American Journal of Marketing Research, Vol. 2, No. 5, October 2016 Publish Date: Oct. 19, 2016 Pages: 114-126

Nature of Commercial Practices in the Namibian Pension Fund Administration Market

Manfred Rii Zamuee*

The Research Department, Maastricht School of Management, Maastricht, Netherlands

Abstract

Using a diagnostic and explanatory framework, this paper inquires into the market conduct and power dichotomy of the private pension fund administration industry in Namibia. Therefore, the purpose of the study is to appraise the core commercial practices of Namibian pension fund administrative firms to determine impact on anti-trust outcomes and consumer protection. Data was collected through intensive literature review and administration of questionnaires to trustees and principal officers of pension funds. The study outcome reveals that the dominant market structure in the Namibian pension fund administration industry is oligopolistic based on imperfect competition.

Keywords

Anti-trust Impact Test, Customers Impact Test, Pension Funds, Oligopoly, Cross Selling, Conditional Selling

Received: September 11, 2016

Accepted: September 29, 2016

Published online: October 19, 2016

@ 2016 The Authors. Published by American Institute of Science. This Open Access article is under the CC BY license. http://creativecommons.org/licenses/by/4.0/

Contents

1. Introduction 2. Research Problem 3. Objective of the Study 4. Research Propositions 5. Research Methodology 5.1. Introduction 5.2. Research Design and Data Collection 5.3. Theoretical Framework and Data Analysis 6. Analytical Foundation of the Study 7. Operationalization of the Study Framework 8. Literature Review 8.1. Background 8.2. Theoretical Foundations 9. Study Findings 9.1. Cross-Selling 9.2. Conditional Selling 9.3. Aggressive Commercial Tactics 10. Empirical Findings of Survey 11. Discussion of Study Results 11.1. Market Dominance 11.2. Market Structure 12. Discussion of Competitive Impact Tests 13. Conclusion Appendix 1. Research Conceptual Model

1. Introduction

Namibian financial services sector plays a very important role in the Namibian economy. Given the strategic importance of this sector various efforts were concerted towards localizing and integrating this sector into mainstream developmental opportunities.

The Namibian pension fund landscape resembles the globalised taxonomy or constellation of three pillars for pension schemes (World Bank, 1994), namely:

• first pillar of a universal non-means tested old age pension scheme administered by the State

• second pillar of occupational pension schemes administred by private administrive firms; and

• third pillar of voluntary pension saving schemes administred by private administrative firms and insurance companies.

Within the financial system, the occupational pension funds accounts for more than 65% of GDP and hence a vital catalyst for creating a perfect competitive environment. Pension fund investments have given impetus to the development of financial markets, stock broking and asset management industry in Namibia (Stock & Sherbourne, 2004). Pension funds are registered and operated under the Pension Funds Act 24 of 1956 with the primary objective of providing retirement benefits to members. Under this Act, pension funds are allowed to carry out pension fund business activities in order to achieve members’ retirement objectives. Therefore, in carrying out this business mandate pension funds receive, invest contributions and pay benefits to members when they fall due. It is this commercial nature of pension funds that invites treatment as an "undertaking" under the Competition Act.

However, most pension funds have outsourced this responsibility to third party administrators who proclaims expertise and capacity to carry out these functions. In this regard, the proposed Financial Institutions and Markets Bill (2014) require trustees "to ensure that the rules and operation and administration of the fund comply with this Act and other applicable laws". This is in line with the common law position on delegation of authority, which requires accountability for outsourced services. Therefore, it can be argued that it is part of trustee fiduciary duty to ensure that the fund and its members are protected against maladministration and uncompetitive behavior. Before 1981, most pension funds in Namibia where managed and controlled by employer groups and most of the administrative functions (including treasury, benefit payments, member record updates etc.) were outsourced to third party specialist administrators who in most cases doubled as advisors also. No regulatory rules were in place around this type of outsourcing and administrative firms exerted huge control and influence over pension funds and the industry in general. The rules of engagement were left to the laissez faire principles of free market profit maximization. Given this context, the pension fund administration environment was characterized by few strong firms that seek to maximize monopoly capital. These administrative firms have developed business models that may be potentially prejudicial to consumers (members of the funds and trustees) and bordering on anti-competitive behavior. Some of these practices include cross selling or bulking, vertical integration and conditional selling.

This has led to deleterious consequences for the pension fund industry and the emergence of oligopolistic tendencies, which threatens compliance with anti-competitive legislation and destroys customer value.

An analysis of the Namibian pension fund administration reveals market segmentation between private administrators of occupational pension schemes (made up of private and umbrella funds) and insurance-linked administrators (administering mainly umbrella and insured funds). Insured funds are those pension schemes administered by insurance companies whose investment mainly consist of policies of insurance.

The Namibian pension fund administration market is highly concentrated with three of the largest administrators controlling more than 80% of the private market. These administrative firms have leveraged on free market economic principles and engineered various esoteric financial instruments including the creation of commercial umbrella pension and preservation schemes. The lack of sophistication and resources on the side of the Regulator has always made it difficult for them to keep up with the proliferation of financial innovation on the side of service providers.

This analysis excludes the public sector since the Government Institutions Pension Fund (GIPF) is self-administered. However the GIPF employees pension fund and Members of Parliament and Political Office Bearers Pension fund are administered by GIPF’s wholly-owned subsidiary administration company called Kuleni Administrators.

2. Research Problem

Since Namibia’s independence on the 21st of March 1990, insurance companies and private administrators, consisting mainly of South Africa affiliated entities, controlled the pension fund administration market. Since then the market has seen few consolidations and acquisitions leading to the formation of few strong private pension fund administrators. The situation was worsened by lack of regulatory standards on pension fund administration creating a supply and demand dichotomy based on lack of objective business standards to ensure fair competition and consumer protection to members. This has led pension fund administrative firms to develop commercial practices aimed at profit maximization which collides which fair competition and customer value protection. This underscores the study problem.

3. Objective of the Study

Based on the study problem, the primary aim of the study is to investigate the nature of the Namibian pension fund administration market, with specific reference to the impact of commercial practices on fair competition and customer value creation. The study seek to appraise the nature of these commercial practices and synthesis with the overall purpose of a pension fund, which is to maximise retirement values for members in a fair and competitive administrative environment.

4. Research Propositions

The research proposition in qualitative studies refers to a conceptual assertion of a research phenomenon without adequate evidence to house a theory (Miles and Huberman, 1994). Therefore, the primary study proposition is that the current commercial practices of administrative firms in the Namibian pension fund market are not conducive to fair competition and customer value creation.

5. Research Methodology

5.1. Introduction

The analysis of business practices of pension fund administration firms in Namibia will be discussed with reference to a legal and economic perspective. The legal perspective will inquire whether these practices are ant-competitive whilst the economic perspective will look into potential consumer prejudice.

5.2. Research Design and Data Collection

According to Miles and Huberman (1994), qualitative research is based on collection of data in words for example observation, interview and documents in contextualized setting. The study will use secondary data collected from industry comparative literature, structured discussions with industry experts, NAMFISA annual reports, pension funds financial reports, newspaper articles, company reports and extracted information from the internet.

Doing qualitative analysis with the occasional aid of numbers is a good way of testing for possible bias and seeing how robust qualitative insights are (Salkind, 2012). Therefore, the study used a questionnaire survey approach to triangulate and validate the qualititave findings from observed data and comparative literature review. Although questionaires are usually used for quantitative studies (Saunders et al, 2007), it is also effective for descriptive qualititave studies (Robson, 2002). The questionnaires had a 5-point Likert scale with choices ranging from (1) Not very important, (2) Less Important, (3) Moderately important, (4) Important and (5) Very Important.

The study approach is hence based on mixed research methodology.

5.3. Theoretical Framework and Data Analysis

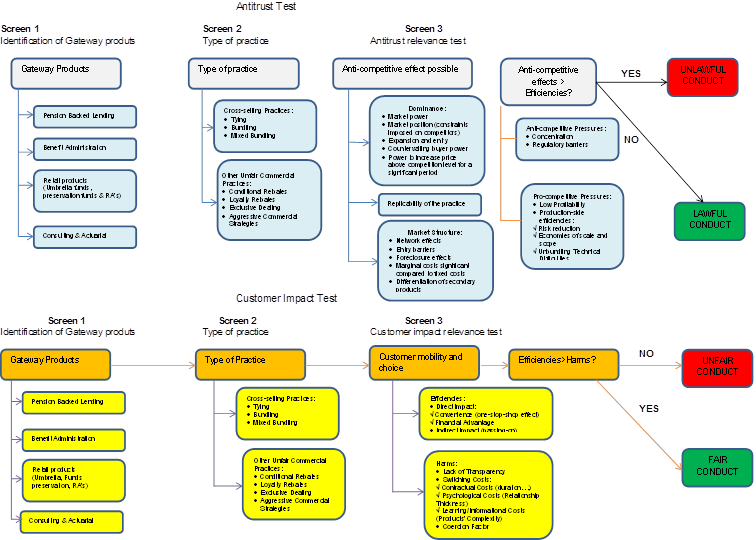

Using a diagnostic framework developed by the Centre for European Policy Studies (CEPS, 2009), that requires a legal and economic perspective to determine whether administrative practices are anti-competitive and unfair to consumers. In others words, two impacts tests will be conducted to measure anti-trust and customer impact of administrative practices by these firms. The anti-trust impact test is based on assessment of the legislative environment around anti-competition and specifically the Competition Commission Act. Customer impact test is based on elasticity of demand efficiencies derives from the current administrative environment.

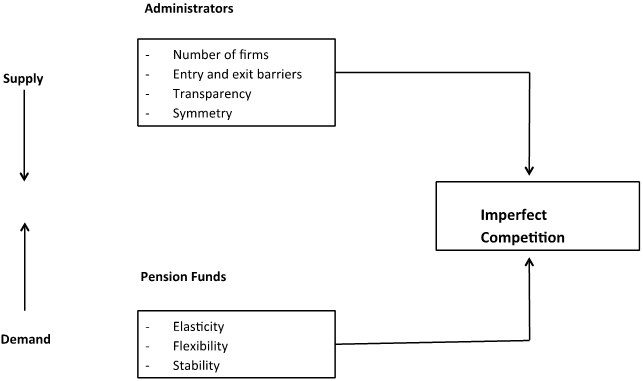

The anti-trust impacts test also uses the diagnostic framework of CPB Netherlands Bureau of Economic Policy Analysis (CPB, 2003) which is conceptually operationalized as follows in figure 1 below:

Figure 1. Research conceptual model.

Source: Authors own construct

Figure 1 above illustrates the study conceptualization of factors that describes anti-trust practices. The figure shows that the market has both a supply and demand side and elements of both dynamics determine whether the market is imperfect or not (CPB, 2003). The conceptual framework in figure 1 is based on a broader analytical framework in Appendix 1 hereto which seeks to create the foundation for determining the nature of market competititveness from a customer value and anti-trust perspective.

6. Analytical Foundation of the Study

Therefore, the analytical foundation in Appendix 1 looks at the following practices in an effort to fully operationalise the study conceptual framework:

• cross-selling (tying and service bundling)

• conditional selling

• aggressive commercial tactics (based on unsolicited offers, churning and steering)

Cross-selling is defined as the selling of two or more products in a package without any of these products sold separately although they can be sold separately. This is usually the case where administrators of pension funds offer additional services like consulting and actuarial services as part of a bundled offering to pension funds. Another aspect is where administrators in a bundled way offer one or two of these services free of charge as a condition for retaining the core administration function.

Conditional selling is defined as the delivery of service subject to a condition to consumers, for example that administration services will only be offered provided a pension fund accepts consulting or actuarial or both services as a condition of the agreement.

Aggressive commercial tactics are divided into three categories being:

• unsolicited offers (pressure selling or inertia selling where a product or service is offered without the consumer asking for it and there is some degree of pressure to buy.). In practice this could refer to so-called "value addition" products that are seamlessly sold to pension funds

• churning is where trust relationship between the administrator and pension fund is abused (data base exploited to give product advantage to administrator)

• steering is seen as the practice of some administrators who use carefully choreographed sale techniques to steer pension funds into a buying decisions.

7. Operationalization of the Study Framework

The observed practice in the Namibian pension fund administration market was analyzed using the study framework in figure 1 and Appendix 1 above, as follows:

When pension-backed lending is used as gateway product:

Anti-trust perspective, lack of transparency in the design and costing models of financial services products. The trend is for administrators to facilitate an agreement with the bank for secret profits or undisclosed kickbacks.

Customer perspective, the members of pension funds unfairly pay for these additional costs and in some cases on top of the standard housing loan administration fees already payable under the fund administration agreement.

When benefit administration is used as gateway product:

Anti-trust perspective, when administration costs are not activity or performance based and merely based on profit motive of the administrator.

Customer perspective, lack of effective service delivery leading to delayed payment of benefits. The lack of consumer powers (by members) over the administration of pension funds is another unfair aspect of benefit administration products.

When umbrella funds are used as gateway product:

Anti-trust perspective, administrators as founders of umbrella funds appoint trustees and principal officers (directly or indirectly). All services are bundled with one service provider for these funds. Exclusive service level agreements with administrator designed to keep competition away.

Customer perspective, the umbrella administration model is not necessarily cost-effective for pension funds or members. No real benefits of cross-subsidization filters down to members. Another unfair aspect of umbrella funds is that management committees have no real impact on decision-making on matters affecting their funds.

When consulting and actuarial services are used as gateway product:

Anti-trust perspective, independence of consultants and actuaries compromised by ties to administrator, directly or through associated firms.

Customer perspective, the biased advice given by tied actuaries and consultants is potentially unfair and not in the best interests of trustees or members.

8. Literature Review

8.1. Background

The Namibian pension fund administration landscape is highly concentrated with three administrative firms controlling over 80% of the market. According to the structure-conduct profitability model used to measure competitiveness in the banking industry, market concentration leads to an increase in anti-competitive behaviour including collusion (Carlton D. & Peltzman S., 2010). The Competition Commission Act 2 of 2003 creates the legal framework for consumer protection against uncompetitive market conduct like collusion and price fixing. The Act establishes the Competition Commission, which has powers to administer and enforce the Act in a co-ordinated manner. Therefore, any "undertakings" in Namibia are within the purview or captive net of the Namibian Competition Commission.

The Competition Commission Act defines "undertakings" as "any business carried on for gain or reward by an individual, a body corporate, an unincorporated body of persons or a trust in the production, supply or distribution of goods or the provision of any service."

For purposes of analysis the terms "business", "gain" and "reward" have a common denominator in that all refers to an activity that derives "commercial or material benefit or advantage" as held in the Namibian High Court case of Mitchel’s Plain Town Centre Merchants Association v. Mcleod and Another, 1996.

Section 1 of the Pension Funds Act 24 of 1956 states that a pension fund organisation is any association or "business" created for the purpose of providing annuities or lump sum payments for member and their beneficiaries. Reference to the word "business" implies some degree of commercialisation of the pension fund activity. Therefore, the business of pension funds is to provide retirement benefits to members by collecting and investing contributions based on an investment strategy. In other words, any activity of a pension fund that seeks to maximise rewards or return on investment (both interchangeably referring to gain from business activity) to fulfil its purpose may be regarded as a business for gain or reward. Therefore, to the extent that pension funds carry on any business for "gain" or "reward" they would be regarded as "undertakings" and subject to the jurisdiction of the Competition Commission.

Although pension fund administrators are not directly regulated under existing pension fund laws, as private companies they fall under the ambit of the Namibian Constitution, Companies Act, Financial Institutions (Investment of funds) Act and the Competition Commission Act. This creates legal and socio-economic framework for administrative firms to act in utmost good faith, observe administrative justice and protect pension fund member assets in their care without taking undue advantage.

Furthermore, the proposed Financial Institutions and Markets Bill of 2014 states that pension fund trustees have a duty to ensure that administrators of their pension funds comply with relevant laws.

The ordinary Oxford dictionary meaning of the word "ensure" is to "make certain that (something) will occur or be the case". This imposes an onerous duty on trustees to "regulate" the conduct and practices of administrators of their schemes. Therefore, the general conduct of pension fund administration firms is required to be consistent with fair competition and protection of customer interests (including members of pension funds).

Under the Namibian Constitution the State has a duty to "protect" citizens from infringement on their fundamental rights through passing relevant law and regulations. In Head of Department, Department of Education, Free State Province v Welkom High School and Another (2013) at par 84 it was held that ""the state must regulate private retirement provision to protect people against exploitation by private institutions and must, through such regulation, provide effective legal remedies where such exploitation or other forms of interference occur."

The normative theory of regulation requires pension fund regulators to encourage fair competition and regulate innovation in the interest of consumer protection (Botha & Makina, 2011). Therefore, NAMFISA has a statutory mandate to guarantee the enforcement of protection against market abuse by monopolistic or oligopolistic market tendencies and ensure that customer rights are protected.

Furthermore, in the South African Pension Fund Adjudicator case of Kamaldien v. Telkom Retirement Fund Sanlam Life Insurance Ltd PFA/WE/3009/01 it was held that trustees cannot abdicate their fiduciary duties in favour of administrative firms. Trustees must apply their independent minds to pension fund management issues and take informed decisions.

8.2. Theoretical Foundations

A literature overview on the subject matter reveals that the market structure of the Namibian pension fund industry resembles some degree of imperfect competition. Private pension fund administrators in Namibia is limited to few dominant firms and this market structure is common in pension fund administration markets in the developing world. In Latin America most of the countries like Chile, Uraguay, Brazil also have major challenges around competitive efficiency (OECD, 2008). This is mainly due to constraints like market concentration, entry barriers, lack of consumer power, product complexity, lack of transparency, switching costs and search costs, financial illiteracy and weak intermediaries (Bikker and Spierdijk, 2009).

According to economic theory (CPB, 2003), markets structure is seen in terms of perfect and imperfect competition. Perfect competition is where the market has the following main characteristics:

• all firms sell identical products and services

• consumers have perfect knowledge of industry

• no barrier to entry or exit

On the other extreme, imperfect competition is where the above-mentioned conditions do not prevail and the market is mainly made up of few dominant firms who are oligopolistic and controls almost every aspect of the market based on artificial barriers to entry for potential competitors. Oligopoly refers to a market characterized by few sellers of a product and super normal profits over prolonged periods, whilst monopoly implies product differentiation because of many sellers. Oligopolistic markets are reminiscent of exorbitant prices and output rigidity (Rosenberg & O’Halloran, 2014). Therefore, in understanding the market dynamics of the Namibian pension fund administration industry, it makes sense to critically review the costing models for administration services charged by administrative firms.

Administration costs for pension funds are generally excessive and usually around 1% to 2% of assets (SA Treasury, 2013). Although the theory of activity based costing is conceptually premised on performance management as a key determinant of costing (Turney, 2008), administrative firms in Namibia are not obliged to price on the basis of customer value creation.

This means that there is no objective criteria for charging pension fund administration feee and much is left to the laissez faire market principles. Therefore, administrative firms in Namibia can determine profit margins at will and push the pendulum in whichever convenient direction. This creates a breeding ground for predatory pricing creating super natural profits and incentives for administrative firm to consolidate market dominance at the expense of customers (Bikker & Dreu, 2007).

According to international practice, the relationship between cost and retirement benefits is linear such that a 2% charge equals to a drop of almost 40% in member’s fund credits (OECD, 2001). This arithmetic representation fairly represents reality in Namibia given the same levels of costing for administrative services.

Another aspect of market control is the ability of private firms to appoint trustees and principal officers of umbrella funds. Contrary to NAMFISA Circular PF 02/2004, some dominant administrative firms continues to unfluence the appointmnet of trustees and principal officers of pension funds. This is usually done through entrenched rights under the founding charters or rules of these umbrella funds. This is an obvious governance breach colliding with global standards of pension fund administration (OECD, 2009).

Although no regulatory guidelines exits around the registration and operation of administrative firms, the basic provisions of the Namibian Constitution protects members and pension funds against arbirtrary and unreasonable administrave action. In a free market economy, regulatory restraint is advised, but not at the expense of consumers (IOPS, 2011). Therefore, regulatory insouciance in dealing decisively with predatory administrative firms collides with principles of consumer protection and leads to weak regulation.

Economies of scale or scale economies are important for market dominance and usually mergers and take-overs are conducive to tight oligopoly (CPB, 2003). In Namibia, we have seen significant activities around consolidation of administrative firms through acquisitions and buy-outs which has materially entreched the dominance position of these firms.

Some of the gateway products (Rusconi, 2008) developed by administrative firms include the following:

• pension-backed lending (housing loans offered to members on commercially agreed terms between banks and administrative firms in terms of which secrets profits are payable for administration and intermediation services);

• umbrella funds (pension or provident funds created as multi-employer schemes for member pension savings);

• retail funds (created by administrative firms to capture exists from umbrella funds)

• consulting and actuarial services (bundled with administrative services in a multi-dimensional service delivery model that ensures control and sustainability).

Based on the above, the Namibian pension fund administration market is associated with cross selling, conditional selling and aggressive selling tactics used as an effective means to create and retain market control by administrative firms.

About 75% of private occupational pension funds interviewed have been with the same administrative firm for periods longer than 10 years and have not tested the market for competitive rates in that period. Those few pension funds that eventually go out on tender for services does it as a formality to comply with good governance tick-list rather than a strategic attempt to get competitive rates from the market. Furthermore, a critical review of the most recent tender documents of funds for administrative services requires the following criteria as part of the eligibility requirements:

• past experience measured by the number of years in operation (and not necessarily the personal experience of the promoters of the firm);

• current funds under management (measured by the number of funds under administration);

• capacity in terms of technology;

• number of employees and

• financial capability measured by balance sheet information

This proves that there is practically no opportunity for new entrants to enter the administration market given the artificial barriers created by the existing dominant firms.

9. Study Findings

Using the study framework discussed in figure 2 above, the result of our analysis reveals the following:

9.1. Cross-Selling

The study found that the practice of cross selling is widespread and entrenched in the Namibia pension fund administration industry. Service delivery is done on the basis of a vertically integrated business mode in terms of which the administrator, consultants, actuaries and in some cases, the investment manager is the same person. Therefore, no system of checks and balances exists within this bundled environment. Although there is departmental or functional separation, all the services are carried out through the corporate structure of the same firm. Given the relatively easy access to member data, administrative firms have used this to their commercial advantage and developed various add-on retail products to capture and retain members within the administrative loyalty system of the firm. Given the lack of regulatory involvement, administrative firms exclusively determines the nature and level of costs for administrative services to umbrella funds. This has led to enormous abuse of market positon and some administrative firms have entrenched unreasonaby high costs covering investment levies and ad hoc fees on top of the already exorbitant administrative and investment fees. Therefore, cross selling is seen as a leveraged market penetration, retention and cost manipulation strategy for administrative firms without any real demonstrable value for customers or members of these umbrella funds.

The impact of cross selling is discussed at two levels:

Anti-trust perspective, cross-selling leads to anti-competitive foreclosure (Whinston, 1990) since potential competitors do not have real access to umbrella schemes founded and managed exclusively by administrative firms (some of these umbrella schemes do not allow external consultants to advise participating funds). Services are bundled under the pretext of cost-efficiencies, but on critical review it appears that the only efficiencies are in the form of maximised profits interest for administrative firms. Bundling of services creates unfair economies of scale, which would deter potential rivals to enter the market due to the high cost of technology and other resources necessary to start and operate and administration business in Namibia. This has created enormous leveraged market power for these dominant administrative firms.

Customer perspective, the unfair advantage derives from the fact that members have no impact on decision-making since they are mostly not represented at board of trustee level. Decisions are around costs and benefit distributions are unilaterally and arbitrarily imposed on them. Therefore, customer mobility is restricted due to the bundled nature of services and inherent product tying. This negatively limits customer choice.

9.2. Conditional Selling

Some of the services and product offered by administrative firms have subtle conditions that force customers or pension funds to remain with the same firm if they were to enjoy the add-on benefits. An example of this would be the new generation life-stage products in terms of which members are forced to invest with associate firms.

Anti-trust perspective, Conditional selling is regarded as an undesirable practice under the Long-term Insurance Act, but not prohibited for pension fund administration. The most frequent form of conditional selling is the obligation to "take-it-all or nothing" approach of these multi-carrier types of umbrella schemes founded and managed by administrative firms.

Customer perspective, customers are not offered any choice with regards to participation conditions and product transparency and comparability.

9.3. Aggressive Commercial Tactics

Aggressive commercial tactics involve unsolicited offers, churning and steering. This trade practices are most frequent in one-stop shop service providers where the same person does advisory and administration services. Under these circumstances, administration firm develops products on the basis of "privileged" member data whilst the advisor sells the products through buying advice to the customer on an unsolicited basis. The irony is that based on industry observations most of these advisors or consultants are not adequately qualified to provide professional advice to funds. At the moment, there are no regulatory standards for financial advise or intermediation which further enhances market power of administrative firms.

Unsolicited offers is when the administrative firm exploits member information to offer add-on products that is offered to pension funds without any request.

Churning is the practice of power abuse or providing a dependency climate based on information asymmetry. This is an effective abuse of trust by administrative firms who use customer information to their commercial advantage by designing products and services which targets these customers. Administrative firms controls the knowledge economy and conducts trustee training sessions which seeks to enhance and perpetuate their business models at the expense of trustees and members of umbrella funds.

Steering is regarded as a means through which consumer decisions are seamlessly integrated into the administrator’s product structure. Given the unfair access to member data, administrative firms have developed seamless systems that steers or direct member choice into retail products that’s in sync with the firms commercial interests. An example is an exiting member from umbrella funds who defaults into preservation funds administered by the firm.

Aggressive commercial actvities also involves regulatory capture through unsolicited advice on interpretation of ambuiguities in legislation. This means that administrative firms use their market position to pre-empt regulatory outcomes by carefully orchestrating interpretation of existing laws as it applies to their commercial activities through submitting unsolicited legal opinions which favorably justifies their market dominance.

Anti-trust perspective, aggressive commercial selling distorts the market and has negative effect on competition. Potential competitors do not have the same access to member data and cannot offer the same or better solutions to customer needs. This practice enhances exclusivity and also heightens market power of administrative firm at the expense of potential market entrants.

Customer perspective, customers do not possess adequate information about gateway products and increase dependency on the technical advice of consultants who are tied to the administrative firm. In this regard, pension funds are steered towards cost-intensive products and services, which are not necessarily in their bet interests. Some administrative firms have created financial planning associate companies to streamlines advisory activities at member level during exits from pension funds. In this regard, information is shared within the inter-company structures and business leads distributed for selling retail products.

10. Empirical Findings of Survey

To validate and triangulate the comparative literature (Miles and Huberman, 2013), a questionaire survey sent to 158 respondents covering Principal Officers and the Trustees of registered pension funds with NAMFISA. The collected responses were 105 fully completed questionnaires covering a rate of response of 66%. This triangulation approach seeks to test plausibility, sturdiness and confirmability or validity of data (Leedy, 1997). Triangulation also moderates researcher bias or potential prejudice due to participation in the industry (Patton, 2002).

The survey was based on some of the main patterns and themes emerging from the qualitative data like the following:

• trustee information asymetry (training and skill levels)

• transparency

• trustees performance standards

• separation of services

• conflicts of interests

• process for appointment of service providers

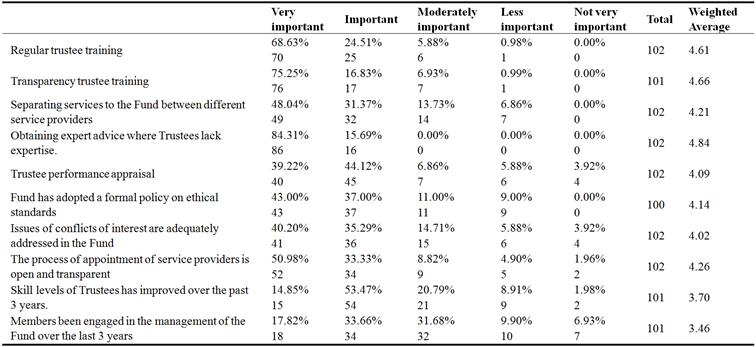

All the above themes are correlated to the major findings under the study conceptual framework and highlights some of the major determinants of anti-trust practices and desecration of customer values in the Namibian pension fund administration market.. Table 1 and figure 2 below illustrates a summary of the survey findings.

Table 1. Namibian Pension fund survey.

Source: Researcher’s own construct

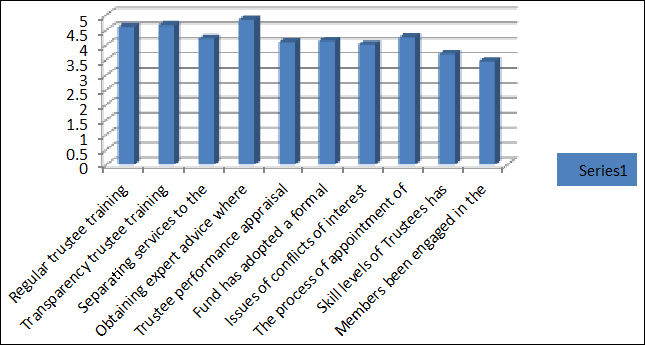

The average weighting under figure 2 below shows that expert dependency sydrome is very high in Namibia and that pension fund trustees have a serious shortage of skill. This also corroborates the earlier finding that administrative firms are capitalising on this gap by introducing complexy products that increases dependency on specialist skills.

Figure 2. Graphical representation of pension fund industry survey.

The results of the pension fund surveys portrays interesting similarities to the emprical literature findings. Based on the above illustration in Table 1 above, most of the trustees have indiacted the following issues as very important froma fund management point of view:

• the majority of trustees (about 70% of respondents) identified knowledge gap as a very important catalyst for effective functioning of pension funds. This is in line with the above findings under the study conceptual model which has highlighted information asymmetry as a major cause of anti-competitive behaviour leading to market abuse by administrative firms. In other words, more informed and empowered trustees of umbrella pension funds will be in a better position to enforce fair and perfect competitive practices in pension fund administration;

• whislt almost 80% of trustees opined that separation of services is eseential (very important and important) from a governance and efficiency point of view, the observed practice is revealing the contrary. Service bundling in the conetxt of the preaviling Namibia pension fund administration environment has a negative impact on governance, anti-trust legislations and customer value creation;

• more than 80% of trustees held that the process of appointment for service providers to pension funds (including umbrella funds) must be open and transparent. From the conceptual analysis, it became apparaent that due market control of administrative firms, administration, consulting, actuarial and investment services are done by the same firm and hence no transparent process exists for open and fair competition;

• trustee performance evaluation and appraisal is a critical governance standards and indicator of whether trustees are properly exercising fiduciary discretion without undue influence and usurpation of powers by dominant administrative firms who are motivated by commericla gain. According to Turney (2008), "performance management plays an important role in strategy execution. It is used to measure goal accomplishment, provide feedback on performance, predict future performance, and trigger analysis and corrective action. These benefits will only occur, however, if relevant and accurate performance measures are available for inclusion in performance management." Therefore, criteria for trustee performance evaluation must include a determination whether in managing the funds trustees have created mechanisms to create a fair competitive administrative environment based on customer value creation.

11. Discussion of Study Results

Although in macroeconomics (Lerner, 1934), market power is defined as the firm’s ability to price above marginal cost, the term is purposively used in the study to reflect all behavioral patterns of the firm showing a degree of control over consumers. In others words, those behaviors of the pension fund administrator that gives it latitude to influence pricing decisions and market structure. Therefore, as part of the anti-trust relevance test in the study conceptual model in Appendix 1, the following discussion classifies these variables under market dominance and market power:

11.1. Market Dominance

The study findings reveals a position of market dominance by few pension fund administration firms in Namibia. This conclusions are based on the following stylized findings:

Market power

• influencial role in the appointment of principal officers and trustees of umbrella funds

• information asymmetry given the custodial ownership and exploitation of memebr data of administrative firms

Market position (constraints imposed on competitors)

• exclusive service level agreements which prevents potential market entrants

• multi-carrier service structures based on bundling

• closed service delivery model (prohibition of external consultants)

Expansion and entry

• vertical integration busines models which constrain market entry

• expansion guanteed by exclusivity and cross selling strategies

Countervailing buyer power

• customer buying power significantly reduced by seamless administration systems (exiting members transitioned into firm’s default retail products) and lack of information

• governance capture (in terms of which firms dictate trustees appointments) compromised countervailing customer buying power.

• administrative firms controls voluntary pension fund industry bodies and further reduces any countervailing powers of pension funds

Power to increase price above competition level for a significant period

• no regulatory guidance on nature and levels of administrave costs

• lack of transparency in pricing methods

• aggressive cross selling strategies

11.2. Market Structure

An analysis of the market structure is essential to complete an analysis of the market from an anti-trust and customer value perspective. Using the conceptual framework in Appendix 1, the study found the following:

Network effects

The technical standards of electronic processing in private administration make it prohibitively expensive and complicated for new entrants to enter the market. The standardized and routine nature of administrative services stifles innovation. The huge investments in internet-based technology for benefit payments and member records updates is a keeping potential entrants far away from entering the market.. The seamless member transfer capability of administration technology denies potential competitors of an opportunity to access the data and offer alternative solutions, especially in the retail environment.

Entry and exit barriers

Vertical integration of services serves as the most effective barrier of entry strategy for administrative firms. Under this arrangement, one firm usually carries out all the administration, advisory and investment functions on umbrella funds. This has led to a service monopoly and excessive reliance on one service provider at the expense of market competitiveness. The exit barriers are presented by switching costs imposed on exiting funds by administrative firms. This becomes a disincentive to leave.

Marginal costs significant compared to fixed costs

Given the lack of regulatory guidelines on costing levels, the princples of free market economy applies and marginal costs are based on profit maximization appetites. Therefore, the observation is that in most cases, marginal costs by far exceeds fixed costs. This conclusion is also supported by the bundled service delivery model based on cross-subsidization of costs between administration, advisory and investment services.

Differentiation of products

Although administration services (in terms of process and procedure) in Namibia are homogenous, heterogeneity is visible in service delivery and complimentary products like housing loans, member projection statements (net replacement ratio). This makes it easy for firms to determine price based on these additional complimentary products (under the guise of originality and value addition). These heterogeneous products like pension-backed lending and annuity products has created opportunities for secret profits and undisclosed fees made from the administration of pension funds. This has led to smart partnerships with commercial banks and insurance companies to hide the true nature of products and profits derived from this. Complexity around products like projection statements, life stage administration and member level choice is heightened to benefit from oligopolistic nature of the market.

12. Discussion of Competitive Impact Tests

As indicated before, the study conceptual framework was based on applying the anit-trust and customer impact test as illustrated in Appendix 1 hereto. The following is a discussion of the result of the two tests:

Anti-trust impact test:

• the Namibian pension fund administration market reveals oligopolistic tendenies in that only few administration firms dominates the landscape;

• market dominance of these few administrative firns due to enornous market power and control through infromation asymetry and service dependency;

• evident barriers to entry based on exclusivity and vertical integration service delivery model of administrative firms;

• market concenttration

Customer impact test

• no transfer of direct financial or economic advantage to customers or members due execssive administration costs (evident diseconomies of scale derived from mismatch between bundling of services and net impact of administrative fees on member values);

• low net replacement rates of members of pension funds;

• no administrative efficiencies evidenced by poor benefit administration by some of these dominant frims (late payment of benefits);

• conditional selling and integrated cost structures making customer mobility difficult;

• artifical brand loyalty based on preceived economies of scale and concentrated nature of the market, and

• lack of transprancy making it difficult for customers to understand the real impact of administration services

Based on the application of the anti-trust test (forming the conceptual basis of the study), some of the practices of administrative firms in Namibia like cross selling and aggressive commercial tactics constitute anti-competitve behaviour contrary to the Competition Commission Act.

The study also found, after application of the customer impact test, that customers drive no real financial advantage or service convenience from the current oligopolitic market structure. Market dominance by few administartive firms has resulted in undesirable mobility constraints, coercive buying and lack of transparency for customers.

13. Conclusion

The primary aim of the study was to investigate the nature of pension fund administration market practices and appraise the potential of these practices in relation to anti-competitive behavior and consumer protection (members of pension funds.

The study results have revealed that the current market practices in pension fund administration are tainted with charactieristics of unfair competition bordering on non-compliance with the Competition Act.

Regulatory policy on pension fund administration is sparse and conducive to some of these ubiquitous business practices. Administrative firms have leveraged their market dominance thorugh, inter alia, structured influence over the appointment of trustees and the principal officers of umbrella funds. This guarantees commercial sycophancy and sheepish obedience to the potentially conflicting interests of the administrative firm.

From the above findings, an unavoidable conclusion is that the administration model of pension funds in Namibia is sophomoric and opaque and tainted with signs of oligopoly. This arrangement is an antithesis to fair competition and against the social protection objective of pension funds. Therefore, on both the supply and the demand side, there is overwhelming empirical evidence that suggest that the nature of the Namibian pension fund administration market is oligopolistically imperfect. The application of the multi-dimensional anti-trust and customer impact tests have also found the Namibian pension fund administration market to be unfavorably disposed towards administrative firms at the expense of pension funds and members who derive no real economic value or efficiencies from the current market configuration. The above study outcome creates a foundation for pension fund industry practitioners and regulators (including the Competition Commission) to critically review the commercial practices of some of these dominant administrative firms and enforce compliance with relevant Namibian anti-trust laws. Equally trustees of pension funds can use these findings to execute their fiduciary mandates and ensure that members’ interests are protected from these predative commercial practices of administrative firms.

Appendix 1. Research Conceptual Model

References

- World Bank. (1994). Averting the Old Age Crisis: Policies to protect the old or promote growth. Oxford.

- Botha E., Makina, D. (2011) Financial Regulation and Supervision: Theory and practice in South Africa, International Business& Economic Research Journal, Volume 10 Number 11.

- Bikker and Spierdijk (2009), Measuring and explaining competition in the financial sector, University of Utrecht.

- Bikker, J., & Dreu, J. (2009). Operating costs of pension funds: The impact of scale, governace and plan design. Journal of Pension Economics and Finance.

- Centre for European Policy Studies (CEPS), 2009. "Tying and other potentially unfair commercial practices in the retail financial services sector", Final reports, submitted to the European Commission, DG Internal Market and Services ETD/2008/IM/H3/78.

- CPB Document No. 29 February 2003, "Tight Oligopolies: In Search of Proportionate Remedies". Canoy, M., Onderstal, S.

- FIM Bill. (2014). Financial Insitutions and Markets Bill. FIM Bill. Windhoek: NAMFISA.

- Head of Department, Department of Education, Free State Province v Welkom High School and Another; 2013 (9) BCLR 989 (CC); 2014 (2) SA 228 (CC) at par 84

- IOPS. (2011). Working Papers on Effective Pension Supervision No 14.

- King. (2009). King Code of Governance for South Africa. IOD. IOD.

- Leedy, P. D. 1997. Practical research: Planning and design. Ohio: Prentice Hall.

- Lerner, A. P. (1934). The Concept of Monopoly and the Measurement of Monopoly Power. The Review of Economic Studies, 1 (3), 157-175. http://dx.doi.org/10.2307/2967480

- Miles and Huberman (1994). Qualitative data analysis: An expanded sourcebook (2nd ed.). Thousand Oaks, CA: Sage Publications.

- Mitchell’s Plain Town Centre Merchants Association v McLeod and Another 1996 (4) SA 159 (A) at 167I-168A as quoted by Parker, AJ in the case of NAMAF and Others v. Namibian Competition Commission and Another 2016 (A348/2014) 2016.

- NAMAF and Others v. Namibian Competition Commission and Another 2016 (A348/2014) 2016 NAHCMD.

- NAMFISA. (2014). NAMFISA Annual Report. Windhoek.

- OECD (2001), Administrative costs and the organization of individual account systems: A Comparative Perspective, Private Pensions Series Private Pensions Systems Administrative Costs and reforms.

- OECD (2008), Latin American Economic Outlook, OECD Publications.

- OECD. (2009). OECD Guidelines for Pension Fund Governance. OECD.

- Patton, M. Q. (2002). Qualitative evaluation and research methods (3rd ed.). Thousand Oaks.

- SA National Treasury. (2012). Preservation, portability and governance for retirement funds.

- Salkind, N. (2012). Exploring Research. Pearson.

- Saunders, M, Thornhill A., Lewis P. (2012) Research Methods for Business Students, 6th Edition, Pearson.

- South African National Treasury. (2013). Charges in South African Retirement Funds. Pretoria, South Africa.

- Stock & Sherbourne. (2004). Namibia Stock Exchange and Domestic Asset Requirements: Options for the future. Windhoek: NEPRU.

- Rosenberg S., O’Halloran, P. (2014) Firm Behavior In Oligopolistic Markets: Evidence From A Business Simulation Game, Journal of Business Case Studies – Third Quarter 2014 Volume 10, Number 3.

- Rusconi, R. (2008). South African Insitutional Investments: Whose money is it anyway?

- Turney, B. B. (2008), Activity-Based Costing: An Emerging Foundation for Performance Management, Cost Technology, Inc.

- Whinston M. D. (1990), "Bundling as a way to leverage monopoly", National Bureau of Economic Review.