American Journal of Marketing Research, Vol. 1, No. 3, October 2015 Publish Date: Jul. 31, 2015 Pages: 106-112

Efficiency of Pension Funds in Namibia

Manfred Rii Zamuee*

The Research Department, Maastricht School of Management (MSM), Maastricht, Netherlands

Abstract

Pension funds are a major driver of GDP for many countries including Namibia and have given rise to the establishment of stock markets and the asset management industry. Therefore, it has become imperative for pension funds to be efficient in the manner in which they are managed. While previous studies have addressed the issue of efficiency in many disciplines, not much literature could be found on the analysis of efficiency of pension funds in general and Namibia in particular. The study attempts to demonstrate the Namibian experience in terms of the levels of efficiency of pension funds. The financial efficiency of pension funds was measured with the aid of Data Envelopment Analysis (DEA) using various inputs and outputs. On the other hand, operational efficiency was measured using various latent constructs. Therefore, Structural Equation Modelling (SEM) and Confirmatory Factor Analysis (CFA) form the theoretical basis to validate and operationalize the variables in the model. The study uses questionnaire based survey conducted among members of the board of trustees of approximately 180 pension funds in Namibia, representing about 60% of the Namibian pension fund industry. The results of the study indicates the importance of efficiency in the management of pensions funds in Namibia and aims to contribute to the current literature on the use of SEM, CFA and DEA as more reliable tools to measure pension fund efficiency.

Keywords

Financial Efficiency, Operational Efficiency, Structural Equation Modelling, Confirmatory Factor Analysis, Investments, Governance, Benefit Design

Received: June 24, 2015

Accepted: July 17, 2015

Published online: July 28, 2015

@ 2015 The Authors. Published by American Institute of Science. This Open Access article is under the CC BY-NC license. http://creativecommons.org/licenses/by-nc/4.0/

1. Introduction

Pension funds are an essential driver of macro-economic stability (Stiglitz, 1999) and contribute significantly to GDP’s of global economies, including Namibia. Pension fund investments have given impetus to the development of financial markets, stock broking and asset management industry in Namibia (Stock & Sherbourne, 2004), (Volan, 2005). Namibia’s gross domestic savings as a percentage of GDP is one of the lowest in the region at 6.4%, behind Botswana at 29% and South Africa at 18%. In Chile it is 23.6%, Malaysia at 35.4%, United Kingdom at 15.2% and USA at 16.8% (World Bank, 2013). Furthermore, Namibia not only has a saving problem, but a high fiscal and current account deficit (Shiimi and Kadhikwa, 1999). Against this background, pension funds constitute the largest source of personal income and savings for many people globally, and Namibia is no exception (Hassan, 2008), (Jablonsky, 2005) (Devereux, 2001). In Malaysia the pension fund savings significantly contributed to national savings accounting for almost 30% (Bateman and Piggot (1997). Although the debate is on-going on whether private pension funds alone can raise national savings, the pendulum of opinion seem to swing in favour of the view that pension funds are vital instruments to help alleviate poverty and catalyse economic development if managed efficiently. (Stiglitz and Orszag (1999), (BON, 2010).

Researches in the area of pension economics have found that national savings from private pension funds can be eroded by negative demographic developments (i.e. aging populations), making pension fund savings inadequate to achieve a retirement safety net (Schieber and Shoven, 1994). Therefore, the rate of investment returns earned by pension funds is correlated to demographic dynamics (i.e. the age profile of the pension fund membership). The above finding makes it important to understand the significance of the relationship between age and efficiency in the management of pension funds. According to the World Bank, Namibia has unfavourable demographic developments with a fast aging population and slow population growth levels (World Bank, 2014) (Subbarao, 1998). However, the demographic challenges seem to be a regional and global phenomenon with Botswana, South Africa and a great part of Europe sharing the same demographic challenges (Viceira, 2007), (World bank, 2014). This demographic dynamics makes it absolutely necessary for pension funds in Namibia to be efficient in the management of member investments to avoid inter-generational welfare catastrophe.

On the structural side, the Namibian pension fund environment is made up of a State funded universal old-age pension, private occupational-based mainly defined contribution schemes and a private voluntary pension fund arrangement. This structure resembles the World Bank three-tier structure similar to many other developing countries in the world (Holzmann, 2000), (World Bank, 1994). The World Bank pillar system has been criticised as being too deterministic and at times incongruent with the nuances of many countries (Stiglitz and Orszag1999). Nevertheless, the private occupational defined contribution pension funds seem to dominate the Namibian retirement funding landscape and operate parallel to the State’s universal old-age non-contributory pension scheme. Under defined contribution funds, a retirement benefit guarantee depends on the level of optimisation of investments since members carry the investment risk. Stiglitz and Orszag (1999) states that since the accrual risk rest with members under a defined contribution fund design, the retirement benefit depends on the efficacy with which contributions are managed. Therefore, the relationship between fund efficiency and fund design becomes critical to achieve adequate retirement funding (Boulier, Huang and Taillard, 1999).

According to the Namibian Financial Institutions Supervisory Authority (NAMFISA), many pension funds are becoming dormant and funding levels are dropping (NAMFISA, 2013). This situation is worrying since low funding levels implies solvency and contribution default risk for pension funds (Haberman and Sung, (1994). Under the Pension Funds Act 24 of 1956, pension funds are required to maintain a 100% funding ratio (market value of assets should equal value of liabilities). To mitigate the situation, the proposed Financial Institutions and Markets Bill (FIM Bill, 2014) requires pension funds to identify the various risks and introduce a risk management framework to ensure efficiency. The findings of the study provides a useful analysis on whether a relationship exists between fund risks and efficiency.

Despite the importance of pension funds as seen above, no study in Namibia could be found about the drivers of financial and operational efficiency. Therefore, no guidelines exist on the measurement tools for the performance of pension funds, making it difficult for decision-makers to optimise on scare contributions to provide members with an adequate retirement income. This lack of understanding of determinants of efficiency and performance frontiers of pension funds in Namibia creates a research vacuum for this study.

Against this background, the study aims to analyse and understand drivers of efficiency and contrive strategies to improve performance levels of pension funds to avoid financial catastrophe as witnessed over the last few years with the global economic meltdown which further erodes pension fund values (OECD, 2008).

The study is unique in that it covers an under-investigated area of pension fund management in Namibia and uses Namibian specific data to create an original academic framework and hence contribute to the body of knowledge in the field.

1.1. What Is the Meaning of Efficiency

The term efficiency is used contextually to denote the ability of pension funds to convert inputs (contributions) into outputs (retirement benefit) and hence provide improved values for members (Davis, 2005). As described by OECD, efficiency implies the ability of pension funds to prudently invest contributions and provide members with maximised retirement values on a cost-effective basis based on good governance principles (OECD, 2004, 2008).

1.2. Agency Theory and Pension Funds

Pension funds are managed by a board of trustees consisting of equal representation by the sponsoring employer and employees or members (Pension Funds Act, 1959). The board of trustees have the overall powers to devise benefit structures, receive and invest contributions and appoint service providers. Under the Namibian common law and the FIM Bill (2014), the relationship between the board of trustees and the members is fiduciary in nature and invokes duties of good faith and care in the administration of the affairs of the pension fund. The above description reveals a delegated authority by stakeholders (employer and members) to the board of trustees to take investment decisions on their behalf with a view to receiving a maximised retirement benefit. This principle is consistent with the agency theory which suggests a relationship in which a person engages another to carry out some service on their behalf based on delegated authority (Jensen and Meckling, 1976). Hill and Jones (1992) also confirm this view. Given the fiduciary nature of the agency relationship, board of trustees are required to be prudent and efficient in making investment decisions since members also have legitimate expectations of maximised retirement benefits (Ferrier and Lovell, 1994).

1.3. Theory of Pension Funds as Organisational Systems

Pension funds are conceptualised as organisations under the Namibian Pension Funds Act of 1956 and the Income Tax Act 24 of 1981 and created with the primary purpose of providing retirement savings. In this regard, pension funds collect contributions for savings and investment with a view to providing retirement income to members.

According to the systems theory in management, organisations are regarded as open or closed systems depending on whether they are influenced by the external environment or not (Kast and Rosenzweig, 1972). Therefore, as a participant in the financial services universe, pension funds are influenced by the external environment and hence qualify as open systems as illustrated in figure 1 below. Therefore, similar to other open systems, pension funds have inputs (contributions) that are converted to outputs (retirement benefits) (Njuguna, 2010). This implies optimization of scarce resources (Kumbhakar and Asaftei, 2007). As indicated before, the above systems approach is conceptualised as follows in figure 1:

Fig. 1. Conceptualisation of pension funds as open systems.

Source: Own construction by researcher.

The figure above shows how contributions as inputs are converted into retirement benefits as outputs, following a throughput or conversion process as measured by the opening and closing values of the fund. In other words, the theory measures the extent to which the scarce resources (in the form of contributions) have been converted into retirement benefits for the members.

1.4. Determinants of Efficiency

Based on literature review, efficiency of pension funds is determined by both financial and non-financial variables (Njuguna, 2010), (Bikker and Dreu (2006). The two variables are discussed as follows:

(a) Financial efficiency

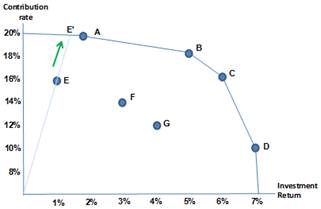

Whilst there are other analytical tools to measure financial efficiency, the majority of previous research in the field of financial services has applied DEA as a more reliable method to test the efficiency of pension funds. DEA is a renowned optimization tool in operations research and applies simple linear programming tools to analyse financial efficiency (Charnes, Cooper and Rhodes, 1978), (Barrientos and Bossofiane, 2005). These tools will analyse the significance of relationships between the variables. The arithmetic basis for DEA is the use of ratios between weighted inputs and outputs (Seiford, Cooper and Zhu, 1990) (Serrano, 2001). The above weighted values are adjusted to between 1% and 100%, the former score being less efficient than the latter (Golany, 1996). The concept of DEA is graphically illustrated as follows in figure 2:

Fig. 2. Basic illustration of DEA

Source: Researcher’s own construct based on Prodtools, 2013.

The diagram in figure 2 above defines a simple illustration of DEA based on imaginary data comprising of a single input and output variables. Based on this illustration, the efficiency scores for pension fund A, B, C and D have created an "efficiency frontier" which the other pension funds E, F and G can improve on by either increasing their output or decreasing their input or by varying both. The repositioning on the efficiency frontier for pension funds E, F and G can only be achieved by either an increase in the contribution rate or the investment return of these funds through for example a change in the investment strategy. Therefore, the efficiency frontier created by pension funds A, B, C and D in the illustration above represents the optimal combination of the inputs, i.e. contributions and net investment returns, required to achieve adequate retirement benefits for members.

Although the illustration in figure 2 above only uses a single input, DEA is also suitable for analysis of multiple outputs and inputs (Charnes, Cooper, & Rhodes, 1978) (Beasley J, 2012). In this study, multiple inputs will be used covering contributions, costs and opening and closing values of Namibian pension funds over the last 5 years.

In Chile, Barrientos and Boussofiane (2005) applied DEA and found that efficiency is also driven by economies of scale. Bikker and Dreu (2006) also supported the above view on efficiency and confirmed that larger pension fund yields better efficiency scores than smaller pension funds. However, Tang (2008) found that in the United States, the design of pension funds also impacted on efficiency levels more than size. The Nigerian experience reveals that investment strategy and cost optimization strategies contributed more to efficiency than other factors (Ezirim, 2008). With the Kenya study Njuguna (2010) applied DEA to measure the financial efficiency of pension funds and contrary to the Chilean experience found that smaller pension funds revealed better efficiency scores than larger funds.

(b) Operational efficiency

Comparative literature review reveals that efficiency cannot only be defined in terms of financial inputs and outputs, but a critical analysis of other attributes is necessary to meaningfully understand the efficiency of organisations (Njuguna, 2010) (Bikker and De Dreu, 2006).

In Bulgaria, the International Monetary Fund defines efficiency in relation to competitive investment rates, price controls, investment performance benchmarking, switching rules (between investment plans) and automatic assignation of undecided participants (default investment options) (IMF Working Paper, 2008).

The OECD defines efficiency in terms of governance (management, regulation and supervision of pension funds), operating costs and fees and pension fund design issues (OECD, 2013), (OECD, 2009), OECD, 2011/13).

The World Bank also supports the OECD views above, and highlights the importance of governance, regulations and risk-based supervision as key attributes to efficiency in pension fund management (World Bank, 2008). According to Impavido (2002), there is a significant positive correlation between governance and investment performance (or efficiency) of pension funds. This view suggest that an improvement in governance practices of the may positively influence the efficiency of pension funds.

At a regional and continental level, the South African National Treasury proposal paper (2012) also defines efficiency in terms of governance, charges and management costs, taxation, net replacement rates and pension fund design issues (National Treasury Papers, 2007/8/9 and 13).

From the above, it is clear that regional and international literature on efficiency offers divergent views on what specific factors to be used in measuring operational efficiency. Therefore, in establishing the appropriate measurement model, the study will use structural equation modelling (SEM) and confirmatory factor analysis (CFA).

SEM is part of a family of statistical tools used to examine the nature of relationships among multiple research constructs and is seen to combine both statistical methods of factor analysis and multiple regression analysis (Hair, Black, Babin, & Anderson, 2010). SEM has an advantage over the other common analytical approaches in that it controls measurement error and bias in analysis that is commonly characteristic of multiple regression methods (Kline, 2005). Whilst CFA looks at the structural inter-relationship among multiple constructs and usually a good starting point in terms of the broader multivariate analysis of data, SEM provides a holistic base for theory testing in correlated and multiple relationships (Hair, Black, Babin, & Anderson, 2010).

Based on the literature review, the study uses multiple variables like governance, regulations, fund risk, fund design, size, age, ethics and investment strategy to measure operational efficiency. To summarise and validate measurement tools, confirmatory factor analysis is used before application of SEM to factorize or determine the structural relationships between the variables (Suhr 2006). These multiple variables based on the literature review forms the theoretical basis for the hypotheses used in this study.

2. Methodology of the Study

The current study is quantitative and deductively grounded on previous studies on application of DEA and SEM as measurement tools for efficiency. Therefore, the study seeks to test the application of an existing theory on efficiency using Namibian data (Leedy, 1997).

The sample

The study sample of 180 participating umbrella pension funds in Namibia was drawn from a data population of about 350 registered participating umbrella pension funds with NAMFISA. This sample covers more than 60% of the occupational private pension fund industry in Namibia and is representative and adequate for the study. Compared to other multivariate methods, SEM usually requires larger sample, but a minimum sample size of a 100 per respondent per model will be adequate for both SEM and DEA in order to achieve sufficient statistical powers (Hair, Black, Babin, & Anderson, 2010). CFA require a sample of 5-20 cases per parameter estimate (Kline, 1998)

The study uses survey data based on questionnaires collected from some 180 trustees with an expected response rate of about 60%. Questionnaires are one of the most widely used data collection technique for large samples for quantitative analysis (Saunders, Lewis and Thornhill, 2007). However, Bell (2005) cautions that questionnaires must be used to collect the precise data necessary to answer a specific research questions in line with the objectives of the research.

Therefore, the questionnaire in this study is based on a five-point Likert-scale from 1 to 5 indicating strong agreement to disagreement on issues around fund ethics, risk, regulations, governance, fund size, age and investment strategy. The questionnaires will be electronically mailed to the respondents.

3. Data Analysis

Financial efficiency for each pension fund will be analysed using financial data for the last 5 years. The study will use DEA to obtain the efficiency scores and determine the level of efficacy for the various pension funds over the period based on weighted inputs and outputs. Data Envelopment Analysis Program (DEAP) Version 2.1 will be used for DEA analysis.

As indicated above, the analysis of operational efficiency uses the various multiple measuring instruments as postulated in the study. CFA assumes normal distribution of data and is used to summarise the important representative factors and confirm validity of the observed variables and create a reliable data structure for SEM (Saunders, Lewis, & Thornhill, 2009). In the above sense, SEM is an extension of factor analysis and multiple regression analysis. Unlike the other multi-variate techniques, SEM is unique in that it can measure multiple dependence relationships at the same time (Hair et al, 2010). Given the multiplicity of dependence relationships to be measured based on the literature review, it is appropriate to use SEM as a reliable optimisation tool of analysis for this study.

CFA creates a pre-conceived factor structure to test hypotheses and allow SEM to statistically test the significance of relationships amongst and between the variables (Truxillo 2003). Based on the foregoing, it is evident that CFA becomes a critical analytical process before application of SEM. Various statistical tests will be used to determine the adequacy of model fit to the data before application of SEM and this include the chi-square test to indicate the amount of difference between the observed and expected covariance matrices. A value close to zero indicates little difference whilst the probability level must be greater than 0.05 when chi-square is close to zero (Hair, Black, Babin and Anderson, 2010).

The study uses STATISTICA and LISREL software package to aid analysis of data. These are the common software packages used for this kind of studies (Hair et al, 2010).

4. Importance of Expected Results

The expected results of the study provide important insights into the determinants of efficiency and suggest effective ways to improve the performance of pension funds in Namibia. The overwhelming literature review shows that larger pension funds are expected to yield better efficiency scores (Barrientos and Boussofiane, 2005). This implies that economies of scale have a direct relationship to the efficiency of pension funds. Pension funds in Namibia are relatively small and sponsored by employers from the small and medium enterprises. Therefore, it will be important to find out how efficient these pension funds are and whether the size of pension funds really impacts on efficiency in Namibia.

The literature has also shown that benefit design has an influence on pension fund efficiency. The literature consulted indicates that defined contributions (DC) funds are more efficient than defined benefit (DB) funds (Tang and Mitchell, 2008). The vast majority of pension funds in Namibia are structured on a DC basis and it will be useful to know whether these schemes are relatively efficient than the few DB schemes in Namibia. Over the last few years, the world has seen a massive conversion from DB to DC and it will be important to know whether benefit design affects efficiency levels of pension funds in Namibia.

Namibia has unfavourable demographic profile and a relatively low coverage rate. Therefore, the average pension fund has small memberships ranging from 50 to a 100 members (NAMFISA, 2013). Therefore, the issue of membership age and fund size is absolutely critical from a planning and efficient management of scarce resources. The comparative literature has revealed that larger pension funds (in terms of membership and assets under management) have diverse investment choices and carry more risk than smaller funds making them less efficient (Bikker and Dreu 2009). It will be interesting to see the findings on the Namibian specific situation to allow improved management decisions.

Life-stage investing is the new phenomenon in Namibia implying that pension funds with older members tends to invest in less riskier assets than funds with younger age profile who invest in more aggressive portfolios and earning better returns over the medium to long-term (NAMFISA, 2013). The concept of life-stage investing derives from the theory of life cycle investing in terms of which fund investments are aligned to the age demographic profile of the fund (Bodie, 2003). Therefore, the findings of the study around the significance of the relationship between age, size and investment returns will help improve decisions around investment strategy and efficient allocation of resources.

With globalisation, standards of governance have become universal and Namibia as a member of various multi-lateral agencies like the United Nations have committed to observing high ethical standards in all dealings. The pension fund industry as an important catalyst of socio-economic growth have not escaped unscathed and is required to comply with these global standards. Therefore, it is very important to determine the extent to which pension funds comply with governance and regulatory standards and whether the same impacts on the ability of pension funds to be efficient. This will be an important consideration in managerial decision-making.

With a weaker global economic outlook and a series of repeated incidents of economic collapse of many countries, it becomes imperative to institute risk management strategies. Economic recessions increase the risk of sponsoring employer’s defaults on contributions to the pension fund, stock market collapse and overall ability of pension funds to be liquid and pay promised retirement benefits. This places a great onus on the board of trustees to implement a risk management strategy. It is not clear whether managing this risk is in any way impacting on the efficiency of pension fund and the findings of the study provides some useful insight.

The significance of the relationship between financial and operational efficiency further highlights the importance of taking both financial and non-financial considerations in every aspect of decision-making in pension fund management. The outcome of the study empowers trustees to develop financial and operational guidelines to help with efficient management of pension funds in general.

5. Conclusion

The study is dedicated to the measurement of efficiency in the management of pension funds in Namibia. It is shown from the analysis of comparative literature review that various factors have an influence on the efficiency of pension funds. The study will factorize these variables using CFA as part of the SEM strategy to investigate the significance of relations between them. The balance of the empirical literature also seems to applaud the use of DEA as a reliable tool to measure financial efficiency given the weights of inputs and outputs in the model.

Lastly, the paper briefly highlights the importance of the expected results and implications of the study for managerial practice and policy formulation.

References

- Bateman H. & Piggot J. (1997). Mandatory retirement saving: "Australia and Malaysia compared", Salvador Valdes-Prieto, The economics of pensions: Principles, policies and international experience (Cambridge University Press, 1997)

- Barrientos, A., & Boussofiane, A. (2005). How efficient are pension funds in Chile? Revista de Economia Contemporanea (2) , pp. 289 - 311.

- Beasley J, E. (2012, July 9). OR Notes. Retrieved June 02, 2013, from OR Notes: http://people.brunel.ac.uk/~mastjjb/jeb/or/dea.html

- Bell, J. (2005). Doing your Research Project (4th edition), buckingham, Open University Press.

- Bikker, J., & Dreu, J,. 2009. Operating Costs of Pension Funds: The impact of scale, governance and plan design. Journal of Pension Economics and Finance. (8)63-89.

- Bikker, d. D. (2006). Pension Fund Efficiency: the imapct of scale, governance and plan design. Amsterdam: De Nederlandsche Bank.

- Bodie, Z. (2003). Thoughts on the future life-cycle investing in theory and practice. Financial Analyst Journal Vol. 59

- Boulier, J., Huang S., Taillard G. (1999), Optimal Management under stochastic interest rates: the case of a protected defined contribution pension fund. Insurance, Mathematics and Economics Journal, vol. 28, pg 173-189

- Charnes, A., Cooper, W. & Rhodes, E. 1978. Measuring the efficiency of decision-making units. European Journal of Operation Research. (2):429-44.

- Davis, E. (2005). The role of pension funds as institutional investors in emerging market economies. Korea: Korea Development Institute Conference.

- Devereux, E. (2001). Social Pension in Namibia and South Africa. World Bank Press

- Ezirim, C. (2008). Survey of Investmet Strategies and Efficiency of Financial Institutions in Nigeria. The lcfal Journal of Applied Economics .

- Ferrier, G., & Lovell, C. (1994). Measuring cost efficiency in banking : econometric and linear programming evidence. Journal of Econometrics, Volume 46 , 229 - 245.

- Financial Institutions and Markets Bill 2014

- Frontier Analyst Version 4.10. 2005. Baxia Software Ltd. [Online] Available: www.baxia.com.

- Golany B, B. (1996). Using Rank Statistics for Determining Programmatic Efficiency Differences In Data Envelopment Analysis. Management Science , 466-472.

- Hair, J., Anderson, R., Tatham, W. & Black, C. 1995. Multivariate Data Analysis with Readings. Engelwood Cliffs. Prentice Hall.

- Haberman, S. & Sung J. (1994) Dynamic approaches to pension funding, Insurance, Mathematics and Economics Journal Vol 15, Pgs 151-162

- Hassan, H. O. (2008). Developing a broad-based employee pension scheme for Botswana. Johannesburg, South Africa: Genetics Analytics.

- Hill, J. & Jones, T.M. (1992). Staleholder-Agency Theory. Journal of management Studies 29:2

- Holzmann R. (2000). The World Bank Approach to Pension Reform. Journal of Social Security Review. Vol 53 Pages 11-34

- Hu, Y., Stewart F. & Yermo J. 2007. Pension Fund Investment and Regulation: An International Perspective and Implications for China’s Pension System. OECD/IOPS Global Private Pensions Forum. Beijing. November pp.14-15.

- Impavido G. (2002). Efficiency and Performance of the Bulgarian Private Pensions. IMF Working Paper WP 08/268

- Income Tax Act 24 of 1981

- Jablonsky, J. (2005). Measuring Efficiency of Production Units by AAP Models.

- Jensen, M & Meckling, W. H. (1976). Theory of the firm: managerial behaviour, agency costs, and ownership structure. Journal of Financial Economics, 3, 305-60

- Kast, F. & Rosenzweg, J. (1972) General Systems Theory: Applications for Organisation and Management, University of Washington

- Kline, R.B. (1998) Principles and Practice of Structural Equation Modeling. New York, The Guilford Press.

- Kumbhakar, S. C., & Asaftei, G. (2007). Regulation and efficiency in transition: the case of Romanian Banks. Springer Science and Business Media , 1-2.

- NAMFISA Annual Reports 201

- OECD. 2008. Global Financial Crisis Hit Pension Fund Assets by 20%. OECD Publishing. Paris.

- OECD. (2009). Pensions at a Glance: Retirement Income Systems in OECD Countries. OECD Publishing.

- OECD. (2013). Pensions at a Glance: Retirement Income Systems in OECD Countries. OECD Publishing.

- OECD. (2011). Pension Fund Operating Costs and Fees in Pension at a Glance 2011: Retirement Income Systems in OECD and G20 Countries. OECD Publishing.

- Saunders, Lewis, & Thornhill. (2009). Research Methods for Business Students. Prentice Hall.

- Seiford, l., Cooper, L., & Zhu, J. (1990). Data Envelopment Analysis. Journal of Eonometrics .

- Serrano, C. & Mar Molinero M. 2001: Selecting DEA specifications. ranking units via PCA. Discussion Papers in Management, M01-3, University of Southampton.

- Shiimi. I. & Kadhikwa G.1999, Savings and Investment in Namibia. BON Occasional Paper No. 2

- SA National Treasury. (2007). Social Security and Retirement Reform. Retrieved from http://www.treasury.gov.za

- SA National Treasury. (2008). Retirement Fund Reforms. Retrieved from http://www.treasury.gov.za

- SA National Treasury. (2009). Retirement Fund Reform. Retrieved from http://www.treasury.gov.za

- SA National Treasury. (2013). Retirement Fund Reforms. Retrieved from http://www.treasury.gov.za

- STATISTICA Version 9.0. 2009. StatSoft Incorporated. [Online] Available: www.statsoft.com.

- Stewart, F. & Yermo J. 2008. Pension Fund Governance: Challenges and Potential Solutions. OECD Publishing.

- Stiglitz, J. (1999). Rethinking Pension Reform: Ten Myths about Social Security Systems.

- Stock, & Sherbourne. (2004). Namibia Stock Exchange and Domestic Asset Requirements: Options for the future. Windhoek: NEPRU.

- Subbarao. (1998). Namibia's Social Safety Net: Issues and Options for Reform.

- Tang, M. (2008). The Efficiency of Pension Plan Investment Menus: Invesment Choices in Defined Contribution Pension Plans. Michigan: University of Michigan.

- Truxillo, Catherine (2003) Multivariate Statistical Methods: Practical Research Applications Course Notes. Cary N.C. SAS Institute.

- World Bank. (1994). Averting the Old Age Crisis: Policies to protect the old or promote growth. Oxford Press

- World Bank (2014). Report entitled "The inverting Pyramid: Pension System Facing Demographic Challenges in Europea and central Asia".