American Journal of Marketing Research, Vol. 1, No. 3, October 2015 Publish Date: Jul. 29, 2015 Pages: 93-98

Impact of Capital Market Growth on Economic Growth and Development in Nigeria

Christain U. Amu*, N. C. Nwezeaku, A. B. C. Akujuobi

Department of Financial Management Technology, Federal University of Technology Owerri, Imo State, Nigeria

Abstract

The capital market has been identified as institution that contributes to the economic growth and development of emerging and developed economies. It is a major driving force of economic growth and development of a nation. The main purpose of this paper is to evaluate the impact of growth in capital market on economic growth in Nigeria using regression analysis on annual data from 1981 to 2012. The results provide evidence to show that the capital market has significant positive impact on economic growth in Nigeria. The results also show, however, that growth in market capitalisation does not have significant impact on the economy in Nigeria. It is therefore recommended that capital market regulatory authorities should put in place polices that will enhance and sustain the market’s contribution to economic development.

Keywords

Capital Market, Economic Growth, Regression Analysis, Nigeria

Received: June 25, 2015

Accepted: July 17, 2015

Published online: July 28, 2015

@ 2015 The Authors. Published by American Institute of Science. This Open Access article is under the CC BY-NC license. http://creativecommons.org/licenses/by-nc/4.0/

Contents

1. Introduction 2. Review of Literature 2.1. Conceptual Framework 2.2. Empirical Literature 3. Methodology and Description of Data 3.1. Methodology 3.2. Description of Data 4. Empirical Results and Discussions 4.1. Graphic Presentation 4.2. Descriptive Statistics 4.3. Regression Results 5. Conclusions

1. Introduction

It is well established that economic growth and sustainable level of development remains the most significant macroeconomic objective of every well-meaning government, and these objectives have received the attention of scholars (Anyanwu, 1997; Levine and Zervos, 1998; Osuala, Okereke and Nwansi, 2013). Economic development is regarded as the major goal of national policy in any economy, while capital accumulation is also seen as a potent factor in the process of economic development it is regarded as the core process by which all other aspect of growth is made possible and feasible. Robinson (1952), for example, declares that "where enterprise leads finance follows". Accordingly economic development creates demands for particular types of financial arrangement and financial system automatically responds to these demands. Levine and Zervos (1998) have been able to show that the level of financial intermediation is a good predictor of economic growth.

The capital market has been identified as institution that contributes to the economic growth and development of emerging and developed economies. It is a major driving force of economic growth and development of a nation. Anyanwu (1988) found that Nigeria stock market is positively and strongly correlated with long run economic development. Thus, the capital market impacts positively on the economy by providing financial resources through it’s intermediation process for the financing of long term projects. The projects could be promoted by government or private sector institutions. They are usually in such areas as infrastructures, agriculture, solid minerals, manufacturing, banking and other financial services and other real sector areas; hence without an efficient capital market the economy may be starved of the required long-term fund for sustainable growth.

A good number of studies have been conducted to examine the impact of capital market on economic growth and development both in developed and developing economies (see for example, Levine and Zervos, 1998; Caporale, Howells and Soliman, 2004; Alajekwu and Achugbu, 2012; Osuala, Okereke and Nwansi, 2013). Caporale, Howells and Soliman (2004), for example, provide the evidence that an organized and managed stock market stimulate investment opportunities by recognizing and financing productive projects that lead to economic activity, mobilize domestic savings, allocate capital proficiency, help to diversify risks, and facilitate exchange of goods and services. Undoubtedly, stock markets are expected to increase economic growth by increasing the liquidity of financial assets, make global and domestic risk diversification possible, promote wiser investment decisions, and influence corporate governance that is, solving institutional problems by increasing shareholders’ value. Ekundayo (2002), on the other hand, argues that a nation requires a lot of local and foreign investment to attain sustainable economic growth and d development. The capital market provides a means through which this is made possible. However, the paucity of long-term capital has posed the greatest predicament to economic development in most African countries including Nigeria. Capital provides the impetus for the effective and efficient combination of factors of production to ensure sustainable growth and development. Moreover, it is the effective utilization of productive resources accumulated over time that will determine the pace of growth of an economy.

Granted that so many studies have investigated the capital market-economic growth nexus, most of the studies were conducted for developed countries and other emerging economies. The few available studies in the case of Nigeria have been overtaken by events such as global financial crisis and outdated data. Again, capital market development and economic development are country specific objectives. The specific factors that affect capital market, for example, include: government policies and regulations, depth and breadth of the market, economic reforms in place, etc. There is need therefore for recent empirical evidence on the impact of capital market development on economic growth and development in Nigeria, especially now that the devastating effect of the global financial crisis has abated.

The objective of this paper therefore is to evaluate the impact of capital market growth on economic growth and development in Nigeria. This study in very important because the Nigerian capital market which witnessed a meltdown in last few years is gradually recovering, moreover, the eroded confidence of shareholders and investors need to be restored. Thus it is expected that this study would complement the efforts of government and policy makers in complete revival of the Nigerian Capital Market and restoring the confidence of shareholders and other players in the market.

This paper will therefore contribute to existing literature on capital market growth on economic growth and development in Nigeria. The findings will also be useful to capital market regulatory authorities and aid in formulation of both economic and capital market development policies. The remainder of the paper is organised as follows. Section 2 presents the empirical literature. Section 3 embodies methodology and data. Section 4 presents the empirical results and discussions, and section 5 concludes the paper.

2. Review of Literature

2.1. Conceptual Framework

Economic development, according to Osamwonyi (2005), is an increase of the national income or total volume of production of goods and services of a country accompanied by improvements in the total standard of living of the people. It is comprehensively defined as a multi-dimensional process of a total upward structural shift of the social system in terms of a capacity and capability to produce, supply, distribute and consume goods and services required by a growing society with changing taste such that more efficient, higher and more equitable standard of living is attained and absolute poverty eliminated. It involves positive changes in the institutional, attitudinal, technological, economic and demographical elements of the society. These elements involve production, technological innovation, education, consumption, real per capita income, equitable distribution of gains of society, external trade, social, political and adaptive ideological orientation.

The capital market on the other hand is the market for longer-term funds and securities that tenor exceeds beyond one year. These include long-term loans, mortgage bonds preference stocks, ordinary shares, Federal Government bonds and industrial loans and debentures. The capital market can be defined as the section of the financial system that is responsible for channeling efficiently funds from the surplus to the deficit economic units on a long-term basis (Onoh, 2002). According to Al-faki (2006), the capital market is a network of specialized financial institution, series of mechanism, process and infrastructure, that, in various ways facilitates the bringing together of suppliers and users of medium to long-term capital for investment in economic development project. This market is the source from which companies and industries obtain capital for expansion and modernization and also from which government borrows on a long-term basis for development purposes. Capital market as a network of institutions and individuals made up of regulators and operators who together bring suppliers and users of capital and facilitate the smooth operation of the market. These institutions that form the capital market network includes investment banks, stockbrokers, issuing houses, underwriters, venture capital companies, professional consultants, fund managers, development finance companies, collective investments firms, and insurance companies. The statutory regulator is the Securities and Exchange Commission while the self-regulatory agency is the stock exchange. In Nigeria, there is the Nigerian Stock Exchange and the Abuja Commodity Exchange.

A stock exchange a place where securities (bonds, stocks and derivatives) are traded and where one can raise long-term capital in large amounts (Onoh, 2002). It seeks the efficient allocation of available capital funds to the diverse uses in the economy and through its extreme sensitive pricing mechanism ensures the available capital resources are allocated to firms with competitive returns. It also is a barometer for the condition of the economy.

2.2. Empirical Literature

A good number of studies have been conducted to examine the impact of capital market on economic growth and development. Levine and Zervos (1996) examines whether there is a strong empirical association between stock market development and long-run economic growth. The study used pooled cross-country time series regression of forty-one countries from 1976 to 1993 to evaluate this association. They find a strong correlation between overall stock market development and long-run economic growth exist. This means that the result is consistent with a positive relationship between stock market development and economic growth. Similarly, Bensivenga, Burce, and Ross (1996) conclude that well developed stock market induces long run economic growth.

Hamid and Sunnt (1998) examined the relationship between stock market development and economic growth for 21 emerging markets over 21 years, using a dynamic panel method. Their results indicate a positive relationship between several indicators of stock markets performance and economic growth both directly and indirectly by boosting private investment behaviour.

Azarmi, Lazar and Jeyapaul (2005) examine the empirical association between stock market development and economic growth for a period of ten years around the Indian market liberalization event (1981 – 2001). The study revealed among others that the Indian stock market development is not associated with economic growth for the study period 1981. On their part Ben and Ghanzouani (2007) reported that financial system development could have adverse effect on economic growth in a sample of 11 countries they studied, and therefore advocated for a vibrant financial sector.

Many authors have equally examined the capital market-economic development nexus in Nigeria. Nyong (1997) developed an aggregate index of capital market development and used it to determine its relationship with long run economic growth in Nigeria. The study employed a time series data from 1970 to 1994. Four measures of capital market development ratio of market capitalization to GDP (in %), ratio of total value of transaction on the main stock exchange to GDP (in %), the value of equities transactions relative to GDP and listing were used. The four measures were combined into one overall composite index of capital market development using principal component analysis. The financial market depth was included as control. It was found that the capital market development is negative and significantly correlated with the long growth in Nigeria.

Ewah, Esang and Bassey (2009) appraised the impact of capital market efficiency on economic growth in Nigeria, using time series data on capitalization, money supply, interest rate, total transaction and government development stock that ranges between 1961 to 2004. The result of the study shows that the capital market in Nigeria has the potential of growth inducing, but it has not contributed meaningfully to the economic growth of Nigeria. The study attributed the findings to the low market capitalization, low absorptive capitalization, illiquidity, misappropriation of funds among others. The study believed and suggested capital market remains one of the mainstreams in every economy that has the power to influence economic growth, hence it advised the organized private sector to invest in the capital market. Abu (2009) examined whether stock market development raises economic growth in Nigeria, by employing the error correction approach. The econometric results indicated that stock market development (Market Capitalization GDP ratio) increases economic growth. He however recommended the removal of impediments to stock market development which include tax, legal and regulatory barriers, development of the nation’s infrastructure to create enabling environment where business can strive, employment policies that will increase the productivity and efficiency of firms as well as encouraging the Nigerian Securities and Exchange Commission to facilitate the growth of the market, restore the confidence of stock market participants and safeguard the interest of shareholders by checking sharp practices of market operators. Ezeoha, Ogamba and Onyiukel (2009) investigated the nature of the relationship that exist between stock market development and the level of investment (domestic private investment and foreign private investment) flow in Nigeria. The authors discovered that stock market development promotes domestic private investment flows thus suggesting the enhancement of the economy’s production capacity as well as promotion of the growth of national output. However the result shows that capital market development has not been able to encourage the flow of foreign private investment in Nigeria. Some authors focus on the casual relationship between capital market development and economic growth of example.

Oke and Ojo (2012) found out that market capitalization and new issues are positively related to GDP implying that market capitalization and increase in stock aids economic development. They opined that increase in market capitalization as a result of primary capital market transactions is needed for economic development rather than improved liquidity in the secondary market. Alajekwu and Achugbu (2012) investigate the role of stock market development on economic growth of Nigeria using Ordinary Least Square (OLS) techniques on 15-year time series data from 1994 - 2008. Their results show that market capitalization and value traded ratios have a very weak negative correlation with economic growth while turnover ratio has a very strong positive correlation with economic growth. Also, stock market capitalization has a strong positive correlation with stock turnover ratio. This result implies that liquidity has propensity to spur economic growth in Nigeria and that market capitalization influences market liquidity. They recommended that government should make policies that boost the interest of domestic investors in Nigeria as this might spur investors’ interest and boost stock market activity.

Osuala, Okereke and Nwansi (2013) examine the existence of causality relationship between stock market performance and economic growth in Nigeria using the General-to-specific Autoregressive Distributed Lag (ARDL) / Bound testing approach on time series data covering the period 1981 – 2011. The study finds the empirical evidence of long-run co-integration between economic growth and stock market performance. However, with regard to causal relationship between GDP and Stock market performance indicators, a uni-directional causality was established from only TNDR to GDP on the short-run. On the long-run, there was no causal relationship between economic growth and stock market. The study therefore recommends that the regulatory authorities should initiate policies that would rekindle the dwindling interest and confidence of both domestic and foreign investors in the market, and also be more proactive in their surveillance role in order to checkmate negative practices which undermine market integrity.

3. Methodology and Description of Data

3.1. Methodology

To investigate impact of capital market growth on economic growth and development in Nigeria, we employ descriptive analysis and regression analysis. Descriptive analysis is the presentation of summary of the important statistics in a data set. Opara, Emenike and Ani (2015) conclude that researchers that are studying financial markets should start by describing their variables before delving into the inferential analysis. Our descriptive statistics therefore involve plotting of time series graph and computation of mean, standard deviation, skewness, kurtosis, and Jarque-Bera statistic for the level and growth series of capital market and economic development proxies. While the mean presents information on the average of the capital market and economic development series, the standard deviation shows the level of variation of the series from their average. The skewness and the kurtosis provide insight into their distributional pattern.

The regression analysis, on the other hand, was conducted using ordinary least square (OLS) method. The OLS enables the measure of the impact of independent variable(s) (X) on the dependent variable (Y). It is specified as follows:

GDPt = λ0 + λ1MCt + λ2INFt + εt (1)

The a priori expectation of the slope coefficient is: λ1 > 0.

Where GDP is the dependent variable and is the observations of yearly nominal gross domestic products, MCt denotes the yearly observations of the Nigerian Stock Exchange capitalisation, λ1 is the coefficient and its effect on nominal GDP and εt is the stochastic error term at time t.

3.2. Description of Data

The data for this study are yearly series of nominal GDP and yearly series of NSE Market Capitalisation. While the GDP proxy’s economic development, NSE capitalisation proxy’s capital market development, and Inflation rate serves as a control variable. The nominal GDP and inflation rates series were obtained from Central Bank of Nigeria (CBN) statistical bulletin for various years and MC series were obtained from the Nigerian Stock Exchange. The period under consideration for the variables ranges from 1981 to 2012.

4. Empirical Results and Discussions

4.1. Graphic Presentation

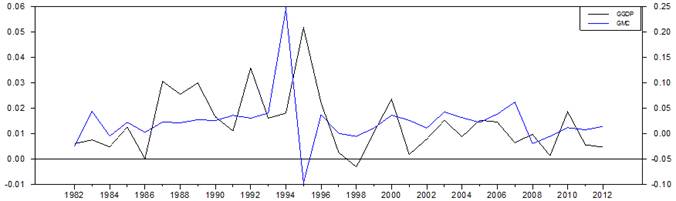

Figure 1 displays a time series plot of the growth in GDP and growth in NSE market capitalisation. Notice from this figure that the growth GDP maintain visible upward and downward spikes, with 1986 and 1998 having the least growth rates. The market capitalisation, on the other hand, achieved the highest growth rate in 1994 and least in 1995. Notice also the increase in market capitalisation growth rate from 2002 till its fall in the first quarter of 2008 as a result of the global financial crisis.

Figure 1. Relation between NSE Market Capitalisation and GDP (1981 – 2012).

4.2. Descriptive Statistics

Descriptive statistics of the GDP and Market Capitalisation series are presented in Table 1 below. From table 1, notice that the average GDP and average MC are 8853167.3 and 2632475.6 respectively for the sample period. However, the sample mean for growth in GDP and MC are 1.3% and 2.2% respectively. The standard deviation is 1.1% for growth in GDP and 5% for growth in Market Capitalisation. These show that market capitalisation has both higher growth rate and dispersion. The skewness and kurtosis coefficients under normality assumption are 0 and 3 respectively. But the skewness coefficients for growth in GDP and growth in Market Capitalisation are 1.28 and 2.55 respectively, and the kurtosis coefficients for growth in GDP and growth in Market Capitalisation are 2.17 and 13.8 respectively. The p-values show that the coefficient of the skewness for growth in GDP and growth in Market Capitalisation are not zero. The excess kurtosis of the growth in GDP is nonzero, and is not significant at 95% confidence, suggesting that series are leptokurtic. In the same vein, the Jarque-Bera statistics for both series suggest that may not be normally distributed at 5% significance level.

Table 1. Descriptive Statistics.

| Variable | Mean | Std Dev | Skewness | Kurtosis | J-B Stat. | Obser. |

| GDP | 8853167.3 | 11841430.8 | 1.500 | 1.263* | 14.138 | 32 |

| MC | 2632475.6 | 4522908.1 | 1.677 | 1.389* | 17.577 | 32 |

| Panel B: First Differenced Series | ||||||

| GGDP | 0.013 | 0.011 | 1.278 | 2.172* | 14.544 | 31 |

| GMC | 0.022 | 0.050 | 2.555 | 13.759 | 278.29 | 31 |

Note: GDP is the nominal GDP. MC is the market capitalisation. GGDP is the growth in nominal GDP and GMC is the growth in market capitalisation. * indicates not significant.

4.3. Regression Results

The summary of the results for the OLS model specified in equation (1) are presented in Table 2 below. Notice from Table 2 that Nigerian Stock Exchange Market Capitalisation has positive and significant impact on economic growth; the coefficient of market capitalisation is 0.711. The t-statistic and p-value stood at 26.17 and 0.000 respectively. This implies that the NSE market capitalisation contributes positively to economic development in Nigeria. The value of the coefficient of determination (R2) stood at 0.960. This indicates that 96% of the total variation in GDP is accounted for by the NSE market capitalisation. The Durbin-Watson coefficient (1.228) suggests that there is serial correlation in the series.

Panel B of Table 2 displays the regression results of the growth series of GDP and Market Capitalisation. We can see from Table 2 that growth in Market Capitalisation has negative but not statistically significant impact on growth in economic growth; the coefficient of the growth in market capitalisation is -0.016. The t-statistic and p-value are -0.37 and 0.708 respectively. These imply that growth in the NSE market capitalisation does not contribute to economic development in Nigeria. The negative impact of growth in Market Capitalisation on the economy may not be unconnected with the crash in the stock market as a result of the global financial crisis, which started in the United States of America in 2007. This crisis results in over 70% erosion of the NSE capitalisation. Both institutional and individual investors lost large amounts of their investment in the NSE. It was during this period that about three banks were nationalized in Nigeria. It is therefore not surprising that growth in the NSE capitalisation did not impact positively on economic development in Nigeria.

Table 2. Results of Regression Model.

| Variable | Coefficient | t-value | Prob. |

| Level Series | |||

| Constant | 5.815 | 11.973 | 0.000 |

| MC | 0.711 | 26.175 | 0.000 |

| INF | 0.023 | 0.222 | 0.825 |

| R2 = 0.960, F(2, 29) = 356.3 [0.000], DW= 1.228 | |||

| Growth Series | |||

| Constant | 0.0139 | 5.895 | 0.000 |

| GMC | -0.016 | -0.378 | 0.708 |

| GINF | 0.009 | 1.251 | 0.220 |

R2 = 0.609, F(2, 28) = 0.845 [0.439], DW= 1.504

5. Conclusions

The capital market has been identified as institution that contributes to the economic growth and development of emerging and developed economies. It is a major driving force of economic growth and development of a nation. Hence, this paper examined the impact of growth in capital market on economic growth in Nigeria using regression analysis. The data for analysis were obtained from the Central Bank of Nigeria (CBN) statistical database and covers the period 1985 to 2013. The estimates from the descriptive analysis show that both the GDP and market capitalisation series are not normally distributed at 5% significance level. The results from the regression model provide evidence to show that the capital market has significant positive impact on economic growth in Nigeria. The results further show, however, that growth in market capitalisation does not have significant impact on the economy in Nigeria. We therefore recommended that capital market regulatory authorities should put in place polices that will enhance and sustain the market’s contribution to economic development.

References

- Abu, N. (2009), Does Stock Market Development Raise Economic Growth? Evidence from Nigeria, Journal of Banking and Finance. 1(1), 15-26,

- Alajekwu, U. B. and Achugbu, A. A. (2012), The Role of Stock Market Development on Economic Growth in Nigeria: A Time Series Analysis, African Research Review, 6 (1), Pp. 51-70

- Al-faki M. (2006), The Nigerian Capital market and Socio-Economic Development, distinguished Faculty of Social Science, public Lectures, University of Benin, 9-16

- Anyanwu J.C. (1997), Stock Market Development and Nigeria’s Economic Development, Nigerian Financial Review, p.6-13.

- Azarmi, T., Lazar, D. and Jeyapaul, J. (2005). Is the Indian Stock Market a Casino? Journal of Business and Economic Research, April, Vol. 3, No. 4, pp 63 – 72.

- Ben N. S. and Ghazouani, S. (2007), Stock Markets, Banks and Economic Growth: Empirical Evidence from MENA Region, Research in International Business Finance, 21(2), 297-315.

- Becncivenga V. R., Burce D. S. and Ross M. S. (1996), Equity Markets, Transaction Costs, and Capital Accumulations: An illustration. The World Bank Review, 10(2), 241-265.

- Caporale, G. M., Howells, P. G. and Soliman, A. M. (2004), Stock Market Development and Economic Growth: The Causal Linkages, Journal of Economic Development, 29(1):33-50.

- Ewah, S., Esang, O. E., Atim, E. and Bassey, J. U. (2009). Appraisal of Capital Market Efficiency on Economic Growth in Nigeria. International Journal of Business and Management, 4(12), pp 219 – 228.

- Ezeoha, A., Ogamba, E and Onyiuke, N. O. (2009), Stock Market Development and Private Investment Growth in Nigeria. Journal of Sustainable Development in Africa, 11(2): 20 – 35.

- Levine R. and Zervos, S. (1998), Stock Markets, Banks and Economic Growth. American Economic Review, 88(3), pp.537-558.

- Opara, C. C., Emenike, K. O. and Ani, W. U. (2015), Behaviour of Nigeria Financial Market Indicators: Evidence from Descriptive Analysis, American Journal of Economics, Finance and Management, 1 (5), pp. 421-429. Retrieved fromhttp://www.aiscience.org/journal/ajefm

- Osamwonyi, I. O. (2005), Capital Market Imperfections and Community Economic Development in Nigeria, A paper presented at the Academy of Management Nigeria on the 23rd of November, Abuja.

- Osuala, A. E., Okereke, J. E. and Nwansi, G. U. (2013), Does Stock Market Development Promote Economic Growth In Emerging Markets? A Causality Evidence from Nigeria, World Review of Business Research, 3 (4), Pp. 1 – 13