Journal of Agricultural Science and Engineering, Vol. 2, No. 6, December 2016 Publish Date: Nov. 12, 2016 Pages: 46-56

Recent Changes in Local Marketing Patterns of Gum arabic in Kordofan, Sudan

Tarig E. M.1, Abdelateif H. I.3, *, Mohamed E. T.1, Awad Elkarim S. O. K.2, Hassan E. A.2, Pretzsch J.4, Auch E.4, Mohamed Elmustafa O. E.1,

Hatim M. E.2, Osman E. A.2, Zeinab M. H.2, Muneer E. S.2, Mohamed E. E.2, Fathi H. B.1, Asmamaw A. A.5, Elbasha B.1

1Faculty of Natural Resources & Environmental Studies, University of Kordofan, Elobeid, Sudan

2Institute of Gum arabic Research & Desertification Studies, University of Kordofan, Elobeid, Sudan

3Department of Agricultural Economics, Faculty of Agriculture, University of Khartoum, Khartoum, Sudan

4Institute of International Forestry and Forest Products, Technische Universität, Dresden, Germany

5Department of Natural Resources Management, University of Gondar, Gondar, Ethiopia

Abstract

The paper described the recent changes in local marketing patterns of Gum arabic in Kordofan, Sudan. The study depended heavily on secondary data sources including market records and documents. Primary data were collected via structured questionnaires based on stratified random sampling technique. A set of research tools encompassing descriptive statistics, linear regression and Kurskal - Wallis Test were used. The findings revealed that local marketing patterns of Gum arabic at central, urban and rural levels have experienced several changes throughout the investigated period. The infrastructures, services and market information were subjected to significant (P ≤ 0.01) improvements, particularly at the central markets (e.g. Elobeid and Enuhud). The trend with regard to of number of the Gum arabic stakeholders at Elobeid Central Crops Market expressed different tendencies; number of registered companies revealed slight increase (R2 = 0.38), number of traders showed sharp decline (R2 = 0.51) and number of producers' agents remained unchanged. By this, the market seems to favor more existence of downstream stakeholders than upper stream ones. Concerning Gum arabic prices at Elobeid Crops Market (2000-2015), a sharp increase (R2 = 0.66) encountered by using nominal market price based on local currency (SDG), while a moderate increase (R2 = 0.29) prevailed when using shadow exchange rate based on foreign currency (US$). On the other hand, the price of the commodity at Enuhud Crops Market (2003-2015) demonstrated an overall increasing trend (R2 = 0.86) at local currency. Setting of Gum arabic prices at rural, urban and central markets showed different scenarios of pricing mechanisms including compromising between sellers and buyers, real auctioning, and determination of prices solely by buyers. The market fees and taxes per quintal resulted in significant differences (P≤ 0.01) between central, urban and rural markets. With regard to post harvest, handling and quality aspects, the findings indicated that some progress has been realized recently in central markets particularly in using electronic balances, start adopting certification process and improving grading and packing procedures. The paper was concluded with some frameworks, which might play a major a role in market reforms.

Keywords

Gum arabic, North Kordofan, Stakeholders, Infrastructure, Prices, Market information

Received: October 7, 2016

Accepted: October 25, 2016

Published online: November 12, 2016

@ 2016 The Authors. Published by American Institute of Science. This Open Access article is under the CC BY license. http://creativecommons.org/licenses/by/4.0/

Contents

1. Introduction 2. Methodology 2.1. Study Area 2.2. Data Collection 3. Results and Discussion 3.1. Description of Crops Markets Patterns in Kordofan 3.2. Recent Changes in Gum arabic Stakeholders at Elobeid Crops Market 3.3. Recent Changes in Gum arabic Prices at Elobeid Crops Market 3.4. Recent Changes in Gum arabic Quantities at Elobeid Crops Market 3.5. Recent Changes in Gum arabic Quantities and Prices at Enuhud Crops Market 3.6. Income and Quantities Across Different Gum arabic Markets 3.7. Prices and Pricing Mechanisms 3.8. Market Fees, Taxes, Duties and Commissions 3.9. Post Harvest, Handling and Quality Aspects 3.10. Market Information System 3.11. Gum arabic Marketing Constraints 4. Conclusion and Recommendations Acknowledgement

1. Introduction

Gum arabic is one of the Sudan’s most important non-wood forest products (NWFPs), in which the country has recently provided (71%) to the global market [11]. Producers of this commodity are scattered over widespread areas in the gum-belt across Sudan that justifies presence of a large numbers of market's stakeholders throughout its value chain [2, 3]. Tapping and collection activities of the Gum arabic product, in most cases, are concentrated in remote areas [12], which substantiate transportation facility from production to marketing sites. Seasonality of Gum arabic production is one of the most important factors which structure its marketing forces in Sudan. Unfavourable environmental conditions, coupled with market imperfections, commonly affect supply of Gum arabic commodity to the marketing sites [8]. Risk and uncertainty are common features that affect both Gum arabic production and prices [8]. Despite the burden of price distortion and the successive policy interventions, the commodity always shows different levels of comparative advantage and market competitiveness [7]. Yet, Gum arabic sub-sector is confronted with some environmental, socioeconomic and institutional problems impinge on the structure of its whole value chain in the country [14]. The local marketing system of Gum arabic in Sudan is very difficult and complex [7]. In view of that, the rural traditional market is argued to have a damaging effect that underestimates the producer’s prices below a reasonable level [8]. Less stakeholders often exist at assembly markets, which receives Gum arabic commodity from domestic markets. Being a higher level market located at urban centers, a wholesale market gets Gum arabic supplies from both domestic and assembly markets. Central markets are located in the big cities. Many traders preferentially sell their Gum arabic commodity outside the auction markets due to many factors including lower rates of taxes and fees imposed on crops, lesser bureaucracy and routine resulting in high profit margins obtained at these markets [11]. Historically, the price mechanism of Gum arabic commodity at the auction markets was fully dependent on the minimum floor price mainly determined by the Federal Ministry of Commerce [5]. Accordingly, the producers were supposed to be protected because the floor price was considered to be the start bidding price for Gum arabic commodity at the auction market [5, 6].

The present paper is aimed to investigate the recent changes in Gum arabic local marketing patterns in Kordofan region as far as the Gum arabic commodity moves from rural through urban to central markets. This was performed though addressing changes in market infrastructures, services, stakeholders, market forces, taxes and fees, pricing mechanisms, information systems and some quality aspects.

Following this section, the remainder of the paper is organized as follows; section 2 presents the sample area, data collection and the methods employed, section 3 discusses the empirical results of descriptive statistics, recent changes in Gum arabic markets, prices, and quantities; section 4 concludes the study.

2. Methodology

2.1. Study Area

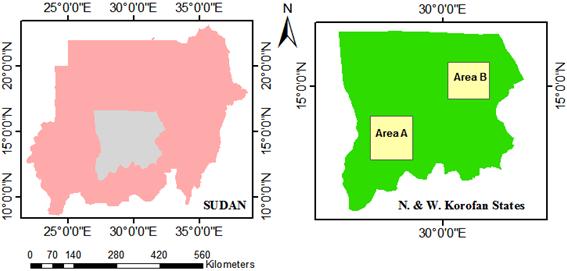

The study was conducted in North Kordofan (A) and West Kordofan (B) States which are located within the semi-arid zone of central Sudan between latitudes 9° 30' and 16° 24' N and longitudes 27° to 32° E. The region is characterized as one of the most vulnerable areas in the country concerning desertification processes. The two areas are located at the heart of the Gum arabic belt. Area (A) lies in the north-east part covering an area of 110483 ha, while area (B) is found in the south-west part of the Gum arabic belt covering an area of 153722 ha (Figure 1). Both sites are located in the Sahel zone, which refers to an ecological zone situated between the Sahara to the north and the Sahel zone to the south [1]. The mean annual temperature varies between 28° and 30°C. The coldest months are December and January with mean temperatures of 14.1°C and 13.5°C, respectively, and the hottest months are April, May and June with an average mean temperature exceeding 30°C [10, 12]. The rainy season extends from June to October with the highest rains in August. Average rainfall estimated is 250 - 400 mm. The main economic activities are rain-fed agriculture and livestock herding. The community constitutes rural (50%), urban (34%) and nomads (16%) with an annual growth rate of 1.45% [9].

2.2. Data Collection

Data necessary for achieving the study objectives were obtained from primary and secondary sources through a combination of qualitative and quantitative collection tools. The primary data were collected based on stratified random sampling technique via a questionnaire designed and distributed randomly to 75 respondents from four markets. These markets comprise rural (Kasgail), (Errahad) and central (Elobeid and Enuhud) levels. Furthermore, focus group discussions (FGDs) with key- informants from administrative units of the selected markets were conducted. The secondary data were heavily depended on market records and documents. These include time series data with regard to Gum arabic sold quantities and their corresponding minimum, maximum and average prices. Other quantitative data encompassed a number of active stakeholders, taxes, fees and duties. Moreover, the information comprised qualitative data in terms of status of infrastructures, services, some quality aspects, administrative setups and market information systems. The data were analyzed by using a set of research tools including descriptive statistical analysis, regression and correlation analysis.

Figure 1. Map of the study area.

3. Results and Discussion

3.1. Description of Crops Markets Patterns in Kordofan

Gum arabic markets in Kordofan were described according to some recent literatures [7, 2] into various types. Domestic or rural traditional markets positioned at the upper stream level of the Gum arabic value chain. Rural markets are considered as places for social and cultural forum for local communities; they comprise small producers and village merchants and operate in most cases one-day a week market basis. The rural market is generally administered by a local committee from the rural village council in common with the administrative officer and executive body of cashiers, market foremen and guards. Commonly, the market areas are small and mostly unfenced without any administrative buildings. Gum arabic commodity is displayed in irregular manner at shades made out of crop sticks and dried hay. Examples for some potential rural markets with regard to Gum arabic commodity in Kordofan are Iyal Baheit, Umgafla and Kasgail.

The assembly markets, receive Gum arabic commodity from rural markets and they encompass village merchants, middlemen and city merchants. Most of these markets are located nearby Gum arabic potential areas of supply. Hierarchically, they are positioned at the first quarter of the upper stream of Gum arabic local marketing value chain. In terms of marketing dynamics they are found in between the rural and wholesale or central markets. They are often administered by market executive committees under the localities’ administrations. Assembly markets are to some extent, more organized compared to rural markets and operated on daily basis. Infrastructures in most cases include fenced market yards, some offices for administrative units, conventional balances and others. Examples for some important assembly markets in Kordofan are Ghibeish, Elkheuei and Errahad. Wholesale markets in Kordofan receive Gum arabic supplies from both domestic and assembly markets. They are located at urban areas. Um Ruwaba, Bara and Abu Zabad are typical examples denoting wholesale markets. Central markets, where Gum arabic commodity is sold in and outside auction markets are located in main cities. Auction markets are organized by local government authorities as part of gum marketing system. Gum arabic is brought by producers’ agents or merchants to special yard or shed and sold by auction to buyers. In auction markets both sellers and buyers come under one roof and Gum arabic is auctioned by government clerks.

Elobeid and Enuhud crops markets are considered the largest auction markets in Sudan, while other important central markets are located in Damazin, Sinnar, Gadarif and Port Sudan. Auction yards are managed by local authorities. The Gum arabic local marketing deals with two main categories namely raw and processed Gum arabic which are found in four grades; Hand- Picked-Selected (HPS), Cleaned, Dust and Kibbled. At present, the Ministry of Finance and Economy in North and West Kordofan States used to be responsible for technical management of crops markets whereas; the market assets and manpower structure are directed by localities.

The Gum arabic in Kordofan is principally produced by small-scale farmers who give priority to production of food and cash crops (usually sorghum, millet, groundnuts, sesame and water melon seeds) to secure family nutritional needs and to obtain other sources of income. According to the reviewed literature [4], it is clear that this situation was kept true for long time and the small scale farmers are still the main producers of gum despite the entrance of few large scale enterprises (e.g. Acacia Company) that come recently to this field. The small scale farmers obtain informal credits through Sheil system in most cases from local village merchants: normally, the credit repayment-ability is made on kind basis inform of Gum arabic commodity [7, 13]. Some telling arguments [3, 7] revealed that local marketing of Gum arabic in Kordofan has been structured by the monopoly monopsony power of the Gum arabic Company (GAC) as a sole buyer and exporter of raw Gum arabic in Sudan since 1969 to 2009. Every year, two months before tapping starts, the Ministry of Foreign Trade (MFT) announces the floor price. According to interviews with stakeholders at Elobeid Crops Market, the floor price setting was not based on the export price of the Gum arabic commodity. It was also clear that when Gum arabic is not sold or not offered the floor price at auction, the GAC has the obligation to procure at the floor price.

Other Gum arabic marketing patterns were tackled from different viewpoints including market stakeholders, market forces (supply and demand), prices and pricing mechanisms, fees, taxes and local duties, quality aspects, market information and marketing constraints.

3.2. Recent Changes in Gum arabic Stakeholders at Elobeid Crops Market

The number of active stakeholders at Elobeid Crops Market is displayed in Figure (2) and Figure (3). Regarding the number of registered companies and producers' agents during the period (2000- 2015), results are presented in Figure (2). A remarkable fluctuation in the pattern of registered companies is indicated. In this context the number of the companies was high during 2008, drastically decreased in 2009, and sharply increased till 2012; recently, the number showed slight decline. The overall trend of the Gum arabic companies revealed slight increase (R2 = 0.38) for the whole investigated period. On the other hand, a noticeable fluctuation in the pattern of registered producer' agents is expressed in the same Figure (2). In view of that the number of the producer' agents was high during 2008, drastically decreased in 2009, remained to some extent steady during the period from 2010-2012 and moderately increased in the recent years (2013-2015). The overall trend of Gum arabic producers' agents at Elobeid Crops Market remained steady (R2 = 0.009) for the whole investigated period. The reason for the sharp decrease in both traders and companies during the first investigated period (2008-2009) was mainly attributed to the recession in Gum arabic trade that enforced the national authorities to issue the Gum arabic Trade Liberalization Polices [11]. At the expense of that, the concession power of Gum arabic company, which is a government sponsored company, was dismantled. Thereafter, many companies and producers' agents have emerged. The ongoing results (Figure 3) also revealed that the number of registered traders at Elobeid Crops Market moderately decreased during the investigated period from 2005 to 2008, slightly increased in 2009 and decreased once again from 2010 to 2015.

The overall trend of Gum arabic traders showed sharp decline (R2 = 0.51). This is presumably attributed to some factors among which is the disfavoring Gum arabic prices offered at the auction market, lack of credit facilities, high taxes and fees and fluctuation in Gum arabic supplied to the market. To conclude, it is clear that Gum arabic producers do not exist at the central markets, which in favors existence and increase of downstream stakeholders like (big Gum arabic companies) more than upper stream ones (e.g. traders).

Figure 2. Number of registerd companies and producers' agents at Elobeid Crops Market (2008-2015).

Figure 3. Number of registered traders at Elobeid Crops Market (2005-2015).

3.3. Recent Changes in Gum arabic Prices at Elobeid Crops Market

The Gum arabic prices obtained from Elobeid Crops Market for last 15 years is displayed in Figure (4). The pattern showed slight increase in the first five years followed by a sharp decrease during 2005-2006 before a short stability occurred till the year ending 2009. Then prices increased vigorously after the abolition of Gum arabic Company (GAC) concession (2010-2015). Generally, the price trend expressed a sharp increase (R2 = 0.66) due to the nominal inflated prices as mentioned before. Therefore, the same price pattern was reanalyzed in US$ using shadow exchange rate (SER) as depicted in Figure (5) to provide logical framework. Accordingly, the price trend revealed moderate increase (R2 = 0.29) for the whole period.

Figure 4. Gum arabic prices per quintal in SDG** at Elobeid Crops Market (2000-2015).

Figure 5. Gum arabic prices per quintal in US$ using SER at Elobeid Crops Market (2000-2015).

3.4. Recent Changes in Gum arabic Quantities at Elobeid Crops Market

The pattern of Gum arabic quantities at Elobeid Crops Market as expressed in Figure (6) showed sharp increase in 2001, remarkable decrease in 2004 and undulating pattern from 2005 to 2015. The quantities of Gum arabic for the whole period demonstrated a slightly declining trend (R2 = 0.004).

Figure 6. Gum arabic quantities at Elobeid Crops Market (2000-2015).

3.5. Recent Changes in Gum arabic Quantities and Prices at Enuhud Crops Market

The quantities of Gum arabic supply at Enuhud Crops Market during the last two decades are shown in Figure (7). They expressed substantial increase from 2003 up to 2008, reaching the lowest level in 2009. The market quantities increased once again in to reach the peak level in 2011. However, the recent period (2012-2015) indicated sharp decline in the Gum arabic quantities to the central market. Generally, the Gum arabic supply to Enuhud Crops Market is characterized by irregular [1] fluctuating pattern expressed in a slightly increasing trend (R2=0.20). This could be explained by the following reasons; presence of Dabei rural market adjacent to the Enuhud Crops Market through which most of market transactions and activities (price bargaining, commodity inspection, cleaning, sorting, grading, and storing) take place. In addition, imposition of high market fees, taxes and Alms (Zakat), curtail market incentives and push auction market towards unrealistic manner. The prices of the Gum arabic commodity at Enuhud crop market (2003-2015), showed an overall increasing trend (R2= 0.86). Under this context the prices pattern was to some extent stable for the first period (2003-2009) fallowed by steady increase in gum prices for the recent period (2009 upwards). This is mainly due to; implementation of Gum arabic trade liberalization policies which have improved the nominal prices and the devaluation of the local currency which has led to inflated prices.

Figure 7. Quantities and prices of Gum arabic at Enuhud Crops Market.

3.6. Income and Quantities Across Different Gum arabic Markets

Incomes generated from sales of Gum arabic in the study areas were expressed in Table 1. It is obvious; the stakeholders at Elobeid central market receive relatively high income compared to stakeholders from Errahad urban market and Kasgail rural market. The same trend is valid with regard to the Gum arabic quantities supplied to the three mentioned markets. The Kurskal-Wallis test showed significant differences (![]() = 10.14*** and 23.73**) between annual income and quantities of Gum arabic supplied to the three markets, respectively. This is mainly attributed to the fact that stakeholders at central markets are mainly big traders, companies or companies’ agents dealing with big lots of Gum arabic transactions compared to stakeholders at rural (village traders) and urban markets (small city merchants). The results also imply that stakeholders from both Elobeid and Kasgail crops markets are more likely involved in Gum arabic activities in comparison to those from Errahad market.

= 10.14*** and 23.73**) between annual income and quantities of Gum arabic supplied to the three markets, respectively. This is mainly attributed to the fact that stakeholders at central markets are mainly big traders, companies or companies’ agents dealing with big lots of Gum arabic transactions compared to stakeholders at rural (village traders) and urban markets (small city merchants). The results also imply that stakeholders from both Elobeid and Kasgail crops markets are more likely involved in Gum arabic activities in comparison to those from Errahad market.

Table 1. Income and supplied quantities of Gum arabic in the selected markets.

*** indicates significant level of 1%.

3.7. Prices and Pricing Mechanisms

The comparative results of price setup in Gum arabic markets between 2004 and 2015 showed some differences as presented in Table 2. A considerable proportion of respondents (35%) mentioned that the price was determined by the buyers in the year 2004. In the year 2015, 37.4%of interviewees stated that the price was setup according the real auction market and the same percentage of respondents advocated attitude of compromising between sellers and buyers. It is worth mentioning that in both years the sellers (producers) have the lowest bargaining power with regard to the Gum arabic price setup.

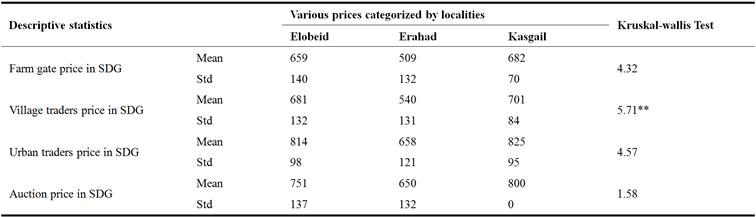

Concerning the price of Gum arabic in the selected markets, the results revealed that there is high significant variations at (P= 0.01) between village's traders; this might be attributed to the small quantities of gum sold in such market. On other hand, no significant variations were reported as far as farm gate prices, urban traders’ prices and auctioning prices are concerned Table 3.

Table 2. Mechanisms for Gum arabic price setups (2004 and 2015).

Table 3. Price of Gum arabic in the selected markets.

** indicates significant level of 5%.

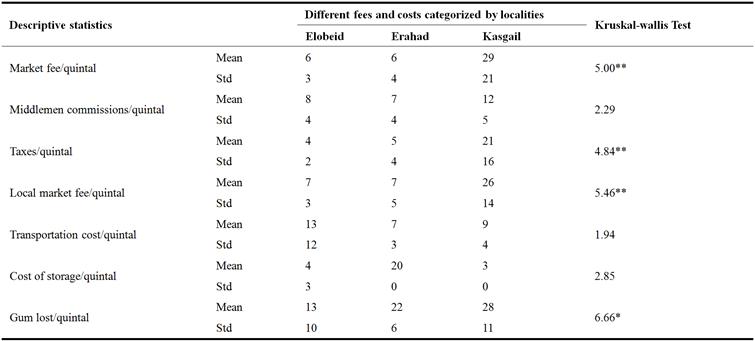

3.8. Market Fees, Taxes, Duties and Commissions

There are no fees, taxes, duties or commissions paid on Gum arabic in the production sites, therefore all such royalties are collected in markets [14]. They are of two types: In case of Gum arabic "with documents", that mean the producer has already paid the expenses. However Gum arabic "without documents" indicate that the producer did not pay any fees and taxes on his product and the trader who buys the commodity will be responsible for that. The alms on Gum arabic identified are: Zakat, Local Council Duties, Forest National Corporation (FNC) fees, Elobeid Crops Market (service fees on Gum arabic) and State Duty Stamp [7, 14]. The Local Council (locally known as Mahalia) in Elobeid, usually receives the so-called Mahalia fees (locality duties) equivalent to 25 SDG/sack (slightly more than two $ dollar based on SER) from traders who sell their products in the central markets. The beneficiaries from the locality fees include the local council and locality services. The alms authority is responsible for collecting the Zakat fees in all markets (village markets, weekly markets and central markets). The amount collected is equivalent to 10% of the value of the product in cash or in kind. The Zakat fees are of federal nature paid according to the Federal Law of 1993, amended in 2006 and later in 2011; the beneficiary groups according to Quran Doctrine should be poor people and other targeted groups and services. The Forests National Corporation (FNC) fee is of federal nature paid in cash to FNC by collectors/producers and traders of Gum arabic according to the 1989 Forest Law. This fee differs in amount from a year to another. With respect to the Elobeid Crops Market, the service unit is responsible for collecting fees on Gum arabic. Such fees are used for provision of services in the market, besides 1% of the fee that goes to the Farmers’ Union and 4% to the State Ministry of Finance and Economy. Market fees have been imposed by the state authorities to compensate for the abolished taxes and fees on Gum arabic. In addition to taxes and fees of federal nature, there are other taxes at state and locality levels which are subjected to duplication and mistiming sometimes [7, 9]. Like all other non-wood forest products, the payments imposed on Gum arabic are compound and not consistent and of changing amount from year to year. Additionally, other types of costs on quintal bases have been identified to include middlemen commissions, storage and transportation costs as categorized by some localities in Kordofan.

Table 4. Market taxes and fees / SDG in central, urban and rural crops markets.

3.9. Post Harvest, Handling and Quality Aspects

According to personal observations and the key informant interviews made by the study team at Elobeid and Enuhud crops markets, Gum arabic commodity in most cases is provided to the market in plastic sack, where the buyer repacks it in a jute sack hence the plastic one has adverse effects on the quality of the product. Conventional balances are still used for weighing Gum arabic in rural and urban markets, whereas both conventional and big electronic balances (Tornatas) are also used in Elobeid and Enuhud crops markets. It is worth to mention that conventional and electronic balances are subjected to regular calibration by the official authorities. Loading and offloading of the commodity are done manually by casual labor. No storage facility inside the market is offered and the product is only covered with a polyethylene plaster for three days at maximum. The grading of the Gum arabic commodity is made by highly skilled women at the company warehouses. Accordingly, the product is categorized into different grades (hand pick selected H.P.S., cleaned, dust after removing the impurities (park, sand). Recently (2016), a dry port-exit has been established in Elobeid city to facilitate the quality standards, custom duties and other export documents. Sudanese Standards and Metrology Organization (SSMO) office takes product samples for determination of physiochemical properties for the export purposes. According to importer's preference, the export enterprises either pack the product (HPS) in 25 or 50 kg or process it in different forms (kibbled or powder gums).

3.10. Market Information System

Results on market records and information system are displayed in Table 5 in which secondary obtained from [8] were merged with primary data collected in 2015 for the purpose of this study. Remarkable changes have been noticed during the specified period 2004 to 2015. In 2004, the majority (73%) of respondent's advocated absence of records in the markets compared to 35% in 2015. Concerning use of book keeping, the results revealed 27% and 50% of respondents in the years 2004 and 2015 respectively. Although there was no use and application of electronic system in 2004, recently, in 2015, about 15% of the stakeholders use electronic devices (computers, mobiles, screens and websites) in marketing purposes.

Table 5. Availability and type of market records across the investigated crops markets.

3.11. Gum arabic Marketing Constraints

Regarding the constraint confronting marketing of Gum arabic, some changes have been identified during the period 2004 to 2015. For instance, the effects of logistics problem (transportation and storage facilities) decreased according to viewpoints of respondent from 22% in 2004 to 14.7% in 2015. The security unrest was a problem for 5% of respondents in 2004 and improved in 2015 to be problem for only 1% of respondents. Percentage of interviewed who bring meager quantities of Gum arabic decreased from 15% to 6.7%, according to view points of respondents in concern. Taxes and customs represented a real problem for 35% in 2004 while it declined to be a problem for 17.3% in 2015 (Figure 8). Some positive changes indicated in these results could be attributed to promotion in the marketing system of Gum arabic; however the situation still needs interventions for further improvements.

Figure 8. Constraints of Gum arabic marketing from view of respondents (2004 and 2015).

4. Conclusion and Recommendations

The current study provided strong argument about recent changes in Gum arabic local marketing patterns of in Kordofan, Sudan. In this context, remarkable changes were undergone with regard to infrastructures, services and market information systems at central markets rather than urban and rural ones. The numbers of registered stakeholders were unstable and most likely decreased across the two investigated central markets (Elobeid and Enuhud). The trends of Gum arabic market prices were found increasing sharply by using local currency (SDG) and slightly increasing if shadow exchange rate based on US dollar is considered. Pricing mechanisms prevailed at these markets have been largely determined through compromised-agreement between sellers and buyers, real auctioning, and to a great extent by buyers alone. The market fees and taxes vary significantly between central, urban and rural markets. Some progress has been achieved with regard to Gum arabic post harvest, handling and quality aspects, particularly at central markets. Based on the obtained results, more attention should be devoted to infrastructures and services particularly at rural markets. The pricing mechanisms at urban and central markets should be pushed towards more realistic auction market.

Acknowledgement

The authors acknowledge the financial and technical support for conduction and publication of this research provided by CHAINS Project (Chances in Sustainability-Promoting Natural Resource Based Product Chains in East Africa, funded by the German Federal Ministry of Education and Research (BMBF) under the project-ID 01DG13017. The responsibility for the contents of this publication is with the authors.

References

- Adam, H. E. (2011). Integration of remote sensing and GIS in studying vegetation trends and conditions in the Gum arabic belt in North Kordofan, Sudan, Berliner Verlag, Germany, ISBN 978-3-941216-58-7.

- Ballal M. E. (2011). Formulating a strategy for production, value addition and marketing of WFPs from arid and semi-arid lands (ASAL) in Sudan. Report for IGAD.

- Couteaudier, T. Y. (2007). Export marketing of Sudanese Gum arabic, multi donor trust fund-national, World Bank, Khartoum: http://data.worldbank.org/country/sudan Accessed on 03 June 2016.

- Gaafar A. (2011). Forest plantations and woodlands in Sudan. African Forest Forum Working Paper Series, Volume (1) issue (15).

- GAC (2006). Gum arabic Company annual reports (An official statement compiling reports for the years 1970-2009. GAC Research Unit, Khartoum, Sudan.

- IFAD (2002). Evaluating cooperative societies of Gum arabic producers. Seminar Paper, records of Forests National Corporation, Um Ruwaba Locality, North Kordofan State, Sudan, pp7.

- Mahmoud, T. E., Maruod. E. M., Khiery, El Naim, M. A., Zaied. M B. (2014). Competitiveness of Gum arabic marketing system at El Obeid Crops Market, North Kordofan State, Sudan. World Journal of Agricultural Research 2 (5): 252–256.

- Mahmoud, T. E. (2004). The adequacy of price incentive on production, processing and marketing of Gum arabic in Sudan: A case study of North and West Kordofan, 1st edn. Schriftenreihe des Institutes für Internationale Forst- und Holzwirtschaft, Vol 11. Institut für Internationale Forst- und Holzwirtschaft, Tharandt8.

- MFE, Ministry of Finance and Economy (2007). "Marketing of Agricultural products in North Kordofan state, current situation and future prospects", North Kordofan State, Sudan.

- Nimir. A. M. M. (2000). Effects of Acacia senegal (L. Wild) on sandy soils and assessment of its foliage nutrient content: case Study of Damokeya Forest, Northern Kordofan State. A Master thesis submitted to University of Khartoum, Sudan.

- Sara, S, A., Rabah, A., Ali H. I. & Mahmoud, T. E. (2016). Acacia seyal gums in the Sudan: A review. The seventh graduate studies and scientific research conference, University of Khartoum, 20-23 February 2016. www.sgcac.u of k.edu

- Taha, M. E. (2006). The socioeconomic role of Acacia senegal in sustainable development of rural areas in the Gum arabic belt of the Sudan. Institute of International Forest and Forest Products, TU Dresden. Add print AG, Bannewitz/Germany, ISBN 3-9809816-4-9.

- Taha, M. E., Bekele T., Hammad Z. M.. (2014). Socio-economic conditions influencing the decision of communities to retain gum producing stands in the Gum arabic belt of the Sudan. International Journal of Agriculture, Forestry and Fisheries. Vol. 2, No. 1, 2014, pp. 1-7.

- Taha, M. E., Rizig, H. A., Elamin, H. M. A., Eltahir, M. E. S. and Bekele. T. (2015). Role of non-wood forest products in welfare of beneficiary stakeholders in Sheikan Locality, North Kordofan State, Sudan. International Journal of Agriculture, Forestry and Fisheries. Vol. 3, No. 4, 2015, pp. 129-136.