American Journal of Marketing Research, Vol. 1, No. 3, October 2015 Publish Date: Aug. 7, 2015 Pages: 174-182

Measuring Service Delivery in Albania’s Banking Sector Mystery Shopping in a Financial Institution

Ana Buhaljoti*, Arjan Abazi

Department of Marketing – Tourism, University of Tirana, Faculty of Economics, Tirana, Albania

Abstract

This paper will measure the quality of the service delivery in the banking sector of Albania through the case of a recognized financial institution. It discusses the phenomenon of Mystery Shopping, as a valuable form of observation, to monitor the processes and procedures used in the delivery of the service within the financial institution. By making use of mystery shoppers, well-trained persons who behave as normal customers but are precisely observing what is going well and what can be improved in the service delivery, a case study of a bank is developed and results are shown. The objective of the study is to assess the level of customer service and measure the services standards in the branches of the bank in terms of six dimensions (i) Accessibility; (ii) Product Sale; (iii) Customer Care; (iv) Professionalism; (v) Transparency; (vi) Branch Appearance; which are combined to calculate the bank index. During June 2015, 19 mystery shop visits are executed, in 8 different branches by 5 different mystery guests. To make the mystery shopping visits as objective and measurable as possible a questionnaire with the six standard dimensions had to be filled by the mystery guest after the visits.

Keywords

Mystery Shopping, Service Delivery, Banking Sector, Customer Service, Financial Institution, Albania

Received: July 2, 2015

Accepted: July 30, 2015

Published online: August 8, 2015

@ 2015 The Authors. Published by American Institute of Science. This Open Access article is under the CC BY-NC license. http://creativecommons.org/licenses/by-nc/4.0/

1. Introduction

The use of "mystery shopping" to test the quality of customer service delivery is increasing emphasis on quality and service management. While service managers set service standards, the task of delivering these standards falls to customer-facing staff. (Wilson, 1998)

The inseparability nature of services indicates that the value for customer is created mainly in the consumption process and derives from the customer experience at the point of sale or with service distributor. (Otto 2004)

Because services are intangible, cannot be stored, transported, or inventoried and they cannot be separated from the person of the seller, variations in service performance have a major impact on customer satisfaction. (Donnelly, Jr. 2012) Bateson (1992) emphasized that the customer's experience during the delivery of a service is as important to customer satisfaction as is the benefit that the service provides. This means that 'how' you perform a service is often as important as 'what' you perform. (Wilson, 1998)

The aim of this study is to measure the quality of the service delivery to the customer in the banking industry. In this situation the research performed through mystery shoppers can be focused on the compliance to specific standards, guidelines and position the quality of the service on a standard that should be achieved. (Hesselink, 2003).

Study objectives include testing whether the service provided meets declared aims and standards, assessing the administrative functions and interpersonal skills of bank employees. Evaluate professionalism, transparency, appearance, identify strengths and weaknesses and help to show where service delivery can be improved (Morrison et al, 1997)

Various publications are available on the implementation of mystery shopping in Banks (Holliday, 1994; Morral, 1994; Dorman, 1994; Hotchkiss, 1995; Hoffman, 1993; Stoval, 1993; Leeds, 1992 and 1995; Hanke, 1993, Tepper, 1994) as refered by Hesselink (2003).

However, in Albania, mystery shopping has been rarely used by financial organizations, retailing, and hotel and no academic research on evaluating bank performance has been found.

2. Literature Review on Mystery Shopping

Mystery shopping is a form of participant observation where the researcher interacts with the subject being observed. It derives from the field of anthropology as observers became part of a tribe's daily life in order to understand the norms and behaviors that were neither documented nor communicable via language. Wilson (1998) through Friedrichs and Ludtke (1975) state that "There is often a discrepancy between real and reported behavior". (Ludtke,1975) Often interviews statements do not comply with the factual behavior of the interviewed persons. Personal interpretation and verbal capabilities of the interviewed person can limit the quality of the information gathered. (Wilson 1998).

Especially in the services context, observational methods are able to provide information on the service experience and help to develop a richer knowledge of the experiential nature of services (Grove and Fisk, 1992). The participant can identify dimensions of the service unlikely to be detected by a nonparticipant observer. However, there is an ethical issue involved in observing people without their knowledge as it may violate their rights to privacy. Jorgensen, 1989 argues that services are often performed in public sites where their delivery is observed by members of the public other than the specific recipient of the service. Mystery shopping is a clear example of participant observation in a public site as mystery shopping uses a structured approach of checklists to gather and measure specific information about service performance in everyday conditions (Grove and Fisk, 1992). (Wilson 1998)

"Mystery shopping is a valuable exercise for studying and evaluating service delivery performance within the banking industry" Gobo. It uses researchers called mystery shoppers to act as customers to monitor the processes and procedures used in the delivery of a service. The researchers pretend to be customers and go through all stages of the shopping experience from entry to the point of sale to exit, ask for information and also make purchases. The researchers are trained on product information, securities regulation, sales practices of retail banks and also on how to approach the banks and act during the customer interview. At the end of the visit, the researcher complies a structured evaluation form recoding what happened. (Gobo)

In particular, mystery shopping results in banking industry are used for three main purposes:

• To detect weak points in the bank’s service delivery.

• To encourage service personnel by linking with appraisal, training and reward mechanisms.

• To assess the competitiveness of the banks’ service provision against the others in the industry. (Hesselink 2003)

3. Research Design and Methodology

A qualitative research approach, mystery shopping approach is being used to measure the service experience as it unfolds. It looks at the activities and procedures that happen in the delivery of a service rather than gathering opinions about the service experience. Unlike customer satisfaction surveys it is a snapshot of actual events, such as sales or service interactions and tells what employees are doing, not customer’s opinions.

"Mystery shopping differs from other methods of assessing service user satisfaction in that the technique deals with the "here and now" of services, and records, in detail, the component parts of each element of contact with the service user" (Brend Group)

Thus, it is described as a method for measuring whether the service provided meets declared aims and standards declared by the management and customer. Mystery Shopping collects facts rather than perceptions. These facts can relate to basic enquiries, purchases and transactions.

Based on the findings of the literature review and the objectives of the study six major sections representing the bank standard dimensions were covered:

• Accessibility – the extend information and services are available to the clients.

• Sales and services – the extend bank delivers its services or products in a way that persuades the clients by assessing their needs in the most efficient, fair, cost effective, and humanly satisfying manner.

• Customer Care – the professionalism, friendliness and expertise of the bank employees toward efficiency and reliability fulfilling orders.

• Professionalism – the level of excellence or competence that is expected from a bank employee.

• Transparency – the degree of disclosure to which agreements, dealings, practices, and transactions are open to all for verification.

• Branch Appearance – outward impressions, indications, or circumstances affecting a public image of the bank

Questionnaire

A mystery shopper questionnaire was designed to document the shoppers’ experiences during their visits to the banks. The The questionnaire was composed of six major sections representing the standard dimensions (i) Accessibility (ii) Product Sale (iii) Customer Care (iv) Professionalism (v) Transparency (vi) Branch Appearance.

Each shopper was required to complete and submit the questionnaire to the service provider after the visit. Specific instructions were provided to the shoppers on how to approach the banks and act during the customer interview. In this regard, the shoppers were asked to perform four different scenarios:

• Scenario 1. Interaction with the teller: the shopper does a transaction at the teller

• Scenario 2. Ask for e deposit: the shopper does a transaction at the teller and afterwards goes to Customer Service and ask information for opening a Deposit according to a well prepared scenario

• Scenario 3. Ask for a Loan: the shopper does a transaction at the teller and afterwards goes to Personal Banker and ask information for opening a Deposit according to a well prepared scenario

• Scenario 4. Ask for a Credit Card: the shopper does a transaction at the teller and afterwards goes to Personal Banker and ask information for opening a Deposit according to a well prepared scenario

The scenario and number of visits per branch were two. All scenarios involved the Teller as the first contact with the bank. A total number of 19 visits were conducted in 8 branches of a private bank in Albania.

The shoppers observe and interact with the bank employees following the previously set scenario, record what happened during the meetings, complete the questionnaires and collect any materials provided by the Sales Representatives.

The reliability of this technique is defined as the extent to which similar observations made by different researchers would provide the same results (Easterby-Smith et al, 1991).This is a very important issue if mystery shopping results are to be taken seriously . Objective measurement is clearly possible in verifying whether an activity did or did not happen as the customer's name was used . However, judgments on the appearance of the premises and staff as well as the actions of staff in terms of politeness, product knowledge and helpfulness are slightly more subjective. Users and agencies attempt to minimize this subjectivity by using rating scales .This is often supported by verbatim comments from shoppers to justify their rating selection.

Consequently, each question in the questionnaire has been considered as a standard that should be achieved and get answers like (1) Yes and (2) No, meaning that either a standard is achieved or not.

Each of the questions in the questionnaire is followed by a comment section, which implies the necessity of proving and illustrating whether a standard is achieved or not with corresponsive arguments.

Each dimension measured through the questionnaire has a total score of 100 points.

Branch Index is composed by combining the scores of all six dimensions each with the following weight.

| Accessibility | 10 % |

| Sales & Services | 30 % |

| Customer Care | 15 % |

| Professionalism | 25 % |

| Transparency | 10 % |

| Branch Appearance | 10 % |

| ______ 100% |

Figure 1. BSM "Branch Standard Measurement Score".

Except Accessibility dimension all other dimensions points are generated as the ratio of positive answers over the total answers included in that dimension.

Accessibility dimension points is calculated as the mean waiting time to get served by the bank employee.

Branch Standard Measurement Score

The standard score is a scale that classifies branches based on their overall score from 0-100, where 100 means that the maximum quality standard aimed is achieved. Based on the above, in order to avoid confusion with the overall score of branches it was decided that all branches that score up to 50.9 points should be considered as "0 - out of standard" and all those branches that scored from 91-100 points as "5-the standard".

4. Results of Mystery Shopping

During June 2015, 19 mystery shop visits are executed from 5 different mystery shoppers. The scores of the visits are presented in this section, where a distinction is made between the six categories of criteria.

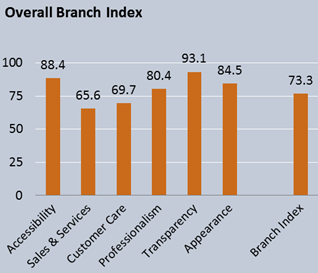

The unified branch index score is 76.8 out of 100, positioning the bank at the "Fair" standard quality scale. The main gaps stand in the dimensions of sales & service and customer care.

In Sales & Service dimension the bank has the lowest performance scoring 65 points out of 100.

Figure 2. Overall Branch Index.

Table 1. Key Findings in depth of sales and services.

| The employee…. | Scenarios | |||

| Interaction with Teller | Ask for a Deposit | Ask for a Loan | Ask for a Credit Card | |

| Welcomed the customer | 75.0% | NA | NA | NA |

| Teller asked customer for an ID | 64.7% | |||

| Teller was professional and friendly during transaction | 71.7% | |||

| Teller used the sales tool or product offering | 13.6% | |||

| Teller greeted the customer in a warm way | 75.5% | |||

| …started reacting immediately upon request for information | 92.0% | 98.2% | 95.0% | |

| Asked appropriate questions | 74.0% | 78.6% | 72.5% | |

| Summarized client’s needs | 52.0% | 69.6% | 62.5% | |

| Demonstrated good or very good product knowledge | 76.0% | 83.9% | 72.5% | |

| Answered clearly the questions | 88.0% | 92.9% | 87.5% | |

| The employee used leaflets to explain the product | 54.0% | 76.8% | 62.5% | |

| Explained the product benefits | 68.0% | 66.1% | 72.5% | |

| Explained the benefits of being a bank client | 42.0% | 58.9% | 52.5% | |

| Ended conversation friendly | 90.0% | 100.0% | 90.0% | |

Sales and Service

Overall results are presented in Table 1 and show that upon entering the bank, 48% of the shoppers were noticed (drew the attention of at least one bank employee), 40% felt welcomed and about the same were offered help. However the level of welcomeness perceived improves when they are attended from the teller (75%), and even more when getting personalized service by the personal banker or customer service (90%).

More than 90% of the employees started interacting immediately when their service was prompted by the customer. The overall experience was perceived as satisfactory especially on the services involving the Personal Banker. In average 65% of the bank employees were using leaflets (to be highlighted that the Personal Banker used promotional materials in 77% of the visits).

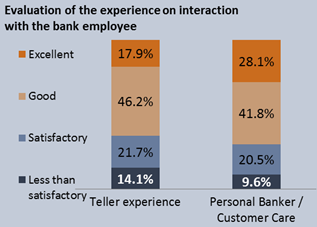

Customer Service

The experience with the personal banker or the customer service has been evaluated as "excellent" in 28% of the visits, compared to the experience with the teller in 18% of the visits. Overall there is a less satisfactory experience with the teller compared to the personal banker.

BRANCH INDEX

Mystery shopping results of three major branches are presented below.

Figure 3. Evaluation of the experience on interaction with the bank employee.

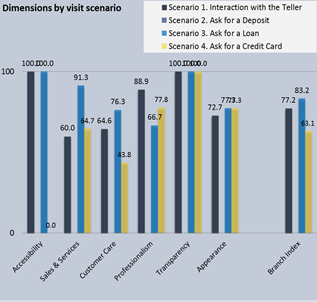

Figure 4. Branch 1, Dimensions by visit scenario.

Below are presented the qualitative interpretations of Branch 1 performance by dimensions (Figure 5).

Figure 5. Qualitative interpretation of branch 1 performance (selected quotes).

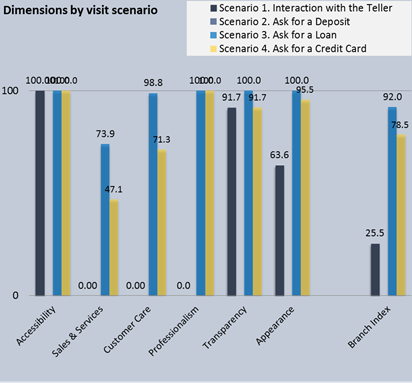

Branch 2 Index

Branch 2 performance is ‘Poor’ (65.3 points). ‘Sales & Services’, ‘Customer Care’, ‘Professionalism’ dimensions resulted to be negative in the interaction with the teller scenario.

Branch Index for the teller amounts 25.5 points resulting to an "out of standard" performance.

Qualitative interpretation of branch 2 performance (selected quotes) are presented in Figure 7.

Figure 6. Branch 2, Dimensions by visit scenario.

Figure 7. Qualitative interpretation of branch 2 performance (selected quotes).

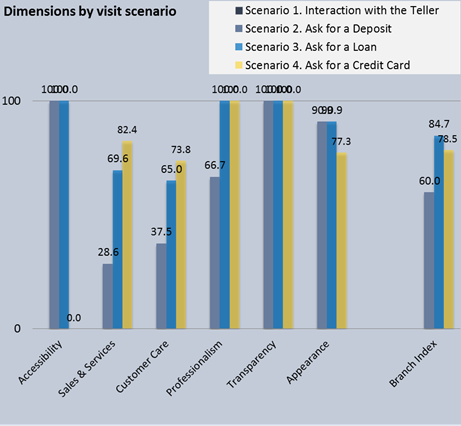

Branch 3 Index

Branch Index (BI) for Branch 3 is 74.4 points on the Brand Standard Measurement (BSM) scale.

This branch was evaluated based on the deposit, loan and credit card scenarios. The branch has performed the worse on the ‘Ask for a Deposit’ scenario, where ‘Sales & Service’ dimension in this visit scored as low as 37.5 points and ‘Customer Care’ 28.6 points (Figure 8).

Qualitative interpretation of branch 3 performance (selected quotes) are summarized in Figure 9.

Figure 8. Branch 3, Dimensions by visit scenario.

Figure 9. Qualitative interpretation of branch 3 performance (selected quotes).

5. Mystery Visits Findings

Some major findings and solutions resulting from the Mystery Shopping Exercise in the financial institution are summarized below.

Findings: From this mystery shopping evaluation, the bank learnt that its employees did not consistently use customers' names, an important practice in order to provide top-notch customer service.

Solution: To address this issue, the bank shall institute training that help employees identify ways that they could learn and remember customers' names-through a friendly introductory greeting or by glancing at the customer's check

Findings: The employees failed in practicing cross selling and upselling. The banker did not offer sale on cross selling products.

Solution: Getting the employees involved in those exercise and motivating them to sell more to existing clients requires continuous training from the bank. Employees should be trained how to explore customer's needs through asking appropriate questions and how to close a sale without feeling too pushy.

Findings: Employees were unable to close a sale by neglecting to follow up the client.

Solution: The employees should be monitored to carefully register the data of a potential client and follow him after a certain time frame.

6. Conclusions

The Exercise has shown that more efforts should be made to improve the overall quality of explanation of features and disclosure of risks provided by the sales staff. The major improper practices were:

(i) Insufficient understanding of products. Some sales staff did not demonstrate sufficient understanding of the recommended products.

(ii) Insufficient explanation of the features and risks of the products recommended. It would be difficult for the sales staff to properly discharge their suitability obligations to clients.

(iii) Insufficient information delivered to clients. Some sales staff failed to provide sufficient information about the recommended products to the shoppers, such as, the features and risks of the products, relevant fees and charges.

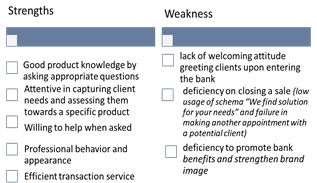

Overall the Mystery Shopping Exercise uncovered the following strengths and weaknesses of service delivery in the financial institution. (Figure 10)

Figure 10. Strengths and Weaknesses of Bank Service Delivery.

Future Implications

The scores of the visits will be delivered to the official structure of the company working on the program "We find solutions for your needs" and Service Excellence Program. This means that mystery shopping exercise will allow the actual results to be compared with the objectives formulated at the beginning of the program.

Suitability Assessment

Insufficient explanation of rationale behind recommendation

The sales staff generally did not sufficiently explain why the products were suitable for the shoppers having regard to their individual circumstances. Failure to provide a clear rationale for product recommendations would make it difficult for clients to assess whether the recommendations are suitable for them.

Some bankers did not explain clearly and explicitly how commission worked, increasing the potential for misunderstanding

Recommending products to clients without proper regard to their specific circumstances

It was noted in some instances that the sales staff did not take into account all the relevant personal circumstances of the shopper when making the assessment. As banking products tend to get very complex and dynamic, helping the customer to choose the right product requires

Know-Your-Client

In order to better understand their customer, the bankers should collect from each customer relevant information that includes their financial situation, investment objectives, investment experience, investment knowledge, investment horizon, risk tolerance and education level, etc.

References

- Brent Homeless User Group ‘ Mystery Shopping Report’ May 2009http://www.crisis.org.uk/data/files/publications/090929%20Mystery%20Shopping.pdf

- Bateson, J.E.G., 1992, Managing Services Marketing, 2nd Edition. Dryden Press, Orlando, USA.

- Dawson, J. and Hillier, J., 1995, 'Competitor Mystery Shopping: Methodological Considerationsand Implications for the MRS Code of Conduct', Journal ofthe Market Research Society,Vol.37, No.4, pp.417-27.

- Donnelly, Jr.James H. 2012, Marketing Intermediaries in Channels of Distribution for Services Journal of Marketing, Vol. 40, No. 1 ,pp. 55-57, Published by American Marketing Association

- Grove, S.J. and R. Fisk, 1992, 'Observational Data Collection Methods for Services Marketing:

- An Overview', Journal ofthe Academy of Marketing Science, Vol.20, No.3, pp.217—24.

- Gobo, Giampietro ‘A technique of applied ethnography’, University of Milano,http://podcast.spolitiche.unimi.it/podcast/vrs/Lezione12_2.pdfRetrieved 20.06.2015

- Johnston, R., 1988, 'Service Industries: Improving Competitive Performance', Service IndustriesJoumal,Vol.8, No.2, pp.202-lI..

- Jorgensen, D.L., 1989, Participant Observation: A Methodology for Human Studies, , NewburyPark, CA: Sage Publications

- Leeds, B., 1995, 'Mystery Shopping: From Novelty to Necessity', Bank Marketing, Vol.27, No.6, pp. 17-23.

- Morrison, L.J., A.M. Colman and CC. Preston, 1997, 'Mystety Customer Research: CognitiveProcesses Affecting Accuracy', Joumal of the Market Research Society, Vol.39, No.2, pp.349-61

- Morrall K., (1994), Mystery shopping tests service and compliance, Bank Marketing, 26 (2), 13 23.

- Morrison L.J., Colman A.M. and Preston C.C., (1997), Mystery customer research: processes affecting accuracy, Journal of the Market Research Society, 39 (2), 349-361.

- Wiele A. van der, Boselie P., Hesselink M., Empirical evidence for the relationship between customer satisfaction and business performance, MSQ, 12 (3), 2002, 184-193.

- Hesselink Martijn, Van Der Wiele Ton , 2003 Mystery Shopping: In-Depth Measurement Of Customer Satisfaction, Erasmus Research Institute Of Management, Journal of Economic Literature (JEL),

- Rudawska Edyta 2011, Customer as an active partner in creating offer in banking services, International Journal of Management Cases , University of Dubrovnik, Croatia 27th-29th April 2011

- Wilson Alan 1998, The Use of Mystery Shopping in the Measurement of Service Delivery Service Industry Journal The Service Industries Journal. Volume 18, Issue 3