Scorecard achieved satisfactory results. Kaplan and Norton found that these organizations are not only non-financial factors as well as financial agents had placed but their strategy is also linked through measures that had been chosen. Thus, in 1996, Kaplan and Norton wrote a book that is named balanced scorecard and is explained BSC as a tool to implement organizational strategies and performance. Since the completion of the balanced scorecard in four generations and improved, many public and private companies try to follow this model to evaluate the performance [4], [11].

6. BSC Perspectives

Balanced Scorecard considers an organization in four perspectives [6], [13], [17], [18], [19], [20], [21]. They are explained as follows:

6.1. Financial Perspective

Financial aspects, because of direct relevance to the demands of all groups such as owners, shareholders, government and others have been the focus of management and control activities. Financial aspects can be used as a basis for the process of the customer and the employee's perspective is considered. In fact, this view is the starting point for identification purposes other financial aspects (Customer side, processes and aspects of learning) and ultimately, the success of other aspects of the financial aspects of the measure. Each of the measured parameters is part of the chain of cause and effect which should find its place in accordance with the financial objectives and also estimates a part of strategic objectives.

6.2. Customer Perspective

Customer satisfaction is the main theme of most systems, because these systems are put customers at the beginning and end of the process. On the one hand, the systematic identification of customer needs is an absolute imperative; on the other hand, customer satisfaction variable in this model is emphasized responsibility and accountability’s senior management.

Thus, using the following parameters is defined according to criteria relating to the customer's perspective is necessary:

• Customer

• Marketing

• Identify customer requirements

• Customer satisfaction

6.3. Internal Business Perspective

Organizations often for controlling their process improvement focus on processes within the organization but for comprehensive process control, according to the whole evaluation process, according to the views and the views and needs of our customers and owners of the process is necessary. Assessment process with clear communication of customer survey process is closely related to quality management systems [17]

Thus, using the following parameters is defined according to the sub-indices of all processes is essential:

• Focus on customer needs

• Production lead time based on customer needs

• Guided costs to customer needs

6.4. Learning and Growth Perspective

How to set ambitious objectives in terms of fulfill the customer’s internal processes and ultimately shareholder?

The answer to this question lies in the objectives and measures of learning are growth perspective. In fact, the objectives and measures enabling the objectives set out in the other three perspectives are [17]

7. BSC Advantages

Using the Balanced Scorecard framework provides organization can implement its strategy and the implementation of its results. Also, this card provides a framework for evaluating specifies objectives and programs and strategies. Finally, it’s a way to measure and ensure the functional status of the present head [3]

Some merits and benefits of the Balanced Scorecard are [1], [10]:

• Welcomed to BSC by various organizations around the world,

• A comprehensive and systematic approach to the performance,

• Successful link to the reward and encourage system,

• Logic modeling,

• Enabling business processes to ensure the health of the organization,

• Leadership and guidance of the continuous improvement program,

• Enabling the external benchmarking processes,

• Good experiences in order to develop a list of business planning and evaluation is used,

• Reliance on soft measures, the recent addition of a hard and long and short term,

• Leading the desire for professional use in various businesses

• Focus on the concepts of total quality management,

And also, it can be mentioned that the main advantages of using the balanced scorecard (BSC) are:

• The integration and oversight,

• Concentration,

• Timeliness,

• Alignment,

• Accountability,

• Participation,

• Transformation,

• Evolution

8. BSC Literature

In table 1 some prior studies are discussed in Balanced score card area.

Table 1. Prior studies in Balanced score card area

| Author | Year | Subject | Result |

| Alidade, B., & Ghasemi, M.[22] | 2015 | Ranking the Branches of Bank Sepah of Sistan Baluchistan Using Balanced Score Card and Fuzzy Multi-Attribute Decision Making Methods | In this study, the method of fuzzy AHP and fuzzy TOPSIS are used to evaluate the Balanced Scorecard. Meanwhile, the Kolmogorov-Smirnov test was used to check the normality of variables. |

| Noori, B.[23] | 2015 | Prioritizing strategic business units in the face of innovation performance: Combining fuzzy AHP and BSC | In this research SBUS or the Balanced Scorecard Strategic Business Units is used to consider and prioritize its strategic business units. Fuzzy AHP technique has also been used. |

| Feizi, A., & Solukdar, A.[1] | 2014 | Combined with a balanced scorecard approach to performance assessment of the banking industry - with Fuzzy TOPSIS method | In this study, the performance of the banking industry with a balanced scorecard approach combines techniques TOSIS and Fuzzy AHP is analyzed. A total of 24 indicators in the balanced scorecard model is applied. |

| Hoque, Z. [17] | 2014 | 20 years of studies on the balanced scorecard: Trends, accomplishments, gaps and opportunities for future research | In this study, 20 years of research on the balanced scorecard is discussed. |

| Mandic, K., Delibasic, B., Knezevic, S., & Benkovic, S. [7] | 2014 | Analysis of the financial parameters of Serbian banks through the application of the fuzzy AHP and TOPSIS methods | Balanced scorecard indicators in Serbian banks with FAHP and TOPSIS technique have been studied. |

| Zhang, Q., Wu, C., & Guo, W. [24] | 2014 | Performance evaluation of bank microfinance based on fuzzy mathematics and AHP. In Fuzzy Systems and Knowledge Discovery (FSKD) | In this study, have been selected the performance indicators and balanced scorecard approach with FSKD in China's commercial banks for analysis. Research has shown that lack development agencies and banks is due to the lack of information. |

| Ghasemi, A., & Ahmadi, S.H. [10] | 2013 | Evaluation of higher education institutions with the help of a balanced scorecard and multi-criteria decision methods | In this research, higher education institutions, universities with the help of a balanced scorecard and multi-criteria decision methods have been evaluated and ranked. |

| AkkoÇ, S., & Vatansever, K. [28] | 2013 | Fuzzy performance evaluation with AHP and Topsis methods: evidence from turkish banking sector after the global financial crisis | Balanced Scorecard indicators are discussed with FAHP and TOPSIS technique, in 12 Turkish banks after the financial crisis. In other words, the bank's performance evaluation is conducted by the BSC. |

| Dincer, H., & Hacioglu, U. [34] | 2013 | Performance evaluation with fuzzy VIKOR and AHP method based on customer satisfaction in Turkish banking sector | In this study, BSC model of Turkish banks with VIKOR and fuzzy AHP technique is analyzed. |

| Jafari-Eskandari, M., Roudabr, N., & Kamfiroozi, M. H. [25] | 2013 | Banks' Performance Evaluation Model Based on The Balanced Score Card Approach, Fuzzy DEMATEL and Analytic Network Process | In this study, key performance indicators (KPI) with regard to the balanced scorecard and ANP fuzzy DEMATEL techniques have been studied. These indicators are the basis for evaluating the performance of organizations. |

| Jiang, L., & Liu, H. [4] | 2013 | A multi-criteria group decision making model for performance evaluation of commercial banks. In Fuzzy Systems and Knowledge Discovery (FSKD) | In this study, the commercial banks to determine indicators in the balanced scorecard and performance evaluation model FUZZY Systems and Knowledge Discovery FSKD or in other words, have been studied. |

| Sedaghat, M., & Sari, I. [26] | 2013 | A productivity improvement evaluation model by integrating AHP, TOPSIS and VIKOR methods under Fuzzy environment. | In this study, the method of fuzzy AHP and TOPSIS and VIKOR to evaluate the Balanced Scorecard is used. Performance evaluation is carried out in three Iranian banks. |

| Shivakumar, U., Ravi, V., & Venkateswaran, T. R. [27] | 2013 | Quantification of Balanced Scorecard Using Crisp and Fuzzy Multi Attribute Decision Making: Application to Banking. In Emerging Trends in Engineering and Technology (ICETET) | In this study, the methodology CRISP AND FUZZY Multi Attribute Decision Making and balanced scorecard are used to assess in Indian banks and ICETET. The study ranked banks. |

9. Fuzzy Analytic Hierarchy Process (FAHP)

There are several methods of analytic hierarchy process, although the experts use of their intellectual competence and ability to perform comparisons, but it should be noted that traditional analytic hierarchy process, does not fully reflect the style of human thinking. Use of fuzzy numbers is compatible with human’s "verbal expressions" and "ambiguous", so it is better that using fuzzy numbers to make decisions in the real world. To implement the fuzzy analytic hierarchy process, there are several ways [28],[29],[30],[1].

Fuzzy theory to deal with the phenomena of the real world where there is uncertainty about that and many of the categories, the number of situations in the real world can be explained by fuzzy logic. Fuzzy AHP is determined by paired comparison matrices [28], [31].

10. Chang Triangular Method

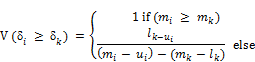

One method of fuzzy AHP method is Chang that the used numbers are in the triangular fuzzy. Chang for generalizing AHP technique is used the concept of Degree of Possibility. Degree of Possibility is to determine how likely a fuzzy number is larger than the other. In Chang triangular method, first select the desired phase spectrum and the data collected will be entered in a paired comparison matrix [2], [7], [32], [33], [34].

Each element of the matrix is shown with ![]() and calculation the sum of the preferences of each element is performed as follows.

and calculation the sum of the preferences of each element is performed as follows.

![]()

After is used linear normalize method and the fuzzy sum from elements preferences total can be calculated

For normalization, the sum of the preferences of each element must be divided by the sum of all preferences. Since the values are fuzzy, so overall preferences of each element multiplied by the inverse of the sum of preferences that can be calculated as follows:

![]() =

= ![]() × 1/[

× 1/[![]() ]

]

Then, the probability degree of each ![]() than the other values is calculated. The probability degree

than the other values is calculated. The probability degree ![]() to

to ![]() can be calculated as follows:

can be calculated as follows:

Final weight of each element is feasibility degree of element that is shown with ![]() .

.

![]() = (

= (![]() (

(![]() ), …,

), …,![]() (

(![]() ))

))

11. The Triangular Fuzzy Numbers

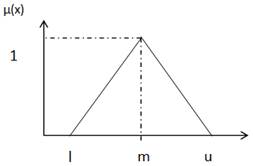

Triangular Fuzzy Number, TFN, is a fuzzy number can be three real number that is shown with F = (l, m, u).

Upper bound z is given by the maximum values that can adopt fuzzy number F.

Lower bound l is given by the minimum amount that can be held by a fuzzy number F.

M is the most probable value of a fuzzy number F.

Figure 1. The Triangular Fuzzy Numbers.

The triangular fuzzy numbers F = (l, m, u) in the geometric space as shown in figure 1. [2], [7], [33]:

12. Fuzzy Delphi Method

To determine the importance of criteria and indicators can be used Fuzzy Delphi technique. This technique is performed in the following way:

• Identify the appropriate range for the phase of verbal expressions

• Fuzzy values and fuzzy aggregation

• DE fuzzy values

• Prioritization criteria [33]

In Fuzzy Delphi Technique to prioritize the implementation, the first phase should be appropriate to the phase spectrum of verbal expressions of the respondents such as tables 2. [3], [7], [33]:

Table 2. The triangular fuzzy numbers of 5.

| Very important | important | Medium | no less important | very insignificant |

| (0.75,1,1) | (0.5,0.75,1) | (0.25,0.5,0.75) | (0,0.25,0.5) | (0,0,0.25) |

After selecting or developing appropriate fuzzy set, fuzzy expert opinion collected and recorded. The second step should be paid to the integration of expert opinion. If any expert opinion as triangular fuzzy numbers (l, m, u) display, a conventional method for aggregating expert opinions is as follow:

![]() = (min {l}, {

= (min {l}, {![]() }, max {u})

}, max {u})

13. Consistency Rate (CR)

Inconsistency rate indicates how much data can be gathered from the perspective of a trusted expert. According to preliminary calculations, the analytic hierarchy process based on judgment decisions based on a comparison of paired elements. So any errors and inconsistency in the elements can affect, the final result obtained from the calculations [33].

Consistency index is calculated as follows:

WSV (Weighted Sum Vector) = [M] × [W]

Approximate value of λmax is:

L = ![]() [

[![]() ]

]

CI = ![]()

CR = ![]()

14. Research Methodology

The first step of this study starts with identification of influential indicators. To this aim a questionnaire is developed based on five-point Likert scale including 56 indicators which were chosen according to prior studies. After administering questionnaires, the data were analyzed using SPSS software, Freidman ranking test were employed which lead to 9 affecting indicators ultimately.

Because usually the elements of each aspect are composed of the following criteria, the number of comparisons can be very frustrating. For this reason, Tomas L. Saaty believes 7 - 9 elements per aspect are most efficient [33].

In this step, 24 questionnaires from BSC team experts in one Iranian bank are entered into analysis.

The next step is to determine weights and priorities of indicators using second questionnaire which is developed based on a matrix of paired comparisons and seven-point L-Saaty scale for FAHP method.

In this step, 175 responses gathered through 300 administered questionnaires which were used for the analysis.

15. The Research Model

In this study, initial balanced scorecard model according to table 3, is examined with 56 indicators in each aspect. And after analyze and software results, 9 indicators in each aspect are chosen and are ranked.

Table 3. BSC model in study after data analyze.

| Financial aspects | → | Assets |

| → | ROE | |

| → | Leverage | |

| → | Spread rate | |

| → | Revenues | |

| → | Loan | |

| → | Deposits | |

| → | NPL | |

| → | P/E | |

| Customer aspect | → | Customer satisfaction |

| → | Loyalty | |

| → | Market rate | |

| → | Customer attract rate | |

| → | Growth rate of customer complaints | |

| → | Availability | |

| → | Long term deposit | |

| → | Validity and reliability | |

| → | Update services | |

| Internal business aspect | → | Number of new services and products |

| → | Management performance | |

| → | Research and development costs | |

| → | Trying to create a new branch | |

| → | Number of issued cards | |

| → | Number of improvement projects | |

| → | Share of consolidated revenue | |

| → | Electronic transactions share | |

| → | Macro and associated facilities | |

| Learning and growth aspect | → | Knowledge management |

| → | Training | |

| → | Employee stability | |

| → | Education | |

| → | Experience | |

| → | Job satisfaction | |

| → | Present reduction in disciplinary matters | |

| → | Deposits per capita | |

| → | Loan per capita |

16. Discussion and Results

In this research we have tried aspects of Balanced Scorecard and the importance of each aspect and related indicators are examined in the bank.

To achieve the purpose of research, library method for obtaining information and experiences and field studies to obtain more information to help experts Balanced Scorecard Fuzzy Analytic Hierarchy Process (FAHP) is used.

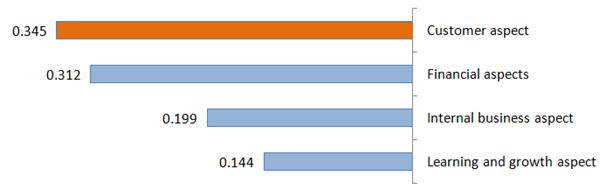

In table 4 and figure 2, normal weights defuzzification of main aspects is shown. The center of gravity (COG) is used for defuzzification, same as follow:

![]()

![]()

![]()

Crisp number = Z* = max {![]() }

}

Table 4. Normal weights defuzzification of main aspects.

| Aspects | X1max | X2max | X3max | Deffuzy | Normal |

| Customer aspect | 0.355 | 0.353 | 0.351 | 0.355 | 0.345 |

| Financial aspects | 0.322 | 0.319 | 0.317 | 0.322 | 0.312 |

| Internal business aspect | 0.205 | 0.203 | 0.202 | 0.205 | 0.199 |

| Learning and growth aspect | 0.149 | 0.147 | 0.146 | 0.149 | 0.144 |

Figure 2. Main aspects priority.

The results show that the highest priority is the "Customer aspect" with normal weight 0.345

The second priority is the "Financial aspect" with normal weight 0.312

And then third priority, "Internal processes aspect" with normal weight 0.199

And the end, lowest priority, "Learning and growth aspect" with normal weight 0.144

Also obtained consistency rate is about 0.054 which is smaller than 1.0.

16.1. Priority Determination of Indicators

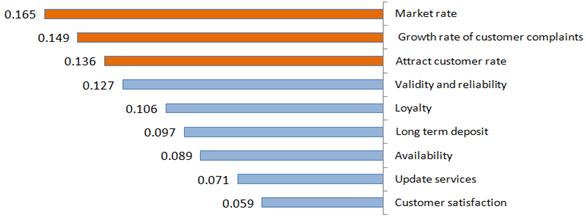

Customer indicators are Market rate, Growth rate of customer complaints, Attract customer rate, Validity and reliability, Loyalty, Long term deposit, Availability, Update services, Customer satisfaction.

The results show that the first priority is the "Market rate" with normal weight 0.165, the second priority is the "Growth rate of customer complaints" with normal weight 0.149, and then third priority, "Attract customer rate" with normal weight 0.136 , also obtained consistency rate is about 0.031 which is smaller than 1.0.

In table 5, normal weights defuzzification of customer aspect is shown and also with figure 3, priority of customer indicators is discussed.

Table 5. Normal weights defuzzification of customer aspect.

| Customer Indicator | X1max | X2max | X3max | Deffuzy | Normal |

| Market rate | 0.174 | 0.173 | 0.172 | 0.174 | 0.165 |

| Growth rate of customer complaints | 0.157 | 0.157 | 0.156 | 0.157 | 0.149 |

| Attract customer rate | 0.143 | 0.143 | 0.142 | 0.143 | 0.136 |

| Validity and reliability | 0.133 | 0.133 | 0.132 | 0.133 | 0.127 |

| Loyalty | 0.112 | 0.111 | 0.111 | 0.112 | 0.106 |

| Long term deposit | 0.102 | 0.102 | 0.101 | 0.102 | 0.097 |

| Availability | 0.094 | 0.093 | 0.092 | 0.094 | 0.089 |

| Update services | 0.075 | 0.074 | 0.074 | 0.075 | 0.071 |

| Customer satisfaction | 0.062 | 0.062 | 0.061 | 0.062 | 0.059 |

Figure 3. Customer indicators priority.

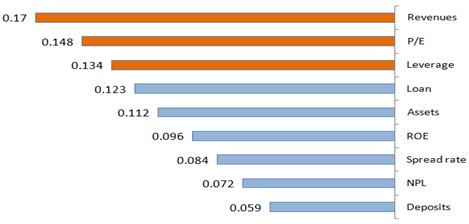

Financial indicators are Revenues, P/E, Leverage, Loan, Assets, ROE, Spread rate, NPL, Deposits.

The results show that the first priority is the "Revenues" with normal weight 0.170, the second priority is the "P/E" with normal weight 0.148, and then third priority, "Leverage" with normal weight 0.136, also obtained consistency rate is about 0.025 which is smaller than 1.0.

In table 6, normal weights defuzzification of financial aspect is shown and also with figure 4, priority of financial indicators is discussed.

Table 6. Normal weights defuzzification of financial aspect.

| Financial Indicator | X1max | X2max | X3max | Deffuzy | Normal |

| Revenues | 0.18 | 0.18 | 0.179 | 0.18 | 0.17 |

| P/E | 0.157 | 0.157 | 0.156 | 0.157 | 0.148 |

| Leverage | 0.142 | 0.141 | 0.141 | 0.142 | 0.134 |

| Loan | 0.13 | 0.13 | 0.129 | 0.13 | 0.123 |

| Assets | 0.119 | 0.118 | 0.117 | 0.119 | 0.112 |

| ROE | 0.102 | 0.101 | 0.101 | 0.102 | 0.096 |

| Spread rate | 0.089 | 0.089 | 0.088 | 0.089 | 0.084 |

| NPL | 0.077 | 0.076 | 0.075 | 0.077 | 0.072 |

| Deposits | 0.063 | 0.063 | 0.062 | 0.063 | 0.059 |

Figure 4. Financial indicators priority.

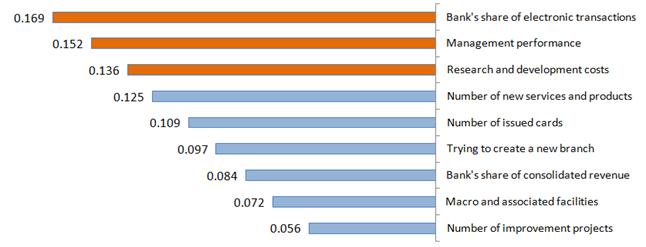

Internal business indicators are Share of electronic transactions, Management performance, Research and development costs, Number of new services and products, Number of issued cards, Trying to create a new branch, Bank's share of consolidated revenue, Macro and associated facilities, Number of improvement projects. The results show that the first priority is the "Share of electronic transactions" with normal weight 0.169, the second priority is the "Management performance" with normal weight 0.152, and then third priority, "Research and development costs" with normal weight 0.136, also obtained consistency rate is about 0.031 which is smaller than 1.0.

In table 7, normal weights defuzzification of internal business aspect is shown and also with figure 5, priority of internal business indicators is discussed.

Table 7. Normal weights defuzzification of internal business aspect.

| Internal business Indicator | X1max | X2max | X3max | Deffuzy | Normal |

| Bank's share of electronic transactions | 0.18 | 0.18 | 0.179 | 0.18 | 0.169 |

| Management performance | 0.162 | 0.162 | 0.161 | 0.162 | 0.152 |

| Research and development costs | 0.145 | 0.145 | 0.144 | 0.145 | 0.136 |

| Number of new services and products | 0.133 | 0.133 | 0.132 | 0.133 | 0.125 |

| Number of issued cards | 0.116 | 0.115 | 0.115 | 0.116 | 0.109 |

| Trying to create a new branch | 0.104 | 0.103 | 0.103 | 0.104 | 0.097 |

| Bank's share of consolidated revenue | 0.089 | 0.089 | 0.088 | 0.089 | 0.084 |

| Macro and associated facilities | 0.077 | 0.076 | 0.075 | 0.077 | 0.072 |

| Number of improvement projects | 0.06 | 0.06 | 0.059 | 0.06 | 0.056 |

Figure 5. Internal business indicators priority.

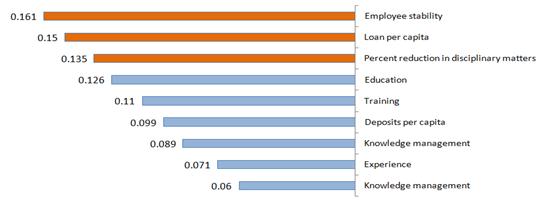

Learning and growth indicators are Employee stability, Loan per capita, Present reduction in disciplinary matters, Education, Training, Deposits per capita, Knowledge management, Experience, Knowledge management.

The results show that the first priority is the "Employee stability" with normal weight 0.161, the second priority is the "Loan per capita" with normal weight 0.150, and then third priority, "Present reduction in disciplinary matters" with normal weight 0.135, also obtained consistency rate is about 0.033 which is smaller than 1.0.

In table 8, normal weights defuzzification of learning and growth aspect is shown and also with figure 6, priority of learning and growth indicators is discussed.

Table 8. Normal weights defuzzification learning and growth aspect.

| Learning and growth Indicator | X1max | X2max | X3max | Deffuzy | Normal |

| Employee stability | 0.171 | 0.17 | 0.169 | 0.171 | 0.161 |

| Loan per capita | 0.158 | 0.158 | 0.157 | 0.158 | 0.15 |

| Present reduction in disciplinary matters | 0.142 | 0.142 | 0.141 | 0.142 | 0.135 |

| Education | 0.133 | 0.132 | 0.132 | 0.133 | 0.126 |

| Training | 0.117 | 0.116 | 0.115 | 0.117 | 0.11 |

| Deposits per capita | 0.104 | 0.104 | 0.103 | 0.104 | 0.099 |

| Knowledge management | 0.094 | 0.094 | 0.093 | 0.094 | 0.089 |

| Experience | 0.075 | 0.074 | 0.073 | 0.075 | 0.071 |

| Knowledge management | 0.063 | 0.063 | 0.062 | 0.063 | 0.06 |

Figure 6. Learning and growth indicators priority.

16.2. The Final Priority Determination with AHP Technique

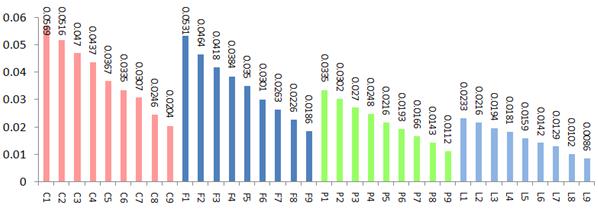

To determine the ultimate priority with using AHP technique should be multiply the main criteria weights (W1) and weights on each criterion (W2). The calculation of final priority determination is shown in table 9.

Table 9. Final priority determination with AHP technique.

| Aspects | Weight | Indicators | Symbol | Weight | Final weight |

| Customer aspects | 0.345 | Market rate | C1 | 0.165 | 0.0569 |

| Growth rate of customer complaints | C2 | 0.149 | 0.0516 | ||

| Attract customer rate | C3 | 0.136 | 0.047 | ||

| Validity and reliability | C4 | 0.127 | 0.0437 | ||

| Loyalty | C5 | 0.106 | 0.0367 | ||

| Long term deposit | C6 | 0.097 | 0.0335 | ||

| Availability | C7 | 0.089 | 0.0307 | ||

| Update services | C8 | 0.071 | 0.0246 | ||

| Customer satisfaction | C9 | 0.059 | 0.0204 | ||

| Financial aspect | 0.312 | Revenues | F1 | 0.17 | 0.0531 |

| P/E | F2 | 0.148 | 0.0464 | ||

| Leverage | F3 | 0.134 | 0.0418 | ||

| Loan | F4 | 0.123 | 0.0384 | ||

| Assets | F5 | 0.112 | 0.035 | ||

| ROE | F6 | 0.096 | 0.0301 | ||

| Spread rate | F7 | 0.084 | 0.0263 | ||

| NPL | F8 | 0.072 | 0.0226 | ||

| Deposits | F9 | 0.059 | 0.0186 | ||

| Internal business aspect | 0.199 | Bank's share of electronic transactions | P1 | 0.169 | 0.0335 |

| Management performance | P2 | 0.152 | 0.0302 | ||

| Research and development costs | P3 | 0.136 | 0.027 | ||

| Number of new services and products | P4 | 0.125 | 0.0248 | ||

| Number of issued cards | P5 | 0.109 | 0.0216 | ||

| Trying to create a new branch | P6 | 0.097 | 0.0193 | ||

| Bank's share of consolidated revenue | P7 | 0.084 | 0.0166 | ||

| Macro and associated facilities | P8 | 0.072 | 0.0143 | ||

| Number of improvement projects | P9 | 0.056 | 0.0112 | ||

| Internal learning and growth aspect | 0.144 | Employee stability | L1 | 0.161 | 0.0233 |

| Loan per capita | L2 | 0.15 | 0.0216 | ||

| Present reduction in disciplinary matters | L3 | 0.135 | 0.0194 | ||

| Education | L4 | 0.126 | 0.0181 | ||

| Training | L5 | 0.11 | 0.0159 | ||

| Deposits per capita | L6 | 0.099 | 0.0142 | ||

| Knowledge management | L7 | 0.089 | 0.0129 | ||

| Experience | L8 | 0.071 | 0.0102 | ||

| Knowledge management | L9 | 0.06 | 0.0086 |

Figure 7. Final priority determination with AHP approach.

Thus, according to the calculations, the total weight of each index is calculated using fuzzy AHP model technique.

17. Summary and Conclusions

In today's world economic literature, the role and importance of the financial system, money and capital market and consequently financial institutions as executive arms of government and economic development tool is quite tangible so that sustainable economic development is not possible without the development of financial markets. The financial and credit organizations have played a pivotal role in this regard [1], [12].

Today, most organizations have realized that to survive and maintain its position and gain more benefits, they should always have performance improvements that will be resolved by setting goals and planning [6]

Banks and financial institutions are at the macro level of economy and the activity will impact directly on economic data. So, the banks are looking for a tool to improve their performance [31].

In this research, balanced scorecard model is chosen to rank four aspects of model in bank. The results of article are proved Customer aspect as first cluster and financial aspect for second, Internal processes aspect for third and the end Learning and growth aspect for forth.

Also, in each aspect, 9 indicators are chosen and after are discussed and ranked with FAHP technique.

According to results, in customer aspect, Market rate with 0.0569, Growth rate of customer complaints with 0.0516 and Attract customer rate with 0.047 weights are the most effective indicators in BSC model.

In financial aspect, Revenues with 0.0531, P/E with 0.0464 and Leverage with 0.0418 weights are the most effective indicators in BSC model.

In internal business aspect, Bank's share of electronic transactions with 0.0335, Management performance with 0.0302 and Research and development costs with 0.0270 weights are the most effective indicators in BSC model.

And also, in internal learning and growth aspect, Employee stability with 0.0233, Loan per capita with 0.0216 and Present reduction in disciplinary matters with 0.0194 weights are the most effective indicators in BSC model.

This is clear, in each kind of country and organization, the results and conclusion are different and are depends on technological, environmental, social and economic criteria.

References

- Feizi, A., & Solukdar, A. (2014), Combined with a balanced scorecard approach to performance assessment of the banking industry - with Fuzzy TOPSIS method, Engineering and management of securities, 20, 57-78

- Seçme, N. Y., Bayrakdaroğlu, A., & Kahraman, C. (2009). Fuzzy performance evaluation in Turkish banking sector using analytic hierarchy process and TOPSIS. Expert Systems with Applications, 36(9), 11699-11709.

- Wu, H. Y., Tzeng, G. H., & Chen, Y. H. (2009). A fuzzy MCDM approach for evaluating banking performance based on Balanced Scorecard. Expert Systems with Applications, 36(6), 10135-10147.

- Jiang, L., & Liu, H. (2013). A multi-criteria group decision making model for performance evaluation of commercial banks. In Fuzzy Systems and Knowledge Discovery (FSKD), 2013 10th International Conference on (pp. 940-945). IEEE.

- Wu, H. Y. (2012). Constructing a strategy map for banking institutions with key performance indicators of the balanced scorecard. Evaluation and Program Planning, 35(3), 303-320.

- Tabari, M., & Araste, F. (2008), The balanced scorecard approach to performance evaluation, Management journal, 5(12), 12-20

- Mandic, K., Delibasic, B., Knezevic, S., & Benkovic, S. (2014). Analysis of the financial parameters of Serbian banks through the application of the fuzzy AHP and TOPSIS methods. Economic Modelling, 43, 30-37.

- Wu, H. Y., Tzeng, G. H., & Chen, Y. H. (2009). A fuzzy MCDM approach for evaluating banking performance based on Balanced Scorecard. Expert Systems with Applications, 36(6), 10135-10147.

- Yalcin, N., Bayrakdaroglu, A., & Kahraman, C. (2012). Application of fuzzy multi-criteria decision making methods for financial performance evaluation of Turkish manufacturing industries. Expert Systems with Applications, 39(1), 350-364.

- Ghasemi, A., & Ahmadi, S.H. (2013), Evaluation of higher education institutions with the help of a balanced scorecard and multi-criteria decision methods, Journal of Medical Education, 6,10, 38-49

- Braam, G. J., & Nijssen, E. J. (2004). Performance effects of using the balanced scorecard: a note on the Dutch experience. Long range planning, 37(4), 335-349.

- Chen, T. Y., Chen, C. B., & Peng, S. Y. (2008). Firm operation performance analysis using data envelopment analysis and balanced scorecard: A case study of a credit cooperative bank. International Journal of Productivity and Performance Management, 57(7), 523-539.

- Kaplan, Robert S; Norton, D. P.(1996) ."Translating Strategy Into action The balanced scorecard" Harvard Business School Press.

- Keyt, J. C. (2001). Beyond strategic control: Applying the balanced scorecard to a religious organization. Journal of Nonprofit & Public Sector Marketing, 8(4), 91-102.

- Kaplan, Robert S; Norton, D. P. (1992). "The Balanced Scorecard-Measures That Drive Performance". Harvard Business Review (January–February), pp.71-79.

- Bentes, A. V., Carneiro, J., da Silva, J. F., & Kimura, H. (2012). Multidimensional assessment of organizational performance: Integrating BSC and AHP. Journal of business research, 65(12), 1790-1799.

- Hoque, Z. (2014). 20 years of studies on the balanced scorecard: Trends, accomplishments, gaps and opportunities for future research. The British accounting review, 46(1), 33-59.

- Park, J. A., & Gagnon, G. B. (2006). A causal relationship between the balanced scorecard perspectives. Journal of Human Resources in Hospitality & Tourism, 5(2), 91-116.

- Sundin, H., Granlund, M., & Brown, D. A. (2010). Balancing multiple competing objectives with a balanced scorecard. European Accounting Review, 19(2), 203-246.

- Anand, M., Sahay, B. S., & Saha, S. (2005). Balanced scorecard in Indian companies. Vikalpa, 30(2), 11-25.

- Ardabili, F. S. (2011). New Framework for Modeling Performance Evaluation for Bank Staff Departments. Australian Journal of Basic and Applied Sciences, 5(10), 1037-1043.

- Alidade, B., & Ghasemi, M. (1393), Ranking the Branches of Bank Sepah of Sistan Baluchistan Using Balanced Score Card and Fuzzy Multi-Attribute Decision Making Methods. Research Journal of Recent Sciences ISSN, 2277, 2502. vol. 4(1), 17-24

- Noori, B. (2015). Prioritizing strategic business units in the face of innovation performance: Combining fuzzy AHP and BSC. International Journal of Business and Management, 3(y: 2015: i: 1: p: 36-56), 36-56.

- Zhang, Q., Wu, C., & Guo, W. (2014, August). Performance evaluation of bank microfinance based on fuzzy mathematics and AHP. In Fuzzy Systems and Knowledge Discovery (FSKD), 2014 11th International Conference on (pp. 153-158). IEEE.

- Jafari-Eskandari, M., Roudabr, N., & Kamfiroozi, M. H. (2013). Banks' Performance Evaluation Model Based on The Balanced Score Card Approach, Fuzzy DEMATEL and Analytic Network Process. International Journal of Information, Security and Systems Management, 2(2), 191-200.

- Sedaghat, M., & Sari, I. (2013). A productivity improvement evaluation model by integrating AHP, TOPSIS and VIKOR methods under Fuzzy environment. Economic Computation and Economic Cybernetics Studies and Research, 47(1), 235-258.

- Shivakumar, U., Ravi, V., & Venkateswaran, T. R. (2013, December). Quantification of Balanced Scorecard Using Crisp and Fuzzy Multi Attribute Decision Making: Application to Banking. In Emerging Trends in Engineering and Technology (ICETET), 2013 6th International Conference on (pp. 164-170). IEEE.

- AkkoÇ, S., & Vatansever, K. (2013). Fuzzy performance evaluation with AHP and Topsis methods: evidence from turkish banking sector after the global financial crisis. Eurasian Journal of Business and Economics, 6(11), 53-74.

- Arman, M., & Salehi S.J., & Mojdehi, S., & Nazarali, A, (2012), The amount of inconsistency hierarchical structure and paired comparison matrices in the analytic hierarchy process and fuzzy, Journal of Industrial Management Studies, 10,27, 89-112

- Safaii GH. AB., & Aghajani, H., & Dargahi, H. (2012), Proposed approach combines the techniques of fuzzy multi-criteria decision to prioritize strategies to achieve world-class manufacturing, Journal of the Operational Research and Applications, 9,2(33), 81-99

- Najafi, E., & Aryanezhad, M. (2011). A BSC-DEA approach to measure the relative efficiency of service industry: A case study of banking sector. International Journal of Industrial Engineering Computations, 2(2), 273-282.

- Rahmani, K., Bohloli, N., Sadeghzade, B., (2012), Developed a mathematical model of fuzzy quality function deployment approach, beyond management, 5,20, 7-34

- Habibi, A., Izadyar, SH., Sarafrazi, A., (2014), Fuzzy multi-criteria decision, Katibe gil, 1, 0-72-5466-600-978

- Dincer, H., & Hacioglu, U. (2013). Performance evaluation with fuzzy VIKOR and AHP method based on customer satisfaction in Turkish banking sector. Kybernetes, 42(7), 1072-1085.